Markets for Corporate Issuers

Go to Fixed Income

Topics

Table of Contents

Introduction

- Short term funding alternatives available to corporations and financial institutions

- Repurchase (repo) agreements – their uses, benefits and risks

- Long term corporate debt – similarities and differences between investment grade and high yield issuance

Short-Term Funding Alternatives

Both non-financial corporations and financial institutions use borrowed capital to support their short-term activities.

External Loan Financing

Non-financial corporations often rely on financial intermediaries for short-term financing. Financial intermediaries can include both bank or non-bank lenders.

The main type of financing options available through these sources are:

- Uncommitted lines of credit – They are the least reliable form of bank borrowing. The bank can refuse to honor the request to use the line.

- Committed lines of credit – The bank makes a formal commitment to honor the line of credit. They are unsecured and prepayable without penalty. Unlike uncommitted lines, regular lines require compensation. Banks typically charge a commitment fee e.g., 0.50% of the full amount or the unused amount of the line.

The interest rate charged is usually the bank’s prime rate or a money market rate + a spread that depends on the borrower’s creditworthiness. These lines are usually in effect for 364 days.

- Revolving credit agreements (Revolvers): They are the most reliable form of short-term bank borrowing. They involve formal agreements similar to those used for regular lines of credit. Revolvers differ from regular lines in two ways

- (1) they are in effect for multiple years

- (2) they are often used for much larger amounts

- Secured (“asset-based”) loans: Secured loans are loans in which the lender requires the company to provide collateral in the form of assets. For example, a company can use its accounts receivables as a collateral to generate cash flows through the

assignment of accounts receivable.

A company can also sell its accounts receivables to a lender (called a factor), typically at a substantial discount. This is called afactoring arrangement.

In an assignment arrangement, the company retains the collection responsibilities, whereas in a factoring arrangement, the company shifts the collection responsibilities to the lender (factor).

External, Security-Based Financing

Commercial Paper

It is a short-term, unsecured instrument typically issued by large, well-rated companies. It has maturities typically ranging from a few days to 270 days.

Most maturing commercial paper is paid with proceeds from newly issued commercial paper (or rolled over). This practice increases the risk that an issuer will be unable to issue new paper at maturity, a risk known as rollover risk.

To minimize rollover risk, issuers of commercial paper are often required to have a backup line of credit. The short duration, high creditworthiness of the issuing company, and the backup line of credit generally makes commercial paper a low-risk investment for investors.

Short-Term Funding Alternatives for Financial Institutions

Retail Deposits

One of the primary sources of funds for a bank is the money deposited by retail (like you and me) and commercial investors in their accounts. It is the lowest possible source of funding for a bank.

The three types of retail accounts and characteristics of each of these accounts are discussed below:

Demand deposits or checking accounts

- Depositors have access to funds anytime.

- The funds may be used to pay for transactions.

- Little or no interest is paid.

Savings accounts

- Depositors have access to funds.

- Unlike checking account, savings accounts pay an interest. But they do not offer the same transactional convenience.

Money market accounts

- Funds are available at short or no notice.

- Offer money market rates of return.

Short-Term Wholesale Funds

Central Bank Funds

- When a bank receives deposits from customers, a certain percentage of this money must be kept as a reserve with the national central bank. The amount a bank keeps as reserves varies based on its financial position: some have a deficit and some have a surplus.

- The funds stashed in the central bank by all banks are collectively known as the central bank funds market.

- Assume a bank is running low on cash and a customer wants to withdraw money from this bank. The bank has two choices.

- It may withdraw cash from its reserve account in the central bank to pay the customer, if it has sufficient funds.

- It may borrow money from banks that have a surplus in their accounts at the central bank.

- The funds, known as central bank funds, may be borrowed for a period up to one year at rates known as central bank funds rates.

- If the borrowing is for one day, it is called overnight funds.

- If it is for more than one day, then it is called term funds.

Interbank Funds

- Banks lend to and borrow from each other in the interbank market.

- It is an unsecured system of lending.

- The term may vary from overnight to one year.

- The reference rate at which they borrow is called the interbank offered rate or, they may borrow at a fixed interest rate.

- Often large banks publish two rates: one at which they borrow and one at which they lend.

Certificates of Deposit

- A CD is a savings instrument with a maturity date, a fixed interest rate, and can be issued in any denomination.

- The investor or bearer of the certificate receives an interest at the end of the deposit period. CDs can be issued to individuals, companies, trusts, funds, etc.

- There are two forms of CD: negotiable and non-negotiable CD.

- In a non-negotiable CD, the interest and deposit are paid at maturity. There is a penalty if the depositor withdraws funds before maturity.

- In a negotiable CD, depositors are allowed to sell the deposits before maturity.

- There are two types of negotiable CDs:

- Large-denomination CDs: CDs of denomination of $1 million or more; often traded among institutional investors.

- Small-denomination CDs: Lower denominations and meant for retail investors.

Commercial paper

- Like non-financial corporations, banks may also issue unsecured commercial papers.

- Some banks and financial institutions also commonly issue a secured form of commercial paper known as

asset-backed commercial paper(ABCP).

ABCP

This financing is not recorded on the balance sheet of the issuer and provides benefits to both the bank and investors.

When the commercial paper is issued, the bank receives cash and reduces its capital costs by providing undrawn backup liquidity rather than holding the short-term loans to maturity.

Investors buy a liquid, short-term note that pays interest and principal from a loan portfolio to which they would not otherwise have direct access.

Repurchase Agreements

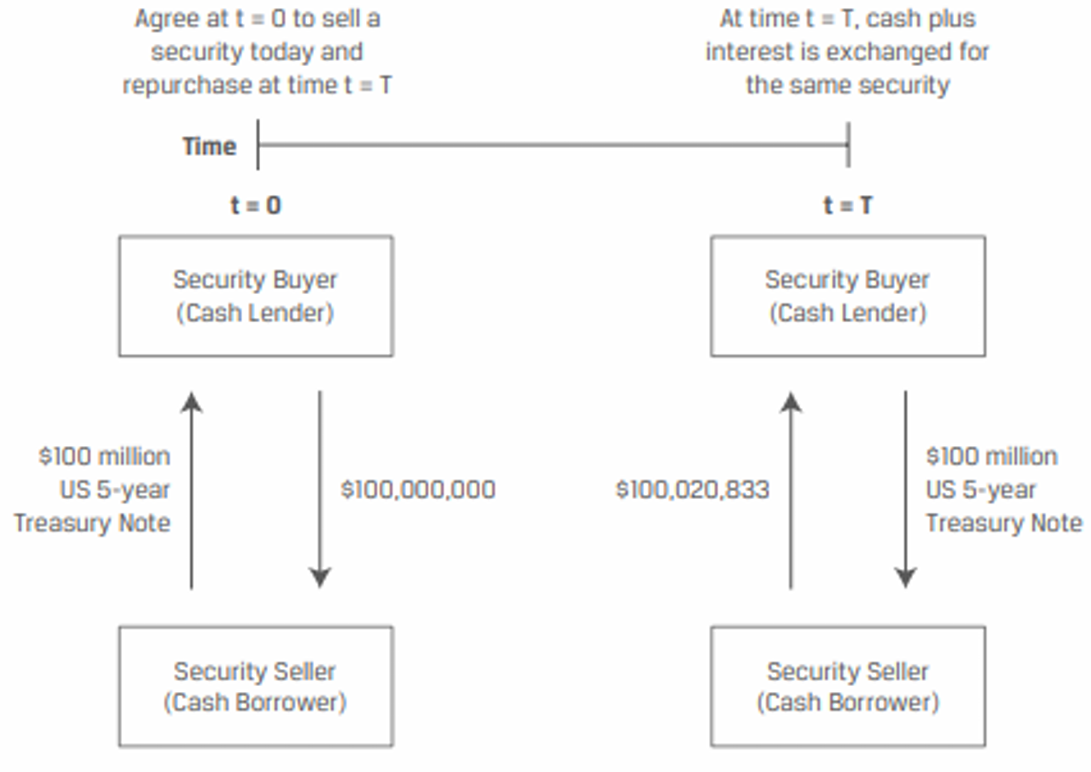

A repo is a sale and repurchase agreement. It is an agreement between two parties where the seller sells a security with a commitment to buy the same security back from the purchaser at an agreed-upon price at a future date. It is similar to borrowing funds against collateral.

Assume there are two parties: banks A and B. A has a 90-day T-bill that it sells to B for $99.50. It agrees to buy the same T-bill the next day for $99.51.

This was a means of borrowing $99.50 overnight for A. The 1¢ can be considered as the interest for the borrowed amount.

Structure of Repurchase and Reverse Repurchase Agreements

- Reverse repo: It was a repo arrangement from bank A’s (seller of security) perspective. But from bank B’s perspective (purchaser of security), it is a reverse repo.

- Repurchase price: The price at which A (dealer) will buy back (repurchase) the security from B the next day is called the repurchase price.

- Repurchase date: The date on which the dealer (A) repurchases the security (from B) is called the repurchase date.

- If the repurchase happens the next day, i.e., if the agreement is for one day, it is called overnight repo.

- If the repurchase happens after more than a day, it is called term repo.

- If the agreement is honored until maturity, then it is called repo to maturity.

- Repo rate: The interest rate negotiated between both the parties is called the repo rate. In our example, 1¢ was the interest paid.

The factors that affect the repo rate include:

- Risk of the collateral: Highly rated collateral (sovereign bonds) exhibit low risk and lower repo rates.

- Term of the repurchase agreement: The longer the term, the higher the rates.

- Delivery requirement: If the collateral is delivered to the lender, the rates are lower.

- Supply and demand: Collateral in high demand has lower repo rate.

- Interest rates of alternative financing.

Repos include features to reduce the risk of a collateral shortfall over the life of the contract.

- Initial margin: Provision of collateral in excess of the cash exchanged. $$\text{Initial Margin}=\frac{\text{Security Price}_0} {\text{Purchase Price}_0} $$An initial margin of 100% indicates a fully collateralized loan. A value greater than 100% represents an even greater initial collateral protection.

- Haircut: Values of initial margin greater than 100% can also be expressed in the form of a haircut, which is a reduction of the underlying loan relative to the initial collateral value. $$\text{Haircut} = \frac{\text{Security Price – Purchase Price }}{\text{Security Price }}$$

- Variation margin: As the value of the collateral changes over the life of the repo contract, additional collateral may be required to maintain a security interest equal to the original initial margin terms. $$\text{Variation Margin = Initial Margin} × [\text{Purchase Price}_t – \text{ Security Price}_t ]$$

Assume that today (t = 0) the current US five-year Treasury note trades at a price equal to the bond’s face value of USD 100,000,000. The security buyer takes delivery of the US Treasury note today and pays the security seller USD 100,000,000. If we assume a repo term of 30 days (and 360 days in a year) and an annual interest rate (or repo rate) of 0.25%, then the buyer agrees to return the Treasury note 30 days from today (t = T) to the seller at a repurchase price of USD 100,020,833, calculated as follows: $$100,000,000 × \left[1 + \left(\frac{0.25}{100} × \frac{30}{360}\right)\right] = 100,020,833$$

- Assume the repurchase agreement is subject to a 102% initial margin. Calculate the revised original purchase price (loan amount).

Purchase Price = USD 98,039,216.

- Calculate the associated repo haircut.

- Calculate the repurchase price using the same 30-day repo term and 0.25% repo rate.

Repurchase Price = USD 98,059,641.

- Calculate the variation margin five days after trade inception if the price of the five-year US Treasury note rises to 103% of the security’s USD 100 million face value.

Recall the original loan amount (or purchase price at t = 0) is equal to USD 98,039,216.