Credit Analysis for Government Issuers

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers special considerations for evaluating the credit worthiness of sovereign and other public issuers.

Sovereign Credit Analysis

Both sovereign and non-sovereign governments issue debt which is used to conduct fiscal policy and meet budgetary needs, such as providing public goods and services (e.g. infrastructure, health care, and education.) The primary source of repayment for sovereign debt is taxes and other government revenue such as fees, tariffs, and in some cases the profits of state-owned enterprises.

The ability of a sovereign government to tax all private economic activity within its jurisdiction is the primary reason that such bonds typically have the lowest credit risk of any issuer within a specific country. While sovereign bonds of advanced economies are often considered default risk-free, emerging and frontier market government bonds do involve default risk.

A combination of qualitative and quantitative factors can be used to asses a sovereign issuer’s ability and willingness to pay.

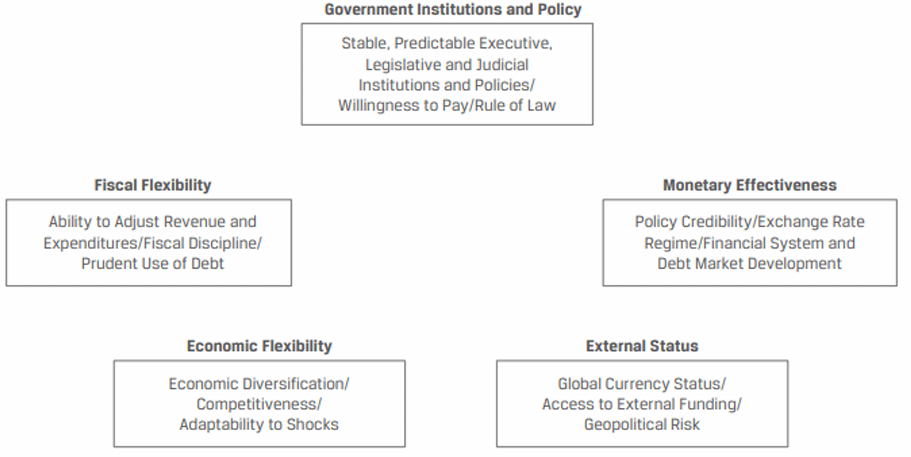

Qualitative Factors

Government Institutions & Policy: Do the sovereign government institutions and policies foster political and economic stability?

Policies range from basic legal protections (e.g., maintaining the rule of law, enforcement of property rights) to promoting a culture of debt repayment, transparency, the consistency of financial data reporting, and the relative ease of doing business.

Political factors include stability of domestic political institutions and the absence of conflict with neighboring countries. These factors are captured using a relative ranking or scoring approach, i.e., countries with better institutions and policies will get a higher rank.

In addition to a sovereign government’s ability to pay, we must also evaluate its willingness to pay. Willingness to pay is important because of the principle of sovereign immunity, which limits investor’s ability to force sovereign government to declare bankruptcy or liquidate its assets to settle debt claims.

Fiscal Flexibility:

- How well does a sovereign government establish and maintain fiscal discipline over time and under different economic conditions?

- Are tax collections properly enforced?

- Is the allocation to public expenditures prudent?

- Is the outstanding sovereign debt properly managed in relation to economic activity?

Monetary Effectiveness: Monetary policy is conducted by the central bank of a country. At one extreme, central banks may implement policy almost entirely independent of government intervention and influence; at the other extreme, they may simply act as the government’s agent.

Treasury reduces the likelihood that a sovereign government will monetize its domestic debt, raising domestic inflation and lowering the domestic currency’s external value.

Economic Flexibility: Key factors to gauge the economic flexibility of a country include not only the size of the economy and level of per capita income, but also the degree of economic diversification and growth potential.

Highest rated sovereign borrowers typically have an advanced and highly diversified domestic economy with strong, sustainable growth prospects. Whereas, emerging or frontier market economies often depend on a single industry or commodity. They may also have a sizable informal economy and may face challenges in collecting tax revenue.

External Status: How do a sovereign government’s international trade, capital, and foreign exchange policies influence its ability to support and service outstanding debt?

A key point to consider is whether a country’s domestic currency is considered to be a reserve currency, i.e., one that is fully convertible and frequently held by foreign central banks and other investors as a portion of their foreign exchange reserves. A reserve currency status greatly expands a government’s ability to access foreign investors using domestic currency debt. This flexibility minimizes the likelihood of sovereign default and increases a government’s ability to sustain higher level of debt.

In contrast, many emerging and frontier market countries have exchange rate restrictions, capital controls, and/or a lack of full convertibility, which limits their ability to borrow from foreign entities.

The factors are often interrelated, e.g., a weak legal system often goes hand in hand with a limited ability to collect taxes or enforce debt contracts.

Quantitative Factors

|

|

|

Fiscal Strength:

- Debt burden provides an indication of a government’s solvency. A higher debt burden indicates lower credit quality. Analysts should monitor whether a country’s debt burden is improving or deteriorating over time.

- Debt affordability provides a measure of debt coverage. A higher ratio indicates lower credit quality.

Economic Growth and Stability: These measures are important because larger, wealthier economies are better positioned to achieve sustainable growth and withstand economic and political shocks.

=External Stability:= These measures focus on the short- and long-term ability to generate sufficient, stable foreign currency cash inflows that can be used to meet interest and principal payments on external debt as well as other obligations to foreign investors.

Non-Sovereign Credit Risk

The main type of non-sovereign government issuers include agencies, public banks, supranational, and regional governments.

Agencies

Agencies are quasi-government entities whose primary function is to carry out a government-sponsored mission to provide public services, that is frequently based on a specific sovereign law or statute. For example, Airport Authority Honk Kong SAR (AAHK) is a statutory body owned by the Honk Kong SAR government that is responsible for operating and developing the Honk Kong International Airport.

Agencies can finance their activities using debt. Rating agencies typically grant agencies the same rating as the sovereign entity.

Government Sector Banks and Development Financing Institutions

Sovereign governments often sponsor the establishment of specialized financial intermediaries to operate in a specific market or to promote specific sovereign political, economic, social, or other growth and policy objectives. For example, Kreditanstalt für Wiederaufbau (KfW) is the largest national development bank established in the Federal Republic of Germany. It is 80% owned by the German federal government and 20% by the federal states.

These institutions also typically get the same rating as the sovereign entity.

Supranational Issuers

Supranational entities are organizations that are established and owned by sovereign governments that join as members to pursue a common objective. For example, the World Bank, Asian Development bank (ADB), the Development Bank of Latin America.

The rating of these entities depends on its members.

- The Indonesia Infrastructure Finance (IIF) was established by the Government of the Republic of Indonesia

- Gov of Republic of Indonesia (30%)

- World Bank (20%) + ADB (20%)

- KfW (15%) + Sumitomo Mitsui Banking Corporation (15%)

- IIF’s credit rating is BBB, equivalent to the sovereign rating of the Government of Indonesia.

Regional Government Issuers

This category includes provincial, state, and local governments. In the US, municipal issuers (state and local governments) are rated individually. They typically issue either general obligation or revenue bonds:

| General obligation bonds | Revenue bonds |

|---|---|

| - Unsecured and issued with the full faith and credit of issuing government. - Credit analysis focuses on employment, per capita income, per capita debt, tax base, etc. - Over-reliance on one or two types of tax revenue (e.g., capital gains or sales tax) can signal credit risk. |

- Issued for specific project financing like toll road, bridge, etc. - Credit analysis is similar to corporate bonds. - Higher risk because of a single source of revenue. - A key metric to calculate: debt-service-coverage ratio (DSCR), i.e., how much revenue to cover debt service payments. The higher the DSCR, the stronger the creditworthiness. |