Cash Flows and Types

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- Common fixed income instrument cash flow structures and their implications for issuers and investors

- Legal, regulatory, and tax considerations faced by fixed income issuers and investors

Fixed-Income Cash Flow Structures

Not all bonds are structured to make periodic interest payments and one lump-sum principal payment at the end. In this section we will look at the different ways in which principal and interest can be paid over the bond’s life.

Principal Repayment Structures

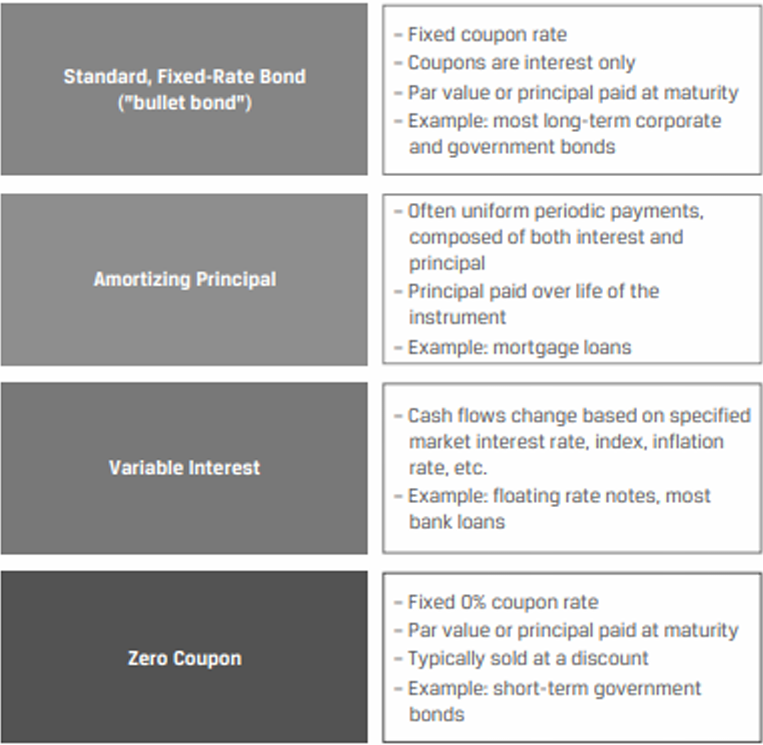

=Bullet bond:= The principal is paid all at once at maturity. Such a type of bond is called a bullet bond.

- No part of the principal is paid before maturity.

- The $1,000 amount towards principal is paid all at once at maturity. During the life of the bond, the principal remains outstanding.

- The last payment includes both the coupon payment of $60 and principal payment of $1,000.

Fully amortized: A fully amortized bond is one in which the principal is paid little by little in equal payments over the bond’s life, so that it is repaid in full by the maturity date.

Partially amortized: A partially amortized bond is one in which only a part of the principal is repaid over the bond’s life. The remaining big part of the principal is paid at maturity making it a balloon payment. This is a hybrid between the bullet and the fully-amortized bond.

$1,000 at 6 % annually

| Year | Cash Flow | Interest Payment | Principal Repayment | Outstanding Principal |

|---|---|---|---|---|

| 0 | -1000 | 1000 | ||

| 1 | 60 201.92 237.4 |

60 | 0 141.92 177.4 |

1000 858.08 822.6 |

| 2 | 60 201.92 237.4 |

60 51.48 49.36 |

0 150.43 188.04 |

1000 707.65 634.56 |

| 3 | 60 201.92 237.4 |

60 42.46 38.07 |

0 159.46 199.32 |

1000 548.19 435.24 |

| 4 | 60 201.92 237.4 |

60 32.89 26.11 |

0 169.03 211.28 |

1000 179.17 + 200 223.96 |

| 5 | 1060 201.92 237.4 |

60 22.75 13.44 |

1000 179.17 + 200 223.96 |

0 |

| Sinking Fund Arrangements | ||||

| This allows for full or partial amortization of a bond prior to its maturity. It specifies the portion of the bond’s principal outstanding that must be repaid each year throughout the bond’s life. |

- Standard: Issuer sends the repayment principal amount to the trustee. The trustee then either redeems bonds to this value or decides which bonds to retire through a lottery.

- Accelerated: Issuer retires more than the specified portion of the bond’s notional principal. The amount redeemed steadily increases each year. If there is any remaining principal, it is redeemed at maturity.

- Call provision: Bonds with call provision give the issuer the right to call (repurchase) the bond before maturity. Callable bonds usually have higher yields as investors bear the risk that they may be called. It is beneficial to the issuer and disadvantageous to the bondholder. The bonds to be retired are selected randomly.

A sinking fund arrangement results in

- Lower credit risk: The objective of a sinking fund provision is to reduce credit risk for investors because the issuer does not have to pay a large payment at maturity. From an investor’s perspective, there is less credit risk as the principal is being paid over the bond’s term.

- Higher reinvestment risk: Receiving principal payments before maturity also means the investor has to bear reinvestment risk, i.e., if the money received cannot be invested at the same or higher expected return. In a declining interest rate environment, there is a risk of investing the proceeds at a lower rate.

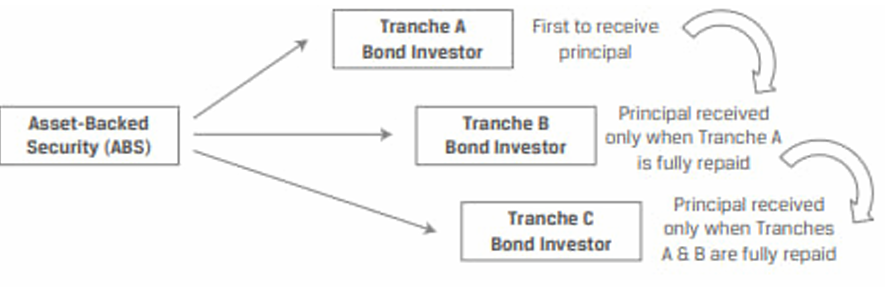

Waterfall Structures

This structure is commonly used in asset-backed securities (ABS) and mortgage-backed securities (MBS). Tranches with different priority of claims to the cash flows are created.

Interest payments are paid to all classed with no preference. However, the repayment of principal occurs sequentially – with the most senior tranche receiving principal payments first, followed by the second-highest tranche and so on.

Shortfalls in principal payment due to defaults are borne by the most junior tranches (since senior tranches are paid first). In the above diagram, Tranche A faces the lowest credit risk, while Tranche C faces the highest credit risk.

Coupon Payment Structures

Fixed Periodic Coupons

This is the most basic form of coupon payment. A fixed interest is paid either semi-annually or annually.

FRN a.k.a. Variable Interest Debt

- A bond whose coupon is set based on some reference rate plus a spread.

- FRNs can have floors (minimum interest rate), caps (maximum interest rate), or collars (both a minimum and maximum rate).

- An inverse FRN is a bond whose coupon has a negative relationship with the reference rate.

Other Coupon Structures

- Step-up coupons: Coupons increase by specified amounts on specified dates.

- Bonds with credit-linked coupons: Coupons change when the issuer’s credit rating changes.

- Bonds with payment-in-kind coupons (also called a split coupon bond): Issuer can pay coupons with additional amounts of the bond issue instead of cash.

- Bonds with deferred coupons: No coupons paid in the initial years but higher coupons paid later.

- Zero coupon bond: No coupon payments are made and the principal is returned at maturity. These bonds are generally issued at a large discount to their face value.

The difference between the issue price and the face value paid at maturity represents the cumulative interest that the investor will receive.

- Index-linked bonds: Coupon payments and/or principal repayments are linked to a price index, i.e., inflation-linked bonds. Examples of inflation-linked bonds include the following:

- Zero-coupon-indexed bonds: The inflation adjustment is made via the principal repayment only.

- Interest-indexed bonds: An index-linked coupon is paid during the bond’s life but nominal principal amount at maturity is fixed. This is essentially a floating-rate note in which reference rate is the inflation rate instead of a market rate.

- Capital-indexed bonds: Fixed coupon rate is paid but it is applied to a principal amount that increases in line with increases in the index during the bond’s life.

- Indexed-annuity bonds: The annuity payment, which includes both payment of interest and repayment of the principal, increases in line with inflation during the bond’s life. These are fully amortized bonds, unlike interest-indexed and capital-indexed bonds that are non-amortizing coupon bonds.

Fixed-Income Contingency Provisions

A contingency provision is a clause in a legal document that allows for some action if the event or circumstance does occur. It is also called an embedded option.

Callable Bonds

A callable bond gives the issuer the right to redeem all or part of the bond before the specified maturity date. Investors face reinvestment risk with callable bonds, as it is not possible to reinvest the proceeds at the previous higher interest rates. To compensate this risk to an extent, issuers offer a higher yield and sell at a lower price than the respective non-callable bonds.

Why companies issue callable bonds?

- To protect the issuer when market interest rates drop.

- Interest rates drop when market interest rates fall or the credit quality of the issuer improves. The issuer has an opportunity to call the old bonds and replace them with new cheaper bonds by saving on otherwise higher interest expenses.

- Companies also issue callable bonds to signal the market about their credit quality.

The following details about a callable bond are included in the indenture:

- Call price: Price paid by the issuer to the bondholder when the bond is called.

- Call premium: The amount paid on top of the face value as compensation to bondholders as they will have to reinvest proceeds at a lower rate.

- Call schedule: The dates and prices at which the bond may be called.

- Call protection period: During this period, a bond may not be called by the issuer. It is typically in the early days of a bond’s life to encourage investors to invest in the issue.

- Call date: The earliest date at which a bond may be called.

The three types of callable bonds based on exercise styles are listed below:

- American call: The issuer has the right to call the bond any time after the first call date.

- European call: The issuer has the right to call the bond only once after the first call date.

- Bermuda-style call: The issuer has the right to call the bond on specific dates after the call protection period.

Assume a hypothetical 20-year bond is issued on 1 December 2012 at a price of 97.315 (as a percentage of par). Each bond has a par value of $100. The bond is callable in whole or in part every 1 December from 2017 at the option of the issuer.

- 103.78 → 103.54 → 103.1 → 102.81 → 102.23 → 101.59 → 101.47 → 101.21 → 100.68 → 100.32 → 100

- What is the call protection period?

- What is the call premium (per bond) in 2021?

- What type of a callable bond is it most likely ?

Solution:

- 2017 – 2012 = 5 years.

- The call price in 2021 is $102.23 (102.23% × $100). The call premium in 2021 is $2.23 ($102.23 – $100).

- It is a Bermuda call. The bond is callable every 1 December from 2017 – that is, on specified dates following the call protection period. Thus, the embedded option is a Bermuda call.

Putable Bonds

A putable bond gives the bondholder the right to sell the bond back to the issuer at a pre-determined price on specified dates. Putable bonds offer a lower yield and sell at a higher price relative to otherwise non-putable bonds.

Putable bonds are beneficial to the bondholder because:

- When interest rates rise, bond prices fall. If the selling price is pre-specified, bondholders may put (sell) back the bond to the issuer at that price, which is higher than the market price when interest rates rise.

- Cash can be reinvested at higher rates.

The following details about a putable bond are included in the indenture:

- Redemption dates.

- Selling price: Usually equal to the face value of the bond.

- How many times the issuer allows bondholders to sell the bond during the bond’s life.

- One-time put: Gives bondholders a single sellback opportunity.

- Multiple put: More than one sellback opportunity available. Priced higher than one-time put bonds.

Like callable bonds, putable bonds are also classified into three, based on their exercise styles:

- American put: Bondholder has the right to sell the bond back to the issuer any time after the first put date.

- European put: Bondholder has the right sell the bond back to the issuer only once on the put date.

- Bermuda-style put: Bondholder has the right sell the bond back to the issuer only on specified dates.

Convertible Bonds

A convertible bond is a hybrid security with both debt and equity features. It gives the bondholder the right to exchange the bond for a specified number of common shares in the issuing company.

| Investor POV | Issuer POV |

|---|---|

| Opportunity to convert into equity if share prices are increasing and participate in upside. | Reduced interest expense; lower yield than otherwise non-convertible bond because of the conversion provision given to bondholders. |

| Downside protection if shares prices are falling. | Elimination of debt if conversion option is exercised. So, they do not have to repay the debt. |

| Usually callable. | |

| Some terms associated with the conversion provision are given below: |

- Conversion price: Price per share at which the convertible bond can be converted into shares.

- Conversion ratio: Number of shares that each bond can be converted into. $$\text{Conversion ratio} = \frac{\text{Par value}}{\text{Conversion price}} $$

- Conversion value: Current share price multiplied by the conversion ratio. It is also called the parity value. $$\text{Conversion value = Current share price} \times \text{Conversion ratio}$$

- Conversion premium: Difference between the convertible bond’s price and its conversion value. $$\text{Conversion premium = Convertible bond’s price – Conversion value}$$

Warrant: A warrant is an attached option, not an embedded option. It gives the bondholder the right to buy the underlying common shares at a fixed price called the exercise price any time before the expiration date.

Contingent Convertible (CoCo) Bonds: These are bonds with contingent write-down provisions. The bonds can be converted into equity contingent to a specific condition. For example, a CoCo bond might be allowed to be converted into equity only after it reaches a certain price.

Assume that a convertible bond issued in the UK has a par value of £1,000 and is currently priced at £1,200. The underlying share price is £56 and the conversion ratio is 25:1. What is the conversion condition for this bond?

Solution: The conversion value of the bond is £56 × 25 = £1,400. The price of the convertible bond is £1,200. Thus, the conversion value of the bond is more than the bond’s price, and this condition is referred to as above parity.

Legal, Regulatory, and Tax Considerations

Legal and Regulatory Considerations

Fixed-income securities are subject to different legal and regulatory requirements depending on where they are issued and traded. National bond market is the bond market in a particular country.

- Domestic bonds: These are bonds that are issued and traded in a country, and denominated in the currency of that country. Bonds in domestic currency issued by a company incorporated in that country are called domestic bonds. For example, bonds denominated in Yen, issued by Toyota to be traded in Japan.

- Foreign bonds: These are bonds issued by a foreign company but traded in the domestic market. For example, bonds denominated in USD issued by the Australian Rio Tinto Group.

Eurobonds are issued internationally, outside the jurisdiction of any single country and are denoted in currency other than that of the countries in which they trade. They are subject to less regulation than domestic bonds.

Bearer Bonds versus Registered Bonds

In the case of bearer bonds, the trustee does not maintain a record of who owns the bonds. That information is recorded in the clearing system.

In the case of registered bonds, records of who owns the bond are maintained using a name or serial number.

In the past, Eurobonds were typically bearer bonds. However, nowadays, Eurobonds as well as domestic and foreign bonds are registered bonds.

Global Bonds

Bonds that are issued simultaneously in multiple markets, such as the Eurobond market and in at least one domestic bond market. This ensures sufficient demand for the issue irrespective of the investors’ location.

Sukuk

Sukuk are fixed-income instruments developed in accordance with Islamic law. Payment of interest and financing of sectors such as alcohol or gambling is prohibited. Instead of interest, Sukuk pay investors a rental cash flow (or a profit rate) from the underlying assets.

Tax Considerations

There are two sources of return from a bond: income from coupon payments and capital gain. The way these two components are treated for tax purposes is different.

- The income portion of a bond investment is generally taxed at the ordinary income tax rate. For example, if you fall under the 30% income tax category, then the coupon income will be taxed at this rate.

- Assume you buy a bond for $900 and later sell it for $1,000. This $100 is considered capital gain. Tax on capital gain may be different for long-term and short-term investments. Often, the tax rate for long-term capital gains is lower than that for short-term capital gains.

- In some countries, a pro-rated portion of discount may be included in interest income. For example, assume you buy a 3-year zero-coupon bond, with a par value of $1,000, at $900. The gain of $100 is over three years. Now, the taxing authority in some countries such as the U.S. may decide to tax this $100 gain on a pro-rata basis over three years instead of taxing it all at once at the end of three years.