Mortgage-Backed Security (MBS) Instrument and Market Features

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module focuses on the largest ABS market in the world – the mortgage-backed securities (MBS) market. In this module we will cover:

- Prepayment risk and time tranching structures

- Fundamental features of residential mortgage loans that are securitized

- Types and characteristics of residential mortgage-backed securities

- Commercial mortgage-backed securities

Time Tranching

Prepayment Risk

The cash flow of a mortgage consists of the following three components:

- Interest

- Scheduled principal payments

- Prepayments (any principal repaid in excess of the scheduled principal)

The risk associated with uncertainty in future cash flows of MBS securities because of unscheduled principal repayments of the underlying mortgages is called prepayment risk. It has two components: contraction risk and extension risk.

- Contraction risk is the risk that when interest rates decline, the security will have a shorter maturity than was anticipated at the time of purchase because homeowners refinance at now-available lower interest rates.

Assume the interest rate is 8% when the Smiths take the loan. If two years later it falls to 6%, then they will prepay the loan and refinance at the lower rate.

- Extension risk is the risk that when interest rates rise, fewer prepayments will occur because homeowners are reluctant to give up the benefits of a contractual interest rate that now looks low. From an investor’s perspective, the security becomes longer in maturity than it was at the time of purchase.

Time tranching is a securitization structure that allows the redistribution of prepayment risk among bond classes. For example, in a sequential tranching structure, the principal repayments flow first to one tranche until its principal is fully repaid, then principal repayments flow to the next tranche and so on.

Mortgage Loans and their Characteristic Features

A mortgage loan is a loan secured by the collateral of some specified real estate property which obliges the borrower to make a predetermined series of payments to the lender.

In simple words, it is a loan a buyer takes for buying a real estate property (land, apartment, house, etc.); the collateral is the property being bought.

If the buyer defaults on mortgage payments, then it gives the lender the right to foreclose on the loan, take possession of the property, and sell it to recover funds given as debt.

The amount lent as loan towards the purchase of the property is always less than the purchase price. It is equal to the purchase price minus the down payment made by the buyer. The buyer’s initial equity is equal to the down payment made.

The ratio of the mortgage loan amount to the property’s purchase price is called the loan-to-value (LTV) ratio. From a lender’s perspective, lower the LTV, the less likely the borrower is to default. Also, if the borrower does default, the lender will have better chances of recovering the amount loaned by repossessing and selling the property.

Another consideration is the capacity to sustain debt payments measured by the debt-to-income ratio (DTI). This ratio compares an individual’s monthly debt payments to their monthly pre-tax, gross income. From the lender’s perspective, lower the DTI, the less likely the borrower is to default.

In the United States, based on the credit quality of the borrower, mortgages can be classified as:

- Prime loans – Borrower has high credit quality, strong credit history, sufficient income to service the loan, and substantial equity in the underlying property.

- Subprime loans – Borrower has low credit quality, high DTI, and/or high LTV.

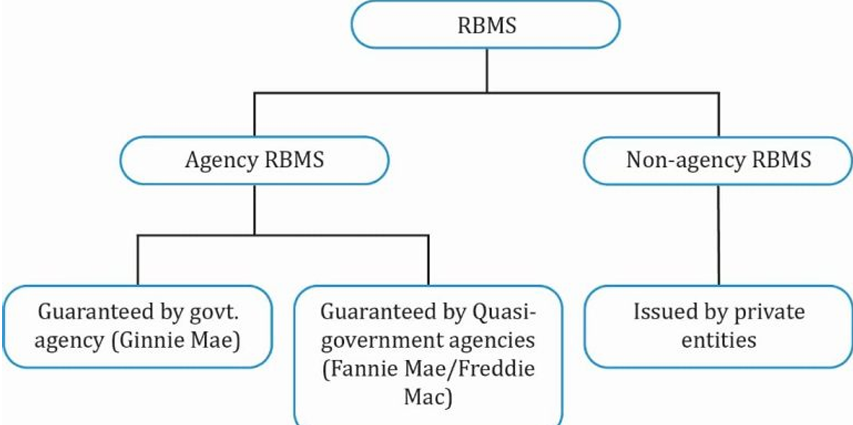

Agency and Non-Agency RMBS

Residential mortgage-backed securities are bonds created from the securitization of residential mortgage loans. In the U.S., residential mortgage-backed securities are divided into the following three sectors:

- Those guaranteed by a federal agency (Ginnie Mae) whose securities are backed by the full faith and credit of the U.S. government.

- Those guaranteed by either of the two government-sponsored enterprises or GSEs (Fannie Mae and Freddie Mac) but not by the U.S. government. They do not carry the full faith and credit of the U.S. government.

- Those issued by private entities that are not guaranteed by a federal agency or a GSE.

Examples of agency RMBS include:

- Mortgage pass-through securities

- Collateralized mortgage obligations

The two differences between agency RMBS issued by GSEs and non-agency RMBS are as follows:

- Non-agency RMBS use credit enhancements to reduce credit risk, while agency RMBS issued by the GSEs are guaranteed by the GSEs themselves.

- For a loan to be included in a pool of loans backed by an agency RMBS, it must satisfy the underwriting standards of the government agencies.

Mortgage Contingency Features

Mortgages may contain certain features that give the borrower and the lender certain rights throughout the contract.

Prepayment option: A prepayment option or an ‘early repayment option’ entitles the borrower to prepay all or part of the outstanding mortgage principal prior to maturity. In some countries, there may be a penalty for prepayment as it hurts the lender (recall prepayment risk). The objective of imposing a penalty is to compensate the lender for the difference in the contract rate and the prevailing mortgage rate when the borrower prepays as rates decline.

Recourse and non-recourse mortgage loans: If the borrower of a loan defaults on payments, then the lender can seize the property and sell it. The proceeds from the sale may be less than the outstanding mortgage balance, and not enough to recoup the losses.

There are two types of mortgage loans in such cases:

- Recourse loans: The lender can claim the shortfall (outstanding mortgage balance – after the property is sold) from the borrower. For instance, if the borrower has other properties or possessions such as an expensive car, or valuable art, then these could be sold to fulfill the shortfall.

- Non-recourse loans: Most mortgage loans are non-recourse. The lender may sell the property in case of a default and keep the proceeds. But, unlike a recourse loan, the bank/lender cannot claim other assets of the borrower to fulfill the shortfall in the outstanding mortgage balance.

Residential Mortgage-Backed Securities (RMBS)

Mortgage Pass-Through Securities

A mortgage pass-through security is created when one or more holders of mortgages form a pool of mortgages and sell shares or participation certificates in the pool. The investors receive a share of cash flows from the underlying pool of mortgage loans.

Cash Flow Characteristics

- Monthly mortgage payments consist of interest, scheduled principal repayment, prepayments.

- Payments are made to security holders each month.

- The servicer collects monthly payments, sends payment notices to borrowers, sends reminders if payments are overdue, maintains records of principal balances, etc.

- The servicing fee is part of the mortgage rate.

- The amount of cash flow from mortgage loans is not equal to that received by the investors. Similarly, there is a delay in passing the cash flow from mortgage loans to the security holders.

Monthly cash flow of a mortgage pass-through security = Monthly cash flow of the underlying pool of mortgages – Servicing and other fees.

- In other words, investors of the mortgage pass-through security receive less than the cash flow coming in from the mortgage loans because a servicing fee is collected by the servicer.

How is the rate and maturity of a mortgage loan calculated?

- Pass-through rate: A mortgage pass-through security’s coupon rate is called the pass-through rate. For example, if the mortgage rate for a pool of mortgages is 8%, the annualized servicing fee is 0.6%, then the investors receive an average return of around 7.4%.

- Weighted average coupon (WAC): Each of the mortgage loans in the securitized pool may not have the same mortgage rate. The WAC is found by weighting the rate of each mortgage loan in the pool by the percentage of the mortgage outstanding relative to the outstanding amount of all mortgages in the pool.

- Weighted average maturity (WAM): Similarly, not all the loans in the pool will have the same maturity. WAM is found by weighting the remaining number of months to maturity for each mortgage loan in the pool by the amount of the outstanding mortgage balance.

| Mortgage | Outstanding Bal | Coupon Rate | Time to Maturity |

| -------- | --------------- | ----------- | ---------------- |

| 1 | 1k | 4.5 % | 28 months |

| 2 | 2k | 4.75 % | 42 months |

| 3 | 4k | 5.15 % | 37 months |

| 4 | 3k | 3.8 % | 60 months |

- WAC = 4.6 %

- WAM = 44 months

Collateralized Mortgage Obligations (CMOs)

The prepayment risk seen in mortgage pass-through securities can be reduced by distributing the cash flows of these mortgage products to different classes or tranches through a process called structuring.

Collateralized mortgage obligation (CMO) is one such security created based on this principle of structuring where the cash flows (interest and principal) are redistributed to different tranches based on a set of rules.

The different classes of bondholders in a CMO have different exposures to prepayment risk. The collateral for a CMO is a pool of mortgage pass-through securities and not a pool of mortgage loans.

Advantages

- CMOs can be created to closely satisfy the asset/liability needs of institutional investors, thereby broadening the appeal of mortgage-backed products.

- Some investors may want to increase their exposure to prepayment risk, while some may want to reduce. Based on their individual needs and risk appetite, investors can choose the CMO.

The most common types of CMO tranches are sequential-pay tranches.

Sequential-Pay CMO

Each class/tranche of bond in this CMO structure is retired sequentially. Let us consider a CMO with four tranches. Note that this example is for simplicity. The coupon rate usually varies by tranche.

| Tranche | Par Amount | Coupon Rate |

|---|---|---|

| A | 389 M | 5.5 |

| B | 72 M | 5.5 |

| C | 193 M | 5.5 |

| D | 146 M | 5.5 |

| The prepayment risk is mitigated in this CMO by following these interest and principal repayment rules: |

- For payment of monthly coupon interest: Disburse monthly coupon interest to each tranche on the basis of the amount of principal outstanding for each tranche at the beginning of the month.

- For disbursement of principal payments:

- Disburse principal payments to tranche A until it is completely paid off and sequentially upto tranche D.

- In this structure:

- Tranche A has the highest contraction risk while tranche D has the highest extension risk.

- Tranches A and B provide protection against contraction risk for tranches C and D.

- Similarly, tranches C and D provide protection against extension risk for tranches A and B respectively.

Other CMO Structures

- Z-tranches: They do not pay interest payments until a pre-set date, when both principal and accrued interest payments start.

- Principal-only (PO) securities: They pay only the principal repayments from the pool.

- Interest-only (IO) securities: They pay only the interest payments from the pool.

- Floating-rate tranche: Although the collateral pays a fixed rate, we can create tranches that pay floating rates. To do this a floater and an inverse floater combination is constructed from any of the fixed-rate tranches in the CMO structure. These tranches are sold to separate sets of investors with opposing views on interest rate movements.

- If interest rates go up, the floating rate tranche will pay a higher rate but the inverse floater tranche will pay a lower rate. Thus, the two tranches offset each other and the effective rate paid will be equal to rate on original fixed rate tranche.

- Planned Amortization Class (PAC) tranche: PAC tranches are often accompanied by support tranches. PAC tranches make scheduled and fixed principal payments over a predetermined time period to their investors if the prepayment levels in the pool are within a certain maximum and minimum range. If the prepayment rate is within the specified range, all prepayment risk is absorbed by the support tranche. Thus, PAC tranches offer the greatest predictability and stability of the cash flows.

Commercial Mortgage-Backed Securities (CMBS)

Commercial mortgage-backed securities (CMBS) are backed by a pool of commercial mortgage loans on income-producing property.

Important features of a CMBS are as follows:

- The underlying are loans to purchase or refinance a commercial property such as a warehouse, apartment building, office building, hotels, health care facilities, etc.

- Commercial mortgage loans are non-recourse loans. Lenders can only stake a claim to the income-producing property backing the loan in case of a default and not on any other asset of the borrower. Therefore, analysis of CMBS securities focus on the credit risk of the property and not on the credit risk of the borrower.

- It is important to study the cash flows from the underlying properties for credit analysis.

- There are two key indicators to assess the potential credit performance of a commercial mortgage loan:

- Debt-to-service coverage ratio

- Loan-to-value ratio

- Debt Service = Annual interest payment and principal repayment

- Net Operating Income = Rental income – Cash operating expenses – Non-cash replacement reserve

If DSC > 1.0, then cash flows from property are sufficient to service debt.

How to interpret DSC and LTV ratios:

- The higher the DSC ratio, the lower the credit risk and the better is the borrower’s ability to service debt.

- A low loan-to-value ratio implies lower credit risk.

- To memorize this formula, draw a parallel with interest coverage ratio from FSA.

CMBS Structure

Interest and principal repayments in a CMBS are structured as follows:

- Interest on principal outstanding is paid to all tranches.

- The highest-rated bonds are paid off first in the CMBS structure.

- Losses arising from loan defaults are charged against the principal balance of the lowest priority CMBS tranche outstanding. These tranches may be unrated by credit-rating agencies and are called the

first-loss piece,residual tranche, orequity tranche.

Characteristics

Call Protection

RMBS investors are exposed to prepayment risk since the borrowers have a right to prepay and are not penalized for prepayment; they have an incentive to prepay. CMBS has considerable call protection, which is protection against early prepayment of mortgage principal. The call protection comes in two forms: at the structure level and at the loan level.

Structural level:

Structuring CMBS into sequential-pay tranches, by credit rating. A lower-rated tranche cannot be paid off until the higher-rated tranches are retired. But, in the case of a default, the losses must be charged to the lowest-rated tranche first and last to the highest-rated tranche.

Loan level:

- Prepayment lockouts: The borrower is prohibited from any prepayments during a specific period of time.

- Prepayment penalty points: The borrower must pay a fixed percentage of the outstanding loan balance as prepayment penalty if he wishes to refinance.

- Yield maintenance charges: Also known as

make-whole charge. The borrower must pay a penalty to the lender that makes refinancing uneconomical if the sole objective was to get a lower mortgage rate. - Defeasance: Defeasance is a protection at the loan level that requires the borrower to provide sufficient funds that can be invested in a portfolio of government securities to replicate the cash flows in the absence of prepayments.

CMBS Risks

Commercial mortgage-backed securities (CMBS) can consist of only a few underlying commercial mortgages, so a single default in a CMBS pool can have a significant impact on CMBS investors. Investors must evaluate this unique concentration risk by analyzing the individual loans and properties backing the CMBS.

Balloon Risk

Residential mortgages are fully-amortizing loans that are fully amortized over a long period of time. Usually, there is no principal outstanding after the last mortgage payment. But many commercial loans backing CMBS transactions are balloon loans which require a substantial principal payment on the final maturity date. If the borrower is not able to make the lump sum payment, he may ask for an extension of the loan over a period of time called the “workout period”.

Balloon risk is a type of extension risk. The risk that a borrower will not be able to make the balloon payment either because the borrower cannot arrange for refinancing or cannot sell the property to generate sufficient funds to pay off the balloon balance is called “balloon risk”.