Go to Quantitative Methods

Topics

Table of Contents

Introduction and Estimation of the Simple Linear Regression Model

Financial analysts often need to find whether one variable X can be used to explain another variable Y. Linear regression allows us to examine this relationship.

Suppose an analyst is evaluating the return on assets (ROA) for an industry and wants to check if another variable – CAPEX can be used to explain the variation of ROA. The analyst defines CAPEX as: capital expenditures in the previous period, scaled by the prior period’s beginning property, plant, and equipment.

| Company | ROA | CAPEX |

| ------- | --- | ----- |

| A | 6 | 0.7 |

| B | 4 | 0.4 |

| C | 15 | 5 |

| D | 20 | 10 |

| E | 10 | 8 |

| F | 20 | 12.5 |

The variation of Y (Sum of Squares Total → SST) can be expressed as: Variation of Y =

- The variable whose variation we want to explain (dependent variable) is presented on the vertical axis denoted by Y.

- The explanatory variable (independent variable) is presented on the horizontal axis denoted by X.

A linear regression model computes the best fit line through the scatter plot, which is the line with the smallest distance between itself and each point on the scatter plot. The regression line may pass through some points, but not through all of them.

Regression analysis with only one independent variable is called simple linear regression (SLR).

Regression analysis with more than one independent variable is called multiple regression.

Estimating the Parameters of a Simple Linear Regression

Basics of Simple LR

Linear regression assumes a linear relationship between the dependent variable (Y) and independent variable (X).

The regression equation is expressed as follows:

- Y = Dependent variable

= Intercept = Slope - X = Independent variable

- ε = Error term

Estimating the Regression Line

Linear regression chooses the estimated values for intercept and slope such that the sum of the squared errors (SSE → Vertical distances between the observations and the regression line) is minimized.

The slope coefficient is calculated as:

or

The intercept coefficient is then calculated as:

For our example, the regression model will be

Interpreting the Regression Coefficients

- The intercept is the value of the dependent variable (Y) when the independent variable (X) is zero.

- The slope measures the change in the dependent variable (Y) for a one-unit change in the independent variable (X).

- If the slope is positive, the two variables move in the same direction.

- If the slope is negative, the two variables move in opposite directions.

In our example,

- If a company makes no capital expenditures, its expected ROA is 4.875%.

- If CAPEX increases by one unit, ROA increases by 1.25%.

Cross Sectional vs Time Series Regressions

Regression analysis can be used for two types of data:

- Cross sectional data: Many observations for different companies for the same time period.

- Time-series data: Many observations from different time periods for the same company.

Assumptions of the Simple Linear Regression Model

The 4 assumptions:

- Linearity: The relationship between the dependent variable, Y, and the independent variable, X, is linear.

- Homoskedasticity: The variance of the regression residuals is the same for all observations.

- Independence: The observations, pairs of Y's and X's, are independent of one another → Regression residuals are uncorrelated across observations.

- Normality: The regression residuals are normally distributed.

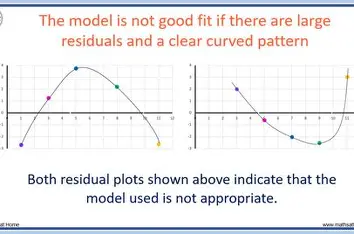

Assumption 1: Linearity

Since we are fitting a straight line through a scatter plot, we are implicitly assuming that the true underlying relationship between the two variables is linear.

- Simple Linear Regression model can't be used on Non Linear (

, Parabolic) relations. - Independent variable X should not be random.

- Residuals of the model should be random and not exhibit a pattern when plotted against X.

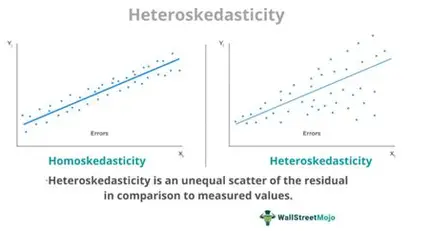

Assumption 2: Homoskedasticity

Homoskedasticity: Variance of the residuals is constant for all observations.

If not constant → Heteroskedasticity

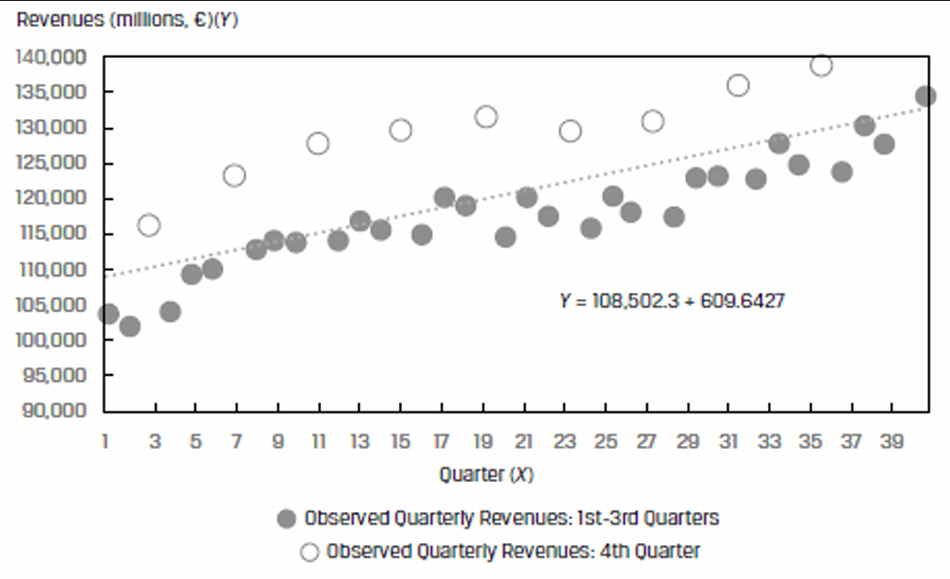

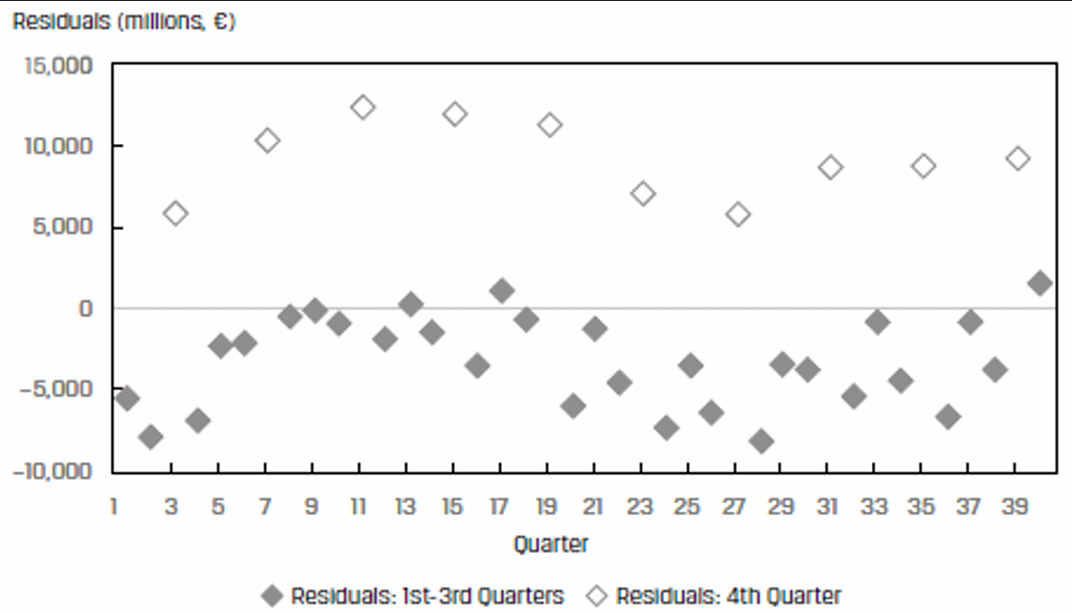

Assumption 3: Independence

Residuals should be uncorrelated across observations. If the residuals exhibit a pattern, then this assumption will be violated.

The residuals are correlated – they are high in Quarter 4 and then fall back in the other quarters.

Assumption 4: Normality

Residuals from the model should be normally distributed.

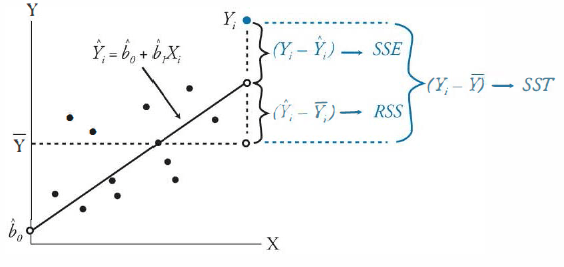

Analysis of Variance

Sum of Squares to Components

To evaluate how well a linear regression model explains the variation of Y we can break down the total variation in Y (SST) into two components:

- Sum of square errors (SSE)

- Regression sum of squares (RSS)

- SST measures the total variation in the dependent variable.

- RSS is amount of total variation in Y.

- SSE is the residual sum of squares that measures the unexplained variation in Y.

Measures of Goodness of Fit

Goodness of fit indicates how well the regression model fits the data. Several measures are used to evaluate the goodness of fit:

- Coeff of Determination

- F Test

Coefficient of Determination

The coefficient of determination, denoted by

Characteristics of coefficient of determination,

- The higher the

, the more useful the model. has a value between 0 and 1. - It tells us how much better the prediction is by using the regression equation rather than just average value to predict Y.

- With only one independent variable, it is the square of the correlation between X and Y.

- The correlation, r, is also called the “multiple-R”.

F Test

For a meaningful regression model, the slope coefficients should be non-zero.

This is determined through the F-test which is based on the F-statistic. The F-statistic tests whether all the slope coefficients in a linear regression are equal to 0.

In a regression with one independent variable, this is a test of the null hypothesis

The F-statistic also measures how well the regression equation explains the variation in the dependent variable.

- n - Total number of observations

- k - Total number of independent variables

- Regression sum of squares (RSS)

- Sum of squared errors or residuals (SSE)

Interpretation of F-test statistic:

- The higher the F-statistic, the better.

- A high F-statistic implies that the regression model does a good job of explaining the variation in the dependent variable.

- An F-statistic of 0 indicates that the independent variable does not explain variation in the dependent variable.

ANOVA and Standard Error of Estimate in Simple Linear Regression

Analysis of variance or ANOVA is a statistical procedure of dividing the total variability of a variable into components that can be attributed to different sources. We use it to determine the usefulness of the independent variables in explaining variation in the dependent variable.

ANOVA Table

| Source of Variation | Degrees of Freedom | Sum of Squares | Mean Sum of Squares | F Statistic |

|---|---|---|---|---|

| Regression | k | RSS | ||

| Error | n - 2 | SSE | ||

| Total Variation | n - 1 | SST | ||

| n represents the # of observations and k represents the # of independent variables. |

The standard error of estimate (SEE) measures how well a given linear regression model captures the relationship between the dependent and independent variables. It is the standard deviation of the prediction errors.

A low SEE implies an accurate forecast

Standard error of estimate (SEE) =

| Source | Sum of Squares | Degrees of Freedom | Mean Square |

|---|---|---|---|

| Regression | 576.1485 | 1 | 576.1485 |

| Error | 1873.5615 | 98 | 19.118 |

| Total | 2449.71 | ||

| F stat > 3.938, slope coefficient is statistically different from 0. | |||

| Model fits the data reasonably well. |

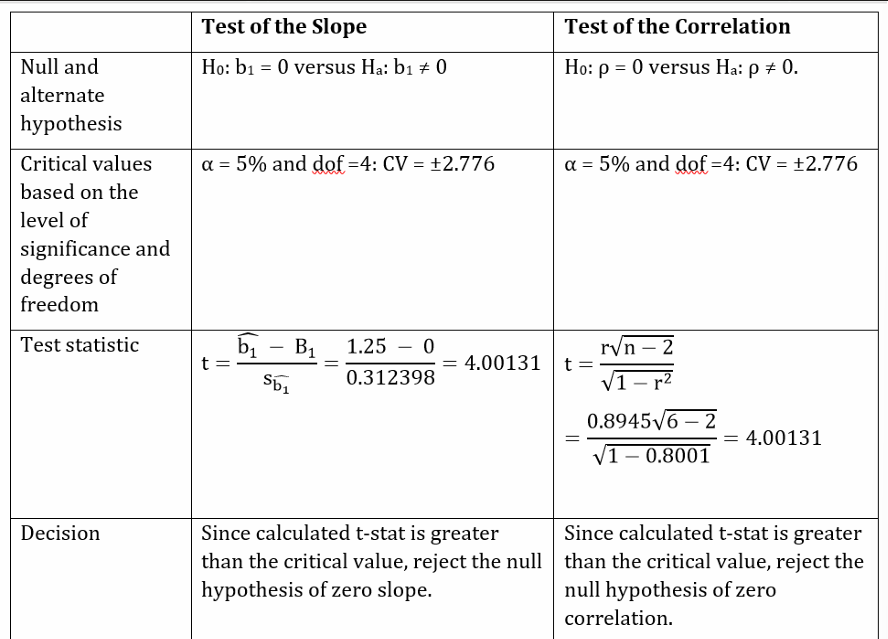

Hypothesis Testing of Individual Regression

Hypothesis Tests of the Slope Coefficient

In order to test whether an estimated slope coefficient is statistically significant, we use hypothesis testing.

- State the hypothesis.

- Identify the appropriate test statistic.

- Specify level of significance.

- State decision rule.

- Calculate test statistic.

- Make a decision.

t - statistic

is hypothesized population slope. is estimated slope coefficient. is the standard error of slope coefficient. - n - 2 = 4 degrees of freedom.

The standard error of the slope coefficient is calculated as:

1]

2] Find t statistic.

3]

4] 2 tailed test, 4 degrees of freedom, Critical t-values are ±2.776.

5] Calculate test statistic

6] Reject null hypothesis of a zero slope.

Test if slope coefficient is different from 1?

Fail to reject the null hypothesis.

Test if slope coefficient > 0?

- 1 Tailed with 5% level of significance and 4 degrees of freedom.

- Reject the null hypothesis.

Testing the Correlation

We can also use hypothesis testing to test the significance of the correlation between the two variables.

The regression software provided us an estimated correlation of 0.8945.

1]

2] Find t statistic.

3]

4] Critical t values are

5]

6] Reject the null hypothesis.

F stat is square of t stat for the slope or correlation.

Hypothesis Tests of the Intercept

For the ROA regression example, the intercept is 4.875%. Say you want to test if the intercept is statistically greater than 3%. This will be a one-tailed hypothesis test and the steps are:

1]

2] Find t stat.

3]

4] Critical t value for 6-2 degrees of freedom is 2.132.

5]

6] Reject the null hypothesis.

Hypothesis Tests of Slope When Independent Variable Is an Indicator Variable

An indicator (dummy) variable or a dummy variable can only take values of 0 or 1. An independent variable is set up as an indicator variable in specific cases.

Evaluate if a company’s quarterly earnings announcement influences its monthly stock returns.

Here, the monthly returns RET would be regressed on the indicator variable, EARN, that takes on a value of 0 if there is no earnings announcement that month.

The simple linear regression model can be expressed as:

You need not memorize this formula, but understand the factors that affect

The estimated variance depends on:

- Squared standard error of estimate,

- Number of observations, n

- Value of the independent variable, X

- Estimated mean

- Variance,

, of the independent variable

To determine the confidence interval around the prediction. The steps are:

- Make the prediction.

- Compute the variance of the prediction error.

- Determine

at the chosen significance level α. - Compute the (1-α) prediction interval using

.

In our ROA regression model, if a company’s CAPEX is 6%, its forecasted ROA is = 4.875 + 1.25 × 6 = 12.375%

Assuming a 5% significance level (α), two sided, with n − 2 degrees of freedom (so, df = 4), the critical values for the prediction interval are ±2.776.

The standard error of the forecast (

The 95% prediction interval is: 12.375 ± 2.776 (3.736912)

2.0013 <

Functional Forms for Simple Linear Regression

Economic and financial data often exhibit non-linear relationships. A plot of revenues of a company and time will often show exponential growth.

To make the simple linear regression model fit well, we will have to modify either the X or Y. The modification process is called transformation and the different types of transformations are:

- Log of Y

- Log of X

- Square of Y

- Differencing the Y

In the subsequent sections, we will discuss three commonly used functional forms based on log transformations:

- Log-lin model: X is logarithmic

- Lin-log model: Y is logarithmic

- Log-log model: Both are in logarithmic form.

The Log-Lin Model

Regression equation is expressed as:

The slope coefficient in this model is the relative change in Y for an absolute change in X.

Better for data with exponential growth.

The Lin-Log Model

Regression equation is expressed as:

The slope coefficient in this model is the absolute change in Y for a relative change in X.

Operating profit margin vs Unit sales

Better for data with logarithmic growth.

The Log-Log Model

Regression equation is expressed as:

The slope coefficient in this model is the relative change in Y for a relative change in X.

Used to calculate elasticities.

Company revenues vs Advertising spend as % of SG&A, ADVERT

Selecting the Correct Functional Form

To select the correct functional form, we can examine the goodness of fit measures:

- Coefficient of determination (

) - F-statistic

- Standard error of estimate (SEE)

A model with a high

In addition to these fitness measures, we can also look at the plots of residuals → Should not correlate.

| | Simple | Lin Log Model |

| --------- | ------- | ------------- |

| Intercept | 1.04 | 1.006 |

| Slope | 0.669 | 1.994 |

|

| SEE | 0.404 | 0.32 |

| F Stat | 141.558 | 247.04 |

Lin Log Model is better.