Credit Analysis for Corporate Issuers

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- The qualitative and quantitative factors used to evaluate the creditworthiness of a corporate borrower

- Financial ratios used in credit analysis

- Seniority rankings of debt and their impact on credit ratings

Assessing Corporate Creditworthiness

The creditworthiness of a company primarily depends on its ability to generate profits and cash flows sufficient to meet interest and principal payments. A combination of qualitative and quantitative factors is used to evaluate a corporate’s creditworthiness.

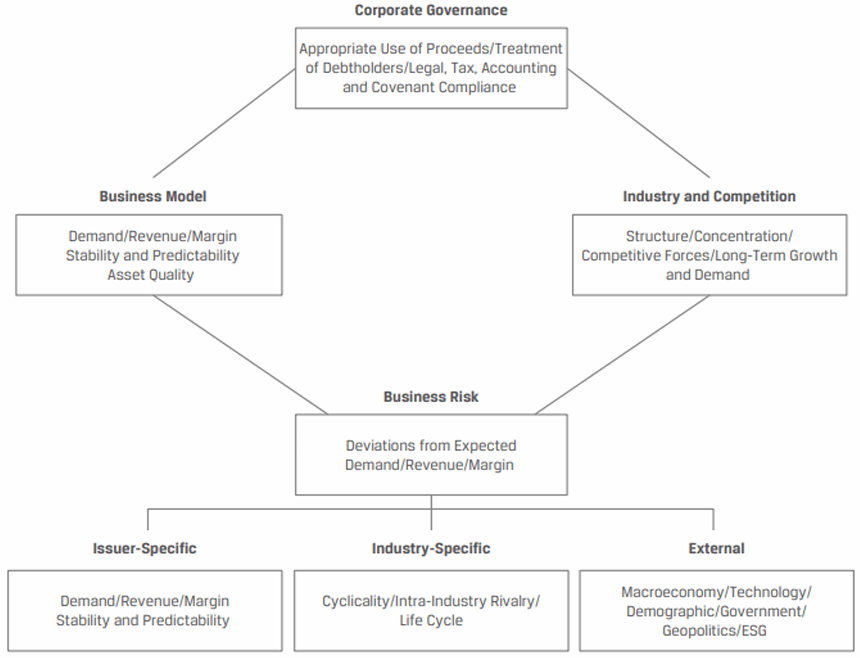

Qualitative Factors

Established firms with a business model characterized by stable and predictable cash flows, low business risk, and less competitive pressures have a greater capacity to use debt in their capital structure and a lower likelihood of default. In contrast, firms with lower and less stable cash flows, higher business risk, and/or greater competition have a lower capacity to use debt in their capital structure and a higher likelihood of default.

Equity vs Fixed Income Analysts: While equity analysts focus on all future cash flows, fixed-income analysts focus on how a company’s creditworthiness may change over a shorter time frame given the finite nature of debt claims.

Secured vs Unsecured Debt: In case of unsecured debt, the company cash flows are the primary source of repayment. In cash of secured debt, specific company assets are designated as collateral and serve as a secondary source of repayment. Secured lenders prefer to have tangible (or hard) collateral rather than intangible (or soft) collateral. The use of collateral and secured debt can reduce the cost of borrowing as compared to unsecured alternatives.

Corporate governance is also an important factor to consider in the analysis. Unlike shareholders who have voting rights on important company matters, debtholders seek to specify what borrower restrictions will apply and how the debt proceeds will be used at the time of issuance of debt. Analysts should also evaluate if the company uses aggressive accounting policies (e.g., use of significant off-balance sheet financing, capitalizing versus expensing items, early and premature revenue recognition). These items are considered potential warning flags.

Quantitative Factors

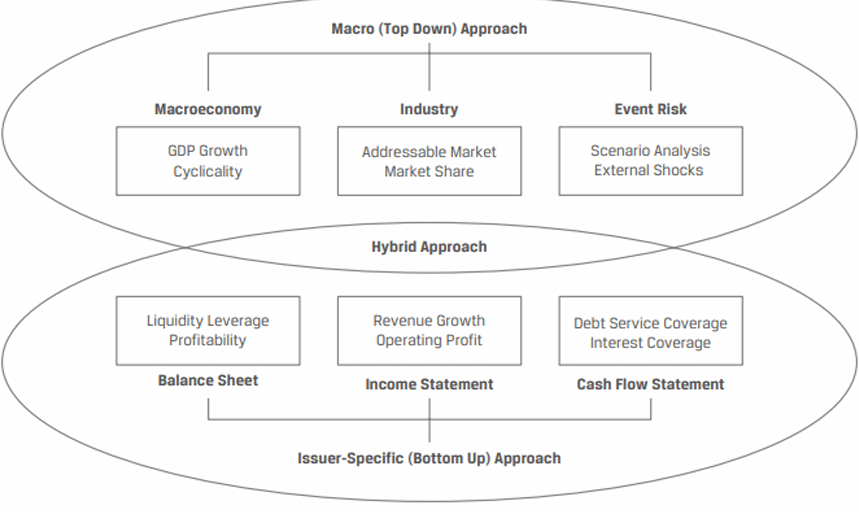

Top-down analysis typically begins with a macroeconomic forecast, which gauges a company’s growth relative to GDP, estimates a firm’s addressable market and market share, and assesses the likelihood and impact of potential adverse events.

Bottom-up analysis involves forecasting key revenue drivers and balance sheet positions.

A hybrid approach combines expected cyclicality with changing bottom-up features to forecast a company’s cash flows.

Financial Ratios in Corporate Credit Analysis

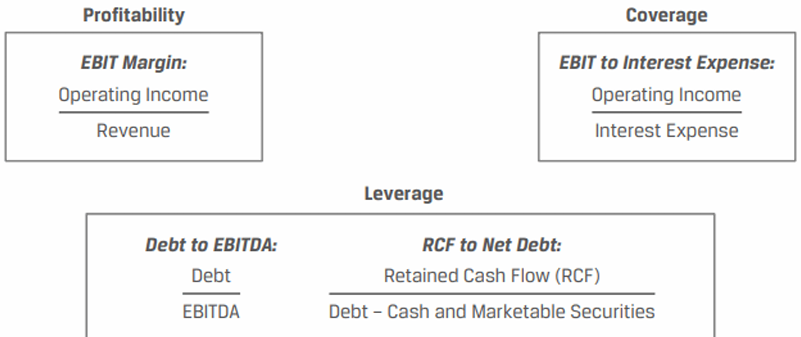

EBIT Margin: Earnings before interest and taxes (EBIT) helps determine a company’s operating performance prior to capital costs and taxes. Higher EBIT margins increases profits available to service debt.

EBIT to Interest Expense: This measures the degree to which operating profit covers periodic interest payments. A higher coverage ratio represents less credit risk.

Debt to EBIDTA: A higher debt to (Earnings before interest, taxes, depreciation and amortization) EBIDTA ratio indicates increased leverage and higher credit risk.

Retained Cash Flow (RCF) to Net Debt: This ratio focuses on cash flow rather than accounting earnings measures. The denominator uses ‘net debt’ which is debt reduced by available cash. A high RCF to net debt ratio implies lower leverage and lower credit risk.

The ratios are compared with the industry average and credit rating peers. Credit analysts also evaluate how these ratios may change over time as revenue drivers change.

Seniority Rankings, Recovery Rates, and Credit Ratings

Seniority Rankings

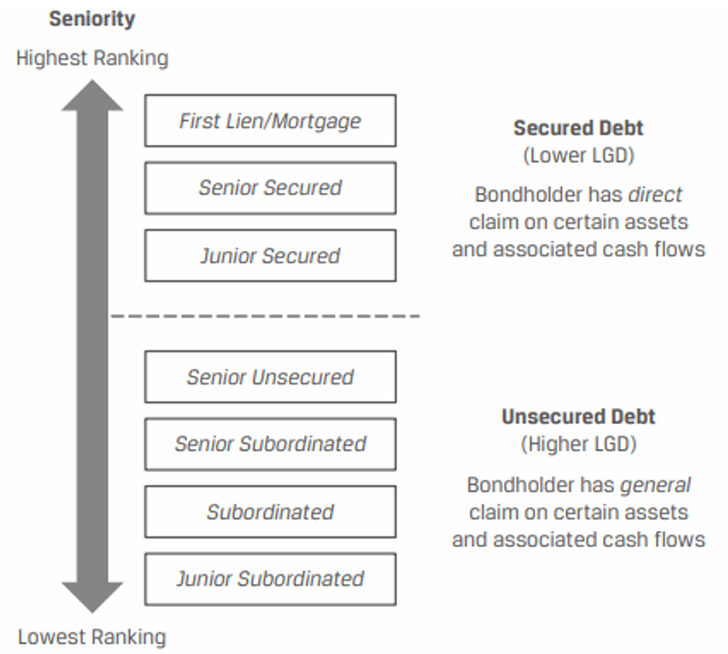

A single borrower may issue debt with different maturity dates and coupons. These various bond issues may also have different seniority rankings. Seniority ranking determines who gets paid first, or who has the first claim on the cash flows of the issuer, in the event of default/bankruptcy/restructuring. Bondholders are broadly classified into secured and unsecured.

- Unsecured bonds are known as debentures. They have a general claim on an issuer’s assets and cash flows.

- Secured bondholders have the first (direct) claim on cash flows in the event of a default.

- Priority of claims determines who gets paid first.

Secured versus Unsecured Debt

Within each category of debt, there are types and sub-rankings. Let us look at each of the items in detail now (in the order of priority for repayment):

Secured debt: Highest ranked debt in which some asset is pledged as collateral.

- First mortgage debt: A specific property is pledged.

- First lien debt: A pledge of certain assets such as buildings, patents, brands, property, and equipment, etc.

- Second lien: Some more assets could be pledged as a second lien to rank below the first mortgage/first lien. Most second lien loans are senior secured obligations of the borrower. They rank above the junior secured obligations.

Unsecured debt: Loss severity can be as high as 100%. Lowest priority of claims. No asset is pledged as collateral.

- Senior Unsecured

- Senior Subordinated

- Subordinated

- Junior Subordinated

Companies issue debt with different ranking for the following reasons:

- Cost effective: Secured debt has a lower cost due to reduced credit risk.

- Less expensive than equity: From a borrower’s perspective, even though the cost of issuing subordinate debt may not be as low as secured debt, it is less restrictive and is relatively less expensive than equity.

- Investors invest in subordinated debt because the higher yield compensates the high risk assumed.

Recovery Rates

Recovery rate is the % of the principal amount recovered in the event of default.

- Pari passu: All creditors at the same level of capital structure fall under the same class, and they will have the same recovery rates.

Assume there are two creditors in the senior secured class; one with a 3-year bond and the other with a 1-year bond. The debt of the 1-year bondholder matures in 3 months while the debt of the 3-year bondholder matures in 2.5 years.

If there is a default, both the investors will have the same recovery rates irrespective of the time left to maturity. This type of equal ranking for the same class of bonds is called pari passu (on equal footing).

- Vary by seniority ranking: If the seniority ranking is high, recovery rate will also be high.

- Vary by industry: If the industry is on a decline like the newspaper publishing industry, then the recovery rates will be low. There may be companies going bankrupt in industries during a recession (e.g., the steel industry in 2011-12), but in general the recovery rates here are higher than those on a decline.

- When they occur in a credit cycle: For instance, if a default happened in 2008 at the peak of the recent credit crisis, then the recovery rates would have been lower relative to, let us say, in 2004-05.

- Vary across industries and across companies within an industry.

- Priority of claims is not always absolute:

- Secured holders have a claim to cash flows/asset in the event of a default before anyone else. However, if the value of the pledged asset is less than the claim, then the unpaid amount becomes the senior unsecured claim.

- Unsecured creditors have a right to be paid before common/preferred shareholders.

- Senior creditors take priority over junior/subordinated creditors.

Issuer and Issue Ratings

Rating agencies provide two ratings:

- Issuer rating: This is based on the creditworthiness of the issuer. It applies to senior unsecured debt. Also known as corporate family rating (CFR).

- Issue rating: This rating is assigned to a specific debt/financial obligation. It takes into consideration the seniority ranking of the debt within the capital structure. Also known as corporate credit rating (CCR).

Cross-default provision: It is believed that the probability of default on one issue is linked to other issues of the same issuer. That is, a default on one issue triggers default on other issues with the same default probability.

Notching: A rating methodology to distinguish rating between different liabilities (bond issues) of an issuer. The objective is that two securities with the same rating should have the same expected loss rate (Probability of Default x Expected Severity Loss). Credit rating on issues can be moved up or down by a notch based on the risk of default/severity loss.

Factors the rating agencies consider while assigning ratings (notching up/down):

- Probability of default: Primary factor that drives the rating.

- Priority of payment: Who gets paid first in the event of a default; secured/senior unsecured/subordinated?

- Structural subordination: Issuer is a holding company rather than an operating company.

Assume both the holding company and each of its operating subsidiaries has issued bonds. The debt of the subsidiaries gets serviced by its cash flows and assets first before any of it can be passed on to the holding company. All else equal, debt issued by the holding company will have a lower rating than the debt issued by the subsidiary.