Markets for Government Issuers

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- Fixed income securities issued by sovereign and non-sovereign governments, quasi-government entities, and supranational agencies

- Differences between the issuance of government versus corporate fixed-income instruments

Sovereign Debt

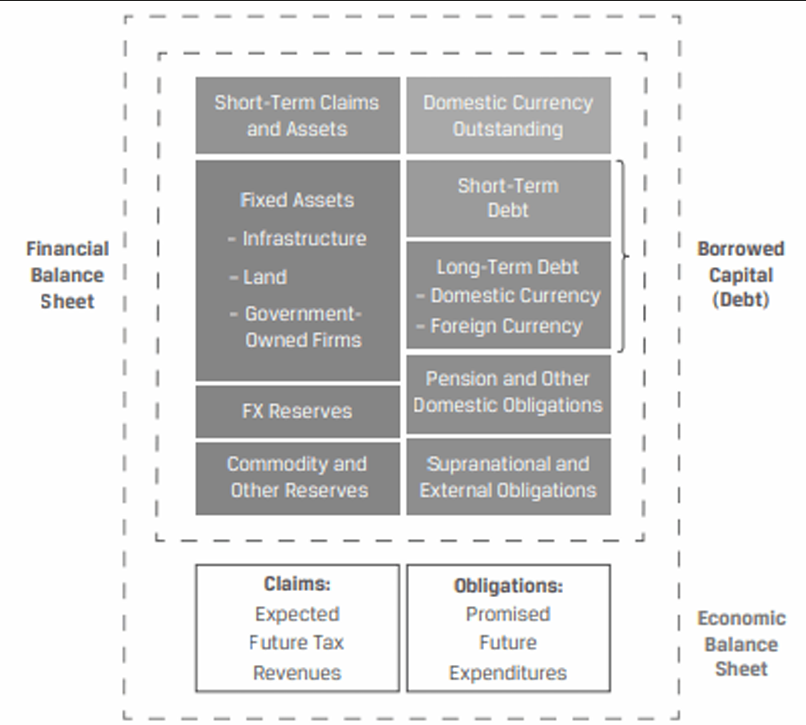

Sovereign debt is issued by national governments primarily for fiscal reasons. Taxes are the primary source of revenue for a government. If tax revenue is insufficient, then a government raises money by issuing sovereign debt. Sovereign debt is not backed by collateral. The primary source of repayment is tax collections.

Additional sources include tariffs, usage fees, and cash flows from government owned enterprises.

While corporate financial statements are accrual based, financial accounting for governments is often cash based. Items such as depreciation of fixed public goods (e.g., national highways), or accrual of unfunded liabilities (e.g., government pension obligations) are typically excluded from the balance sheet.

However, expected future claims and obligations are included because they are of greater relevance for public issuers as compared to corporates.

Developed market versus Emerging market Sovereign Issuers

An important distinction among sovereign debt is the difference between developed market (DM) and emerging market (EM) sovereign issuers.

- DMs are characterized by a strong, stable, well-diversified domestic economy. They typically have a stable and transparent fiscal policy. For these reasons, the debt issued by DM sovereign issuers is often referred to as default-risk free.

- EMs are usually characterized by higher growth but less stable and less well-diversified economies that may be subject to greater fluctuations over the economic cycle. Rating agencies distinguish between a DM sovereign bond issued in local currency and one in foreign currency.

- Local currency bonds generally have a higher credit rating than foreign currency bonds, because if needed the national government can print local currency to repay the bond, however it cannot print the foreign currency.

Investors based in developed markets who purchase external debt of emerging and frontier market sovereign issuers face indirect exposure to currency fluctuations, because their returns depend on an issuer’s ability to generate foreign currency revenue to meet foreign currency interest and principal payments through international capital, goods, and services flows.

Government debt management policies

Government debt management policies determine the composition of sovereign debt, i.e. short-term versus long-term, as well as other features.

Sovereign debt issues include the following:

- Short-term securities (often known as Treasury bills) with maturities ranging from 1 to 12 months. They are usually issued as zero-coupon instruments and are sold at a discount to par.

- Medium and long-term securities (often known as Treasury notes and Treasury bonds). They are often issued as fixed-rate domestic currency instruments. But sovereigns may also issue floating rate, inflation linked, and foreign currency instruments.

- Sometimes sovereign governments do not directly issue securities but instead provide a guarantee that effectively makes the securities a type of sovereign debt. For example, Mortgage-backed securities in US.

Ricardian equivalence

According to the Ricardian equivalence,

Government’s choice of debt maturity is irrelevant in determining the present value of future tax cash flows.

Taxpayers expect government debt to be offset by higher future taxes, implying that a sovereign government should be indifferent between collecting taxes today or raising debt of any maturity based on the following assumptions:

- Taxpayers smooth consumption over time, saving expected future taxes today for future payment.

- Taxpayers form rational expectations that today’s tax cuts will result in future tax increases.

- Capital markets are perfect with no transaction costs, and taxpayers can freely borrow and lend.

- Taxpayers are altruistic on an intergenerational basis; that is, they pass on tax savings to descendants.

Based on this theory, governments should fund themselves with the shortest maturity to minimize borrowing costs (long term bonds have higher interest rates due to term premiums). However, this strategy will introduce significant rollover risk. Also, the assumptions rarely hold perfectly. Therefore, in practice, governments seek to minimize interest rate and rollover risks by distributing debt across maturities, while issuing debt in regular, predictable intervals.

Benefits of longer-term sovereign government securities

Long-term sovereign debt has higher borrowing costs, however, it provides the following benefits:

- Establishment of a risk-free benchmark for all debt of specific maturities: Sovereign bond yields are often used as a benchmark to calculate a corporate issuer’s credit risk premium. Therefore, government debt policies frequently require the regular issuance of benchmark securities with varying maturities in order to improve capital market efficiency and transparency for private issuers.

- Use in managing and hedging market interest rate risk: These instruments and related derivatives are often used by financial intermediaries and asset managers to manage interest rate risk separately from credit risk.

- Preferred use as collateral in repo and derivative transactions: These instruments are the most common form of collateral for both repo and derivative transactions due to their high degree of liquidity and safety.

- Government bond use in monetary policy and foreign exchange reserves: Central banks buy and sell these instruments (open market operations) to implement their monetary policy mandate. Foreign market participants often hold their foreign currency reserves in the form of liquid foreign government bonds.

Sovereign Debt Issuance and Trading

While corporate debt issuances are managed by investment banks, sovereign debt is typically issued through a public auction using standard procedures led by the national treasury or finance ministry.

Once a government debt auction is announced, prospective investors submit a competitive or non-competitive bids. A competitive bidder specifies an acceptable price and number of securities to be purchased. If the price determined at auction is above the bid, a competitive bidder will not be offered any securities. In contrast, a non-competitive bidder agrees to accept the price determined at auction and always receives securities.

A competitive bid process can be a single-price or multiple-price auction. In both cases, the issuer ranks bids by prices, choosing bids from highest to lowest until the desired issuance amount is reached. In a single-price auction, all wining bidders pay the same price and receive the same coupon rate for the bonds, regardless of their bid. A multiple price auction, on the other hand, generates different prices among bidders for the same bond issue. The single-price auction process may result in a lower cost of funds and broader distribution among investor. Multiple price auction may result in a narrower distribution of large bids because investors must accept bonds at their bid prices.

Sovereign governments appoint a group of financial intermediaries to serve as primary dealers, and they must participate in all auctions with competitive prices. Once issued, sovereign debt is typically traded on OTC markets by financial intermediary brokers/dealers in a manner similar to that of private sector debt securities.

Sovereign securities are classified into two categories based on when they were issued: on-the-run and off-the-run. On-the-run are recently issued sovereign securities that trade frequently. They are also called benchmark bonds because the yields of other bonds are determined relative to these bonds. Off-the-run refers to securities that were issued some time ago. They are less liquid compared to on-the-run securities.

Non-Sovereign, Quasi-Government, and Supranational Agency Debt

The level and type of non-sovereign government funding vary widely among countries, depending on whether specific goods and services are provided and financed at the national, regional, or local level.

Government Agencies

Government agencies are quasi-government entities that issue debt to fund specific public goods or services. For example, the Airport Authority of Hong Kong is a government agency that operates and develops the Hong Kong International Airport. This agency issues a combination of short-and-long term debt to meet the airport working capital and capital investment needs. The primary source of repayment is cash flows from airport operations, while its sovereign government backing is a secondary source of repayment.

Local and Regional Government Authorities

This category includes local governments such as states, provinces, and cities (i.e. all government authorities except the national government).

They may issue debt for general purposes known as general obligation bonds (GO bonds) which is repaid from local tax cash flows.

They may also issue debt for specific project financing (such as highways, bridges, or tunnels) known as revenue bonds. The source of repayment is usually linked to the project’s revenue stream (tolls, fees etc.) They are usually longer-dated with a maturity matching the expected life of the project being financed.

Supranational Organizations

Supranational organizations are created and supported by sovereign governments in pursuit of a common objective, such as fostering economic cooperation and development, promoting trade, or providing financing to emerging economies in pursuit of sustainable growth. Examples include the World Bank, IMF, Asian Development Bank etc.

Member states typically share decision-making authority and provide these organizations with implicit and explicit financial support, resulting in the highest credit quality among these issuers and a strong ability to access capital markets across maturities.