Fixed-Income Securitization

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- The benefits of securitization

- The securitization process – the parties involved and the roles they play

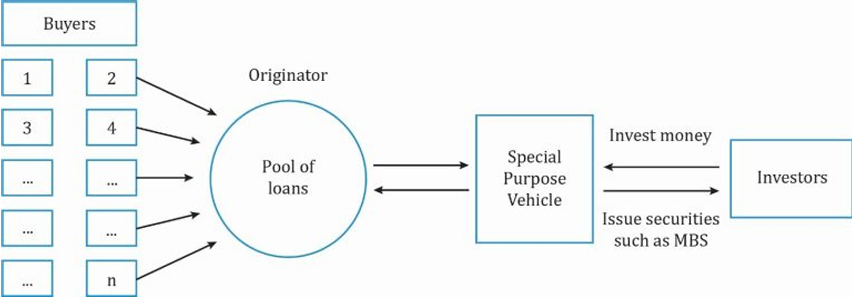

Asset-backed securities (ABS) are based on a principle called securitization. The securitization process involves pooling relatively straightforward debt obligations, such as loans or bonds, and using the cash flows from the pool of debt obligations to pay off the bonds created in the securitization process. The instruments which become part of the pool are called securitized assets.

In this illustration, a mortgage bank sells mortgage loans to thousands of homeowners. The mortgage bank bundles the individual loans into a pool which is sold to a separate legal entity generally referred to as a special purpose vehicle (SPV). The special purpose vehicle issues bonds to investors. The collateral for the bonds is the pool of mortgage loans.

The term mortgage-backed security (MBS) is commonly used for securities which are backed by high quality real estate mortgages. The term asset-backed securities, or ABS, is a broader concept that refers to securities backed by other types of assets. In the example above, we can say that the SPV issues MBS.

The Benefits of Securitization

In this section, we look at the benefits from the perspective of the three parties involved in the securitization process: borrowers who are the homeowners, investors who want to buy mortgages, and the intermediary connecting these two parties which is a commercial bank/financial institution.

Investors cannot lend directly to homeowners because they may be willing to lend/invest only a small amount of money, say $10,000, whereas the homeowner may require $100,000 as a mortgage loan. Second, the investor may not have all the information needed to assess the risk of the property.

Benefits to investors are as follows:

- Securitization converts an illiquid asset into a liquid security.

- It gives investors direct access to the payment streams of the underlying mortgage loans that would otherwise be unattainable.

- There are higher risk-adjusted returns to investors: pooling loans results in diversification and lower risk for investors.

- It gives investors an opportunity to buy a small part of the home buyers’ mortgage in the form of a security issued by the SPV.

- It gives exposure to the market, real estate in this example, without directly investing in it.

Benefits to the bank or loan originator are as follows:

- It enables banks to increase loan origination, monitoring, and collections.

- It reduces the role of the intermediaries (known as disintermediation) like the bank. However, note that an intermediary is still required to package and distribute securities.

- Banks have the ability to lend more money if the demand for ABS and MBS is high relative to if the money was self-financed (from deposits, debt, equity, etc.).

- There is greater efficiency and profitability for the banking sector: the mortgage-backed securities, at least in the US market, trade actively in the secondary market which improves the efficiency and liquidity of the financial market.

Benefits to the borrowers of the loan are as follows:

- It lowers the risk as the pooled loans offer a diversification benefit.

- The lower risk decreases the cost of borrowing for homeowners.

The Securitization Process

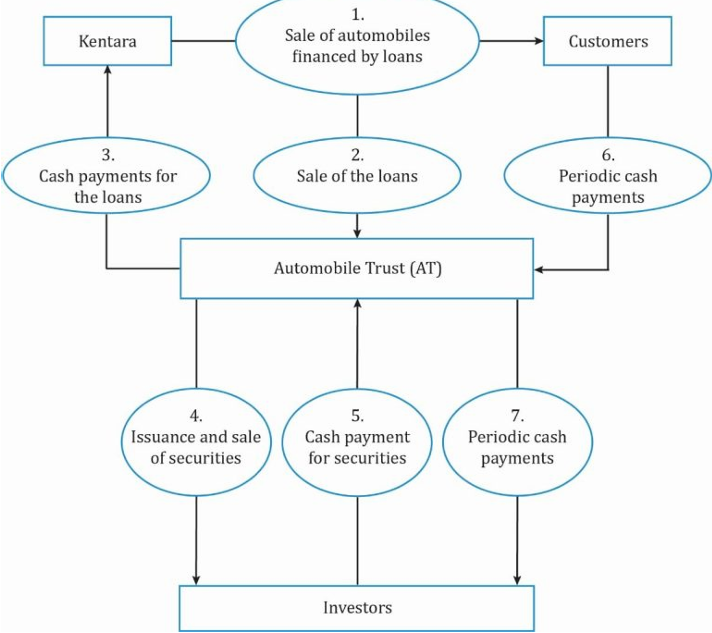

Kentara is a manufacturer of automobiles that range from $20,000 to $200,000. The majority of sales are made through loans granted by the company to its customers, and the automobiles serves as collateral for the loans. These loans, which represent an asset to Kentara, have maturities of five years, carry a fixed interest rate and are fully amortizing with monthly payments. Although the servicer of such loans need not be the originator of the loans, the assumption is that Kentara is the servicer.

Steps in the securitization transaction:

- Now assume that Kentara has $100 million of loans, shown on its balance sheet as an asset, and Kentara wants to raise another $100 million.

- Kentara can do this by securitizing the loans and sells them to a special purpose entity (SPE), Automobile Trust (AT).

- The SPE is a separate legal entity and is also called a special purpose vehicle (SPV) or a special purpose company. The legal form of the SPE varies by jurisdiction but, in almost all cases, the ultimate owner of the loans – AT – is legally independent and considered bankruptcy remote from the seller of the loans.

- AT gets $100 million in cash from investors by selling asset-backed securities, which it pays to Kentara.

- The customers who bought the automobiles on loan make monthly payments. AT uses this cash flow to pay investors of the ABS.

- Setting up a separate legal entity ensures that if Kentara files for bankruptcy, the loans backing the ABS that are issued by AT are secure within the SPE and creditors of Kentara have no claim on the loan.

Parties to a Securitization

| Party | Role |

|---|---|

| Seller of pool of securities | Originates the loans and sells to a special purpose entity (SPE). |

| SPE or Trust or Issuer | Buys the loans from the seller and issues ABS. |

| Servicer | Services loans such as collecting payments from borrowers, notifying borrowers who may be delinquent and, if necessary, seizing automobiles from borrowers who do not make payments on time. |

| Other parties involved include independent accountants, underwriters, trustees, rating agencies, and guarantors. |

- Lawyers: Responsible for creating the legal documentation.

- Underwriters: Facilitate bond issuance.

- Rating agencies: Rate the securities issued.

- Trustee: Safeguards the assets placed in the trust, and hold funds to be paid to bondholders.

Structure of Securitization

In the Kentara example, assume 100,000 securities of Bond Class A were issued with a par value of $1,000 per security to raise $100 million. All the certificate holders in this case are treated equal because there is just one class of bondholders and there is no distinction between bondholders with respect to payment time or credit risk.

However, in reality not all bond issues are created with a similar structure. The motivation for the creation of different types of structures is to redistribute prepayment risk and credit risk efficiently among different bond classes in the securitization.

Prepayment risk is the uncertainty that the actual cash flows will be different from the scheduled cash flows, as set forth in the loan agreements, because borrowers may alter payments to take advantage of interest rate movements.

Prepayment risk cannot be eliminated, but can be redistributed.

In the Kentara example, assume the buyers of automobiles are scheduled to make monthly payments towards the loan over 5 years. Instead, they prepay it in two years, perhaps because the interest rates decline, or due to any other reason. Since the loan is prepaid quicker than planned, the investors of ABS will also be paid quickly thereby reducing their interest income.

Time Tranching: Creation of bond classes to distribute the prepayment risk is called time tranching. Cash flow received from customers is distributed among the tranches based on certain parameters. For example, assume AT issued the following four bond classes, with a total par value of $100 million, instead of one bond class:

Since the motive is to distribute prepayment risk, the A1 class may have a lower prepayment risk than A4. If customers prepay, then A4 bond-holders will get prepaid before A1.

Subordination and Credit Tranching: Subordination is another layering structure in securitization. The bond classes differ in their exposure to credit risk, i.e., how they share losses if the borrowers of the original loans default.

An ABS is made up of a pool of loans. So, any default in payment will have a cascading effect on the investors. Here, several tranches of senior and subordinated classes are created and the credit risk is distributed to each class in a disproportionate manner based on the investor’s choice.

| Bond Class | Par Value |

|---|---|

| A (Senior) | 80 |

| B (Subordinated) | 14 |

| C (Subordinated) | 6 |

| In this example, all the losses are first absorbed by class C, then class B, and then class A. However, class C can accept a loss of up to $6 million. Beyond that, it is absorbed by class B. The risk is highest for class C and lowest for class A, in this example. Based on the high risk high return rule, the expected return of class C bondholders will be higher than that of class A bondholders. |

Role of SPE

The securitization of a company’s assets may include some bond classes that have better credit ratings than the company itself or its corporate bonds. Thus, in the aggregate, the company’s funding cost is often lower when raising funds through securitization than by issuing corporate bonds.

To understand why the funding cost is lower, we will go back to the Kentara example and consider two scenarios for raising $100 million: one in which Kentara issues a corporate bond, and another in which it issues ABS by securitizing loans/receivable.

Corporate bond scenario:

Kentara’s credit spread depends on the following two factors:

- Primarily, credit rating (BB, in this case).

- Collateral, to a lesser extent.

The cost of funding for Kentara will be higher if it issues a corporate bond, and not an ABS, for the following reasons:

- Higher risk: Investors perceive a higher risk given the company’s creditworthiness. In case the company goes bankrupt or is reorganized, their claim to assets will follow the absolute priority rule. Though, in reality the absolute priority rule has not been upheld in case of reorganizations. This means that it is not necessary for the bondholders to be paid off before the other parties (equity holders, other creditors). Hence, the credit spread for a corporate bond backed by a collateral does not decrease substantially.

- Higher return: To compensate for the high risk, investors expect a high return.

- Higher credit spread: Credit spread is the difference between the interest rate the issuer has to pay on the corporate bond and the benchmark interest rate. The riskier the bonds, the larger the spread demanded by investors as compensation for risk.

Securitization Scenario

- Funding cost is low: The collateral (loans/receivable) is legally an asset of AT. Any cash flow from the pool of loans will be paid to the investors of ABS. When an investor buys a bond class, he has to evaluate the credit risk of the class he is investing in. The credit rating of the bond class will depend on the quality of the collateral and capital structure of the SPV, and not the credit rating of the company as in the corporate bond.

- The lower the risk, the lower the funding cost: The assets belong to the SPV. If the company goes bankrupt, the absolute priority rule is followed. The principle is that senior creditors are paid in full before subordinate bondholders are paid anything. So, investors demand a lower return than a corporate bond. Lower return means lower funding cost for the issuer.

- The SPV is a bankruptcy-remote vehicle unlike corporate bonds. It means bankruptcy has no effect on an SPV. If the company goes bankrupt, the loans/receivable do not belong to Kentara anymore and the investors will be paid based on the securitization structure.