Yield and Yield Spread Measures for Fixed-Rate Bonds

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- How to calculate the annual yield on a bond for varying compounding periods in a year

- Yield and yield spread measures for fixed-rate bonds

Periodicity and Annualized Yields

Periodicity is the number of compounding periods in a year, or number of coupon payments made in a year.

The stated annual rate for a bond will depend on the periodicity we are assuming. The stated annual rate is also called the annual percentage rate or APR.

A quarterly coupon paying bond has a periodicity of four, while a semi-annual bond has a periodicity of two, and a monthly-pay bond with a given annual yield would have a periodicity of twelve.

Compounding more frequently within the year results in a lower (more negative) yield-to-maturity.

Consider a 5-year, zero-coupon bond priced at 80 per 100 par value. What is the stated annual rate for periodicity = 4, periodicity = 2, and periodicity = 1?

4.487% 4.51% 4.56%

The formula for conversion based on periodicity is $$\left(1+\frac{APR_m }{m}\right)^m =\left(1+\frac{APR_m }{n}\right)^n $$

A 4-year, 3.75% semi-annual coupon payment government bond is priced at 97.5. Calculate the annual yield to maturity stated on a semi-annual bond basis and convert the annual yield to:

- An annual rate comparable to bonds that make quarterly coupon payments.

- An annual rate comparable to bonds that make annual coupon payments.

Solution

- The annual rate of 4.439% for compounding semiannually compares with 4.415% for compounding quarterly.

- The annual percentage rate of 4.439% for compounding semiannually compares with an effective annual rate of 4.488%.

The effective annual rate (EAR) is the yield on an investment in one year taking into account the effects of compounding. This rate has a periodicity of one as there is only one compounding period per year. EAR is used to compare the rate of return on investments with different frequency of compounding (periodicities).

Semi annual bond equivalent yield: Yield per semi-annual period times two. If the yield per semi-annual period is 2%, then the semi-annual bond equivalent yield is 4%.

Other Yield Measures, Conventions, and Accounting for Embedded Options

Other Yield Measures and Conventions

- Street convention: It is the yield to maturity using a 30/360-day convention assuming payments are made on scheduled dates, even if the payment date fell on a weekend or a holiday.

- True yield: Yield to maturity calculated using an actual calendar of weekends and holidays. True yield assumes the payment is made on 16 March if it is a business day. The coupon payment is discounted back from 16 March instead of 15 March.

- Government equivalent yield: Yield to maturity calculated using the actual day/count convention used for U.S. Treasuries.

- Current yield (Simple yield): Sum of the coupon payments received over the year divided by the flat price. It is also called the income or interest yield. Current yield is not an accurate measure of the rate of return as it ignores the frequency of coupon payments, reinvestment income, and capital gain/loss on a bond. $$\text{Current Yield} =\frac{\text{Annual Cash Coupon Payment}}{\text{Bond Price}}$$

Bonds with Embedded Options

For bonds with embedded options the following yield measures are used.

- Yield-to-call: Calculates the rate of return on a callable bond if it is bought at market price and held until the call date.

The difference between YTM and the yield-to-call is that YTM assumes the bond is held to maturity. Calculation of yield-to-call is the same as YTM where N = number of periods to call date and FV = call price.

- Yield-to-first call (YTFC): It is the internal rate of return if the bond was bought at market price and held until the first call date.

- Yield-to-second call: Similarly, the yield on a callable bond if it was bought at market price and held to the second call date is called yield-to-second call.

- Yield-to-worst: Yield is calculated for every scenario. The lowest yield is called the yield-to-worst.

- Option adjusted yield: The option-adjusted yield is the required market discount rate whereby the price is adjusted for the value of the embedded option. For example, investors pay a lower price for the callable bond than if it were option-free. If the bond were non-callable, its price would be higher. The option-adjusted price is used to calculate the option-adjusted yield.

| | A | B |

| ----------------------- | ------------- | --------- |

| Annual Coupon Rate | 6 % | 10 % |

| Coupon Payment Freq | Semi Annually | Quarterly |

| Years to Maturity | 4 years | 4 years |

| Price (Per 100 Par Val) | 95 | 110 |

| Current Yield | 6.32 % | 9.10 % |

| Yield to Maturity | 7.47 % | 7.11 % |

The additional compensation for the greater risk in Bond A is 30 bps (0.07469 – 0.07169).

- The yield-to-first call = 10.325%

- The yield-to-second call = 10.09%

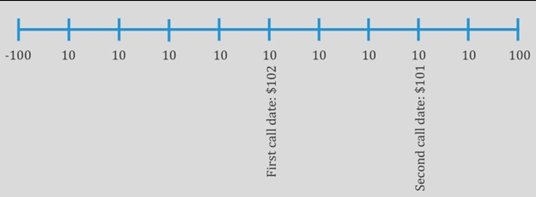

A bond with 4 years remaining until maturity is currently trading for 101.75 per 100 of par value. The bond offers a 5% coupon rate with interest paid semiannually. The bond is first callable in 2 years and is callable after that date on coupon dates according to the following schedule:

- 2 → 102.50

- 3 → 101.50

- 4 → 100.00

- What is the bond’s annual yield-to-first-call?

- What is the bond’s yield-to-worst?

Solution

To arrive at the annualized yield-to-first-call, the semiannual rate must be multiplied by two. (2.6342 × 2 = 5.2684)

The yield-to-worst is 4.52%. The bond’s yield to worst is the lowest of the sequence of yields-to-call and the yield to maturity.

- Yield-to-first-call = 5.27%

- Yield-to-second-call = 4.84%

- Yield to maturity = 4.52%

Yield Spread Measures for Fixed-Rate Bonds and Matrix Pricing

Yield Spreads over Benchmark Rates

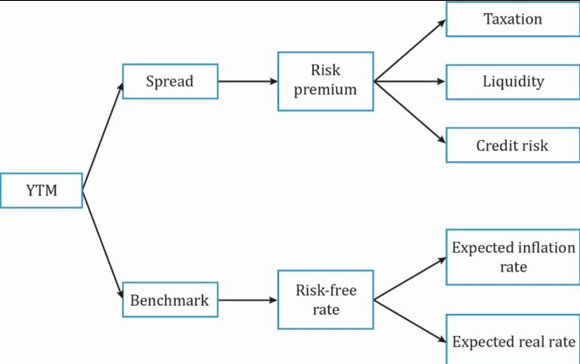

The yield spread is the difference in yield between a fixed-income security and a benchmark.

Say the YTM of a 3-year corporate bond is 7.00%. The benchmark rate is 3-year Libor, which is 5.00%. The yield spread of the corporate bond relative to the benchmark is 2.00%.

Generally, the benchmark reflects macroeconomic factors. A spread reflects microeconomic factors and aspects specific to the issuer, such as credit quality of the issuer and bond, tax status, etc.

The YTM of a bond can be broken down into the following components:

Spreads enable an analyst to more accurately assess a bond’s historical and comparative value by controlling for (excluding) macroeconomic factors such as a broad increase or decrease in benchmark rates. An analyst might compare the current spread to its historical average, highs and lows, and other bonds to determine whether a bond is under- or overpriced relative to others.

Two related concepts are the G-spread and the I-spread.

- The

G-spreadis the yield spread in basis points over an interpolated government bond. The spread is higher for bearing higher credit, liquidity, and other risks relative to the government bond. - The

I-spreadis the yield spread of a specific bond over the standard swap rate in that currency of the same tenor.

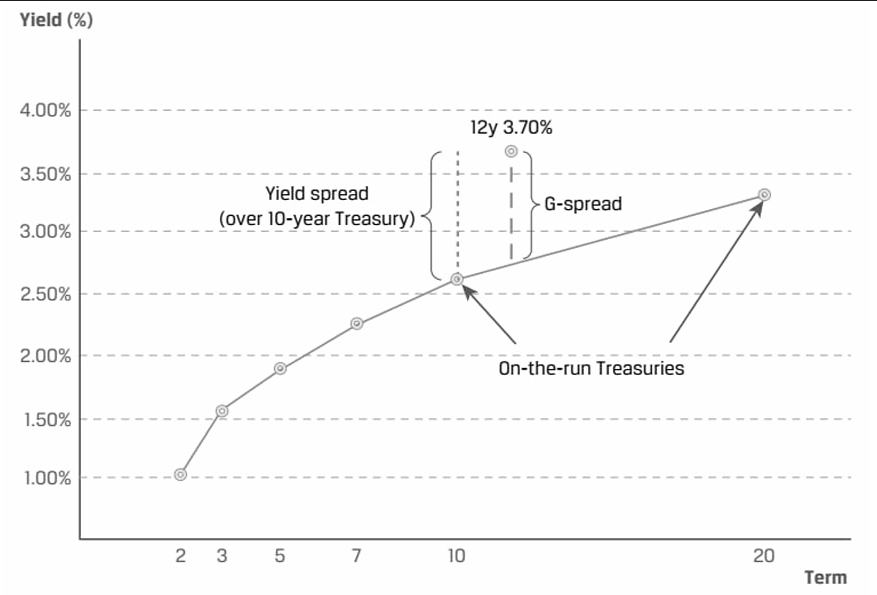

Calculating G-Spread using Matrix Pricing

The G-spread measures the spread over interpolated government bonds. It uses constant maturity Treasury yields to maturity as the benchmark.

Say we want to calculate the G-spread of a 12-year bond. In the market on the run government bonds are available with 7 years, 10 years and 20 years maturities. Since we do not have a government bond with exactly 12 years maturity, we will use linear interpolation on the 10-year and 20-year government bonds.

A 5% annual coupon corporate bond with 3 years remaining to maturity is trading at 100.175. The 3-year, 3% annual payment government benchmark bond is trading at 100.50. The 1-year and 2-year government spot rates are 2.05% and 3.425% respectively. Calculate the G-spread, the spread between the yields to maturity on the corporate bond and the government bond having the same maturity.

Solution:

The yield to maturity for the corporate bond is 4.936%.

The yield to maturity of the government bond is 2.824%.

The G-spread is 4.936% – 2.824% = 2.11% or 211 bps.

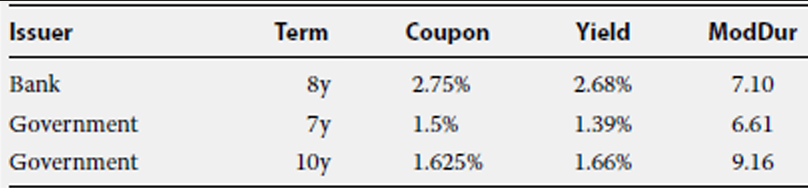

A portfolio manager considers the following annual coupon bonds:

Calculate the G-spread for the bank bond.

Solution: The G-spread is the difference between the bank bond YTM and a linear interpolation of the YTMs of the 7-year government bond and the 10-year government bond.

The interpolated 8-year government rate is: 1.39% +

G-spread = 2.68% – 1.48% = 1.20%

Yield Spreads over the Benchmark Yield Curve

The Z-spread (zero-volatility spread) is based on the entire benchmark spot curve. It is the constant spread that is added to each spot rate such that the present value of the cash flows matches the price of the bond. The Z-spread is also called the static spread as it is constant for all periods.

The option-adjusted spread (OAS) is the Z-spread adjusted for the value of an embedded option.

- Callable bond with a Z-spread of 90 basis points, of which 10 basis points are due to the embedded call option. In this case, the OAS is 90 – 10 = 80 basis points.

- Putable bond with a Z-spread of 90 basis points and the value of the put option is 10 basis points, the OAS is 90 + 10 = 100 basis points.

Based on these simple scenarios, it should be clear that for a callable bond, the OAS is lower than the Z-spread, and for a putable bond, the OAS is higher than the Z-spread.