Yield-Based Bond Duration Measures and Properties

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- Measures of interest rate risk: Modified duration, money duration, and the price value of a basis point (PVBP)

- How a bond’s maturity, coupon, and yield levels affect its interest rate risk

Modified Duration

The duration of a bond measures the sensitivity of the bond’s full price (including accrued interest) to changes in interest rates. In other words, duration indicates the % change in the price of a bond for a 1% change in interest rates. The higher the duration, the more sensitive the bond is to change in interest rates.

There are two categories of duration: yield duration and curve duration.

- Yield duration measures a bond’s price sensitivity to changes in its own yield-to-maturity and assumes underlying cash flows are certain.

- Curve duration measures a bond’s price sensitivity to changes in a benchmark yield curve and accounts for the possibility that a bond may default.

- Macaulay duration is a weighted average of the time to receipt of the bond’s promised payments, where the weights are the shares of the full price that correspond to each of the bond’s promised future payments.

- Modified duration provides an estimate of the % price change for a bond given a change in its yield to maturity. It represents a simple adjustment to Macaulay duration $$\text{ Modified Duration} =\frac{\text{Macaulay Duration}}{1 + r} $$where r is the yield per period.

Therefore, percentage price change for a bond given a change in its YTM can be calculated as $$ % ΔPV^{ \text{FULL}} ≈ -\text{AnnModDur} \times Δ\text{Yield}$$

The

Calculating the modified duration of a bond

A 2-year, annual payment, $100 bond has a Macaulay duration of 1.87 years. The YTM is 5%. Calculate the modified duration of the bond.

Solution:

Modified duration, $$\frac{1.87}{1+0.05}=1.78$$

The percentage change in the price of the bond for a 1% increase in YTM will be $$-1.78 \times 0.01 \times 100 = -1.78%$$

Approximate Modified Duration

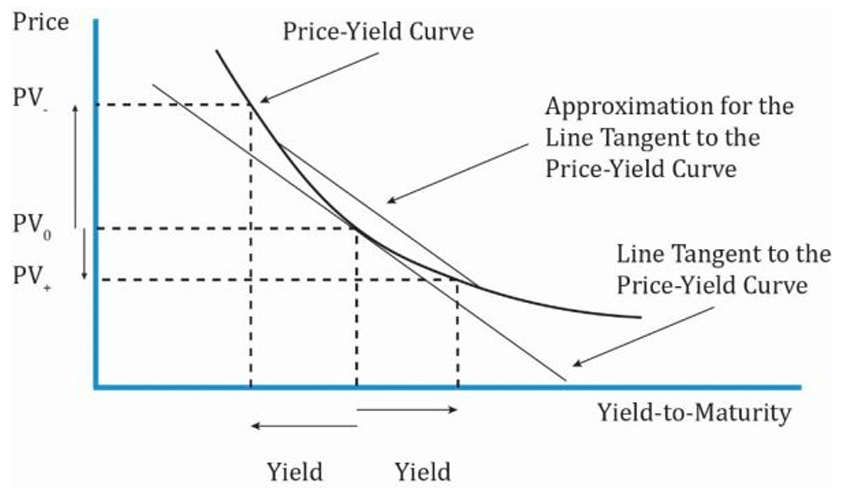

Modified duration is calculated if the Macaulay duration is known. But there is another way of calculating an approximate value of modified duration → Estimate the slope of the line tangent to the price-yield curve. This can be done by using the equation below: $$\text{Approximate Modified Duration}=\frac{(PV_ )– (PV_*)}{2 \times ∆\text{Yield} \times PV_0 }$$where:

- PV_ = Price of the bond when yield is decreased

= Initial price of the bond = Price of the bond when yield is increased

Interpretation of the Diagram

- Change in yield (up and down) is denoted by Δ yield.

- For slope calculation: vertical distance = PV_ –

and horizontal distance = 2 x ΔYield. - The yield to maturity is changed (increased/decreased) by the same amount.

- Calculate the bond price for a decrease in yield (PV_) and increase in yield (

). - Use these values to calculate the approximate modified duration.

Once the approximate modified duration is known, the approximate Macaulay duration can be calculated using the formula below: $$\text{Approximate Macaulay Duration }= \text{Approximate Modified Duration} \times (1 + r) $$

Calculating the approximate modified duration and approximate Macaulay duration

Assume that the 6% U.S. Treasury bond matures on 15 August 2017 is priced to yield 10% for settlement on 15 November 2014. Coupons are paid semiannually on 15 February and 15 August. The yield to maturity is stated on a street-convention semiannual bond basis. This settlement date is 92 days into a 184-day coupon period, using the actual/actual day-count convention. Compute the approximate modified duration and the approximate Macaulay duration for this Treasury bond assuming a 50bps change in the yield to maturity.

Solution: The yield to maturity per semiannual period is 5% (=10/2). The coupon payment per period is 3% (= 6/2). When the bond is purchased, there are 3 years (6 semiannual periods) to maturity. The fraction of the period that has passed is 0.5 (=92/184).

The full price (including accrued interest) at an YTM of 5% is 92.07 per 100 of par value.

Increase the yield to maturity from 10% to 10.5% – therefore, from 5% to 5.25% per semiannual period, and the price becomes 90.97 per 100 of par value.

Decrease the yield to maturity from 10% to 9.5% – therefore, from 5% to 4.75% per semiannual period, and the price becomes 93.19 per 100 of par value.

The approximate annualized modified duration for the Treasury bond is 2.41.

The approximate annualized Macaulay Duration is 2.53 (2.41 $times$ 1.05)

Therefore, from these statistics, the investor knows that the weighted average time to receipt of interest and principal payments is 2.53 years (the Macaulay Duration) and that the estimated loss in the bond’s market value is 2.41% (the Modified Duration) if the market discount rate were to suddenly go up by 1.0%

Money Duration and Price Value of a Basis Point

Money Duration

The money duration of a bond is a measure of the price change in units of the currency in which the bond is denominated, given a change in annual yield to maturity. $$\text{Money Duration} = \text{AnnModDur} \times PV_{FULL}$$$$ΔPV_{FULL} ≈ -\text{MoneyDur} \times Δ\text{Yield} $$Consider a bond with a par value of $100 million. The current yield to maturity (YTM) is 5% and the full price is $102 per $100 par value. The annual modified duration of this bond is 3. The money duration can be calculated as 3 x $102 million = $306 million.

- If the YTM rises by 1% (100 bps) from 5% to 6%, the decrease in value will be approximately $306 million x 1% = $3.06 million.

- If the YTM rises by 0.1% (10 bps), the decrease in value will be $306 million x 0.1% = $0.306 million.

Calculating money duration of a bond

A life insurance company holds a USD 1 million (par value) position in a bond that has a modified duration of 6.38. The full price of the bond is 102.32 per 100 of face value.

- Calculate the money duration for the bond.

- Using the money duration, estimate the loss for each 10 bps increase in the yield to maturity.

Solution:

-

Full price of the bond: $1,000,000 x 102.32% = $1,023,200.

The money duration for the bond is: 6.38 × $1,023,200 = $6,528,000. -

10 bps corresponds to 0.10% = 0.0010.

For each 10 bps increase in the yield to maturity, the loss is estimated to be: $6,528,000 × 0.0010 = $6,528.02.

Price Value of a Basis Point (PVBP)

An important measure which is related to money duration is the price value of a basis point (PVBP). The PVBP is an estimate of the change in the full price given a 1 bp change in the yield to maturity.

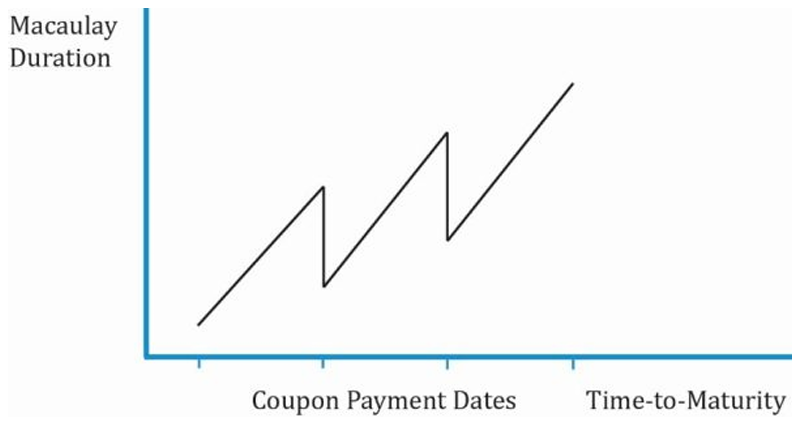

The fraction of the coupon period that has gone by (t/T)

First, let us consider the relationship between fraction of time that has gone by (t/T) and duration. Fraction of time (t/T) increases as time passes by. Assume T is 180. If 50 days have passed, then t/T = 0.277. If 90 days have passed, then t/T = 0.5. If 150 days have passed, then t/T = 0.83. As t/T increases from t = 0 to t = T with passing time, MacDuration decreases in value. Once the coupon is paid, t/T becomes zero and MacDuration jumps in value. When time to maturity is plotted against MacDuration, it creates a saw tooth pattern as shown graphically below:

Interpretation of the Macaulay duration between coupon payments with a constant yield to maturity

- Read from R to L. As time passes between coupon periods, duration decreases in value.

- Once the coupon is paid, it jumps back up creating a saw tooth pattern.

Time to maturity

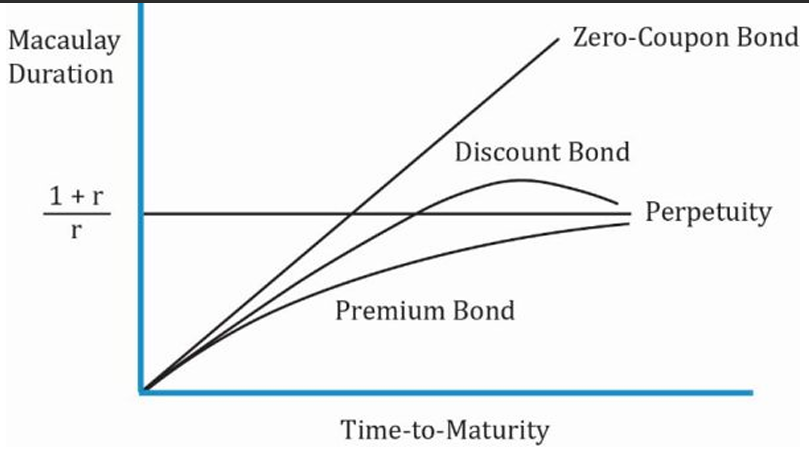

The following exhibit illustrates the relationship between Macaulay duration and the time to maturity for premium, discount, zero-coupon and perpetual bonds.

- Zero-coupon bond: Pays no coupon so c = 0. Plugging in c = 0 and t/T = 0 in MacDur formula, we get Macaulay Duration = N. For a zero-coupon bond, duration is its time to maturity.

- Perpetuity: A perpetual bond is one that does not mature. There is no principal to redeem. It makes a fixed coupon payment forever. If N is a large number in the above equation, then the second part of the expression in the braces becomes zero.

- Denominator: N is an exponent. (1 + r) is a very large number. So 1/(1 + r) must be zero and the value in the numerator will not matter here.

- Macaulay duration of a perpetual bond is (1 + r)/r as N →

.

- Premium bond: Bonds are trading at a premium above par or at par. The coupon rate is greater than or equal to yield to maturity (r).

- The numerator of the second expression in braces is always positive because c-r is positive.

- The denominator of the second expression in braces is always positive. Second expression as a whole is always positive.

- MacDuration = Less than (1 + r)/r because the second expression in braces is positive. As time passes, it approaches (1 + r)/r.

- Discount bond: For a discount bond, the coupon rate is below yield to maturity. The Macaulay Duration increases for a longer time to maturity.

- The numerator of the second expression in braces is negative because c-r is negative. Put together, the duration at some point exceeds (1 + r)/r , reaches a maximum, and approaches (1 + r)/r (the threshold) from above. This happens when N is large and coupon rate (c) is below the yield to maturity (r).

- As a result, for a long-term discount bond, interest rate risk can be lesser than a shorter-term bond.

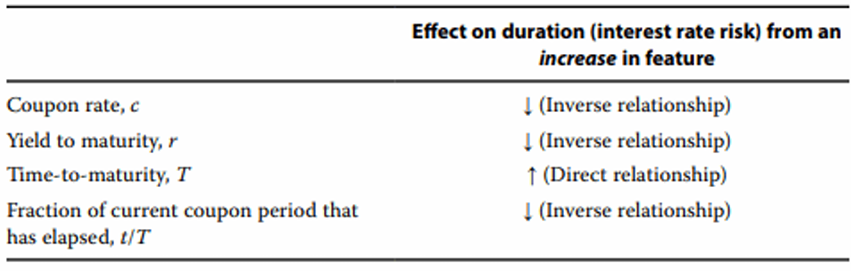

Coupon rate and Yield-to-maturity

All else being equal, a lower-coupon bond has a higher duration and more interest rate risk than a higher-coupon bond.

The same pattern holds for yield-to-maturity, a bond with a lower YTM has a higher duration and more interest rate risk than a bond with a higher YTM.

This is because lower coupons and lower yields increase the weight of the maturity value or final cash flow and reduce the weight of the nearer-term cash flows in the calculation for Macaulay duration.