Issuance and Trading

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- Types of fixed income market segments

- Types of fixed-income indexes

- Primary and secondary fixed-income markets

Fixed-Income Segments, Issuers, and Investors

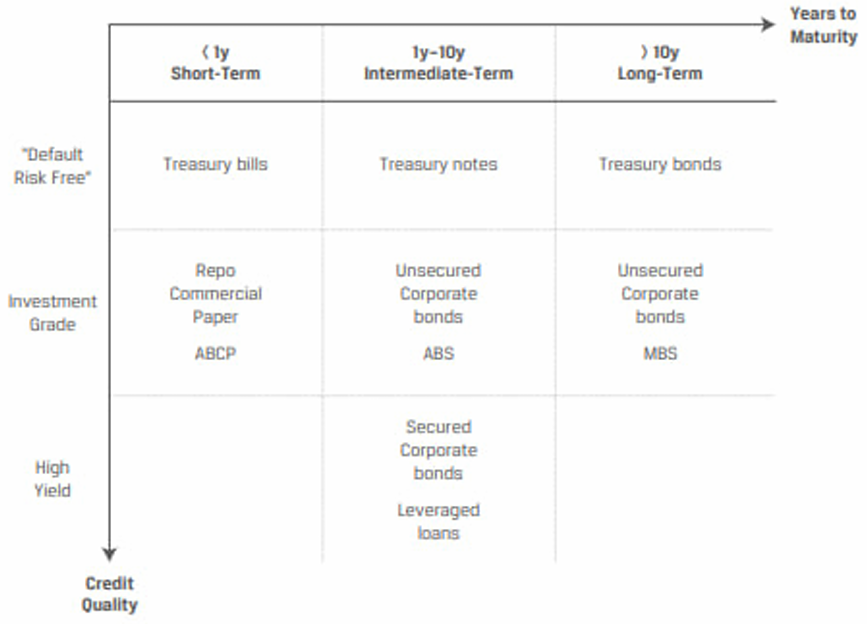

Fixed income markets are often categorized along three dimensions: issuer type, credit quality and time to maturity. Sometimes they may also be categorized along additional features such as currency, geography, and ESG characteristics.

Classification by Type of Issuer

Bond markets may be divided into four categories based on the type of issuers:

- Households

- Non-financial corporates

- Government

- Financial institutions

Classification by Credit Quality

Investors face credit risk, i.e., the risk of loss if the issuer fails to make timely payments of interest and principal as they come due. Rating agencies like Moody’s, S&P, and Fitch assign credit ratings to bonds.

Bonds with a rating of BBB or above are considered investment grade. Bonds below this rating are considered junk bonds.

This differentiation is important as certain investors such as banks and life insurance companies may not be allowed to invest in junk bonds but only in investment grade bonds.

Classification by Maturity

Fixed-income securities can also be classified by the original maturity of the bonds when they are issued:

- Money market securities: They are issued with a maturity at issuance that ranges from overnight to one year. For example, T-bills issued by the US government or commercial paper with short maturities issued by the corporate sector.

- Capital market securities: The original maturity is usually longer than a year.

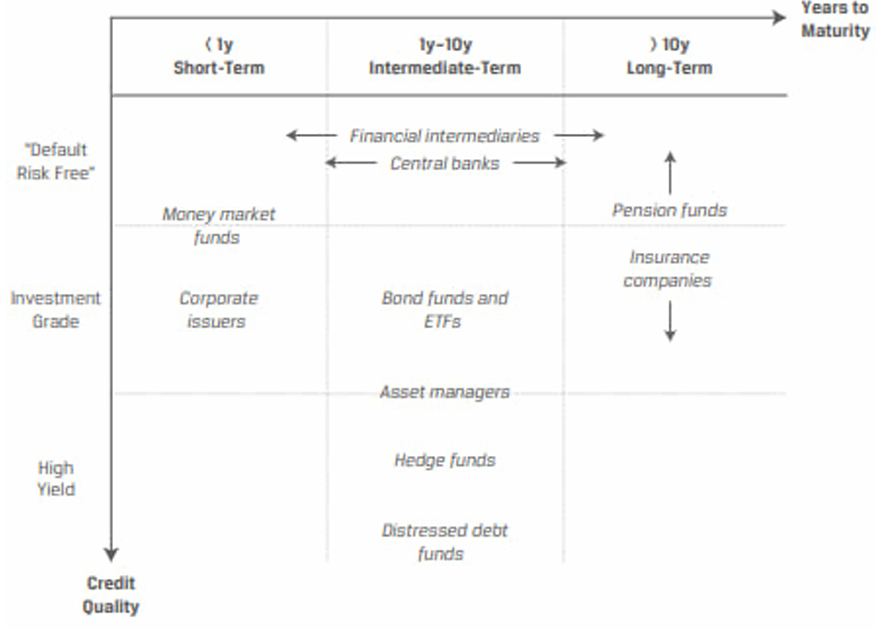

Fixed-income investors take positions across the credit and maturity spectrums in order to gain exposure to specific risks and match the cash flows of known future obligations.

Near-term obligations and liquid cash alternatives are often met with money market securities, while long-term bonds may be used to meet obligations further in the future or to achieve a higher expected return.

Pension funds and insurance companies with long investment time horizons prefer fixed-income instruments with fixed periodic coupon cash flows and a maturity profile that matches their long-term liabilities. Hedge funds and distressed debt funds may take additional credit risk at any point on the maturity spectrum to pursue higher expected return.

Sovereign government issuers typically have the lowest credit risk (and the highest credit rating – AAA).

Investment Grade Bonds

- Investors anticipate more consistent cash flows.

- Defaults are extremely rare.

- High-yield investors expect a higher return in exchange for assuming a higher risk of default.

Fixed-Income Indexes

Like equity market indexes, fixed income indexes also track the returns of groups of securities that meet their inclusion criteria.

Fixed income indexes can be used to evaluate market performance, benchmark the performance of investments and investment managers, and serve as the foundation for indexed investment strategies.

Fixed income indexes differ from equity indexes in three ways:

- In contrast to equities, where issuers typically issue just one or two instruments, issuers often have many fixed-income instruments outstanding → difficult to replicate.

(2021) → Apple Inc had a singe equity instrument but over 80 fixed income instruments outstanding.

- Because bonds have a finite maturity and new bonds are issued on a regular basis, fixed income index constituents change far more frequently than equity index constituents → frequent rebalancing.

- Similar to the market capitalization weighting used in equity indexes, bond indexes are also typically weighted by the market value of debt outstanding. Since bonds are issued by many types of issuers, broad bond indexes will reflect changes to bond market composition over time—for example, increases in public versus private issuer debt, longer maturities, and deterioration in credit quality.

Governments are usually the largest bond issuers in any market, therefore, many broad bond indexes have a high weight of government debt.

Because of the complexity of bond indexes, it is almost impossible to purchase all the constituent securities and a fund manager aiming to match the returns of an index will typically hold a representative sample of constituent securities.

Fixed-income indexes can be classified as broad-based, aggregate indexes with a vast number of constituents or narrower indexes that focus on criteria such as issuer type, credit quality, and time to maturity.

The most popular fixed-income indices include Barclays Capital Global Aggregate Bond Index, J.P. Morgan Emerging Market Bond Index, and FTSE Global Bond Index.

Primary and Secondary Fixed-Income Markets

Primary bond markets are markets in which bonds are sold for the first time by issuers to investors to raise capital. Bonds can be sold initially via a public offering or a private placement. Secondary bond markets are markets in which existing bonds are subsequently traded among investors. After the initial offering, bonds are bought and sold among investors in the secondary market.

Primary Fixed-Income Markets

A company/government/any entity issues bonds in two ways: public offering and private placement.

Public Offerings

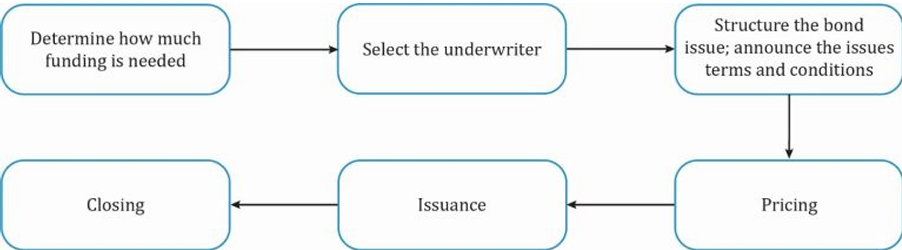

Any member of the public may invest in a new bond issue. The issuer does not sell bonds directly to each investor. Instead, the issuer avails the services of an intermediary called the underwriter to facilitate the selling (placement) process. The underwriter is usually an investment bank because banks have a good understanding of how to market a new issue, can tap their networks to locate investors, and successfully place the issue.

The different bond issuing mechanisms are:

- Underwritten offering

- Best effort offering

- Shelf registration

- Auctions

Underwritten offerings: An investment bank negotiates an offering price with the issuer; the offering price is the price at which the issue will be sold. It then buys the entire issue at the offering price and takes the risk of reselling it to investors or dealers (Firm commitment offering)

While small-size bond issue may be underwritten by a single investment bank, larger-size bond issues are often underwritten by a group (or syndicate) of investment banks. Such issues are called syndicated offerings. A lead underwriter heads the syndicate and the group collectively establishes the pricing of the issue and takes the risk of reselling it to investors or dealers.

Best effort offering: Investment bank acts as a broker and only sells as many securities as it can instead of committing to sell 100% of the issue. The unsold bonds are returned to the issuer. The investment bank gets a commission for bonds sold at the offering price, faces less risk and has less incentive to sell the issue than in an underwritten offering. Best effort offering is usually preferred for riskier issues and corporate bonds.

Shelf registration: Issuer is not required to sell the entire issue at once. The issuer files a single document with regulators that describe a range of future issuances. The advantage is that the issuer does not have to prepare a new document for every bond issue provided there is no change in the issuer’s business and financial terms stated in the prospectus. This allows the issuer to save on repeated administrative expenses and registration fees.

Auctions: Government bonds across the world are usually sold to investors via an auction. Governments finance public debt by borrowing money through the central bank. An auction is a public offering method that involves bidding, and is helpful in price discovery and allocating securities.

The United States follows a single-price auction method for its sovereign securities such as T-bills, T-notes, TIPS, etc. In this method, all winning bids pay the same price for the security and receive the same coupon rate.

Private Placement

Securities are not sold to the public in this type of funding. Instead, they are sold only to a select group of investors such as institutional investors.

Other characteristics are as follows:

- It is typically a non-underwritten, unregistered offering of bonds, i.e., a private issue need not comply with the registration requirements of a public offering such as preparing a prospectus.

- It is also exempt from securities laws that govern a public issue.

- It can be accomplished directly between the issuer and the investor(s) through an investment bank. Because privately placed bonds are unregistered and may be restricted securities that can only be purchased by some types of investors, there is usually no active secondary market to trade them.

- Institutional investors such as insurance companies and pension funds are typical investors of privately placed bonds.

Other points to note:

- Similar to primary equity issuance, which typically involves a transfer from private to public ownership, a first-time bond issuer is often replacing private debt, such as a bank loan, with bonds.

- Increasing the size of an existing bond with a price significantly different from par is referred to as the

reopeningof an existing bond. - Secured bond issuance by corporate high-yield, some special purpose entities, and other issuers is typically a more time-consuming and involved process than unsecured investment-grade bonds. Investors must become acquainted with unusual and complex covenants, as well as the use of operating cash flows and collateral as sources of bond repayment.

Secondary Fixed-Income Markets

Securities are traded among investors in the secondary market. Large institutional investors and banks are the primary participants. Retail investors are limited here, unlike in the equities market.

Unlike listed equities, for which secondary trading largely occurs on an electronic exchange, fixed-income markets consist mostly of quote-driven or over-the-counter markets.

It is important to understand the liquidity of a bond market:

- Liquidity is a measure of how quickly an investor can sell the bond and turn it into cash. Similarly, it should also measure how quickly one can buy a bond to cover a short position.

- Bid-ask or bid-offer spread reflects the liquidity (inversely) of a market.

- The most recently issued, on-the-run developed market sovereign bonds are typically the most liquid.

- Among corporate issuers, recently issued corporate bonds from frequent issuers with high credit quality have high liquidity. Whereas bonds of less frequent corporate issuers or more seasoned bonds of frequent issuers are rarely traded and have low liquidity.

Distressed debt refers to bonds issued by issuers who are on the verge of bankruptcy. Distressed debt typically trades in the secondary market at a price well below par.

Distressed debt is traded until either the corporate issuer’s assets are liquidated or its outstanding bonds are restructured. An equity security, on the other hand, may be removed or delisted from secondary trading on an exchange if it fails to meet the exchange’s listing requirements, which frequently include minimum share prices, net worth, and free float. By the time an issuer’s debt has become distressed, its equity securities will likely have already been delisted.