Bond Valuation - Prices and Yields

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- How to price a bond on or between coupon dates

- Relationship between a bond’s price and bond features such as coupon rate, maturity, and yield-to-maturity

- Matrix pricing

Bond Pricing and The Time Value of Money

Bond Pricing with a Market Discount Rate

A bond’s price is the present value of all future cash flows at the market discount rate. The discount rate is the rate of return required by investors given the risk of investment in the bond. It is also known as the required yield, or required rate of return.

The present value of the bond (91.575) is lower than the par value of the bond (100).

Premium, Par, and Discount Bonds

Assume we have another bond with a coupon rate of 8%, paid annually. If the market discount rate is again 6%, what is the price of the bond?

Coupon rate here is higher than the market rate. [Premium Bond]

PV = -108.425.

In this case, the present value of the bond is higher than its par value. Such a bond is called a premium bond.

What if the coupon rate is 6%? [Par Bond]

PV = -100.

The present value is equal to the par value of the bond.

What if the coupon rate is 2%? [Discount Bond]

PV = -83.151.

This type of bond, which sells at a price below its par value, is called a discount bond.

Yield-to-Maturity

The yield to maturity (YTM) is the internal rate of return on the cash flows – the uniform interest rate that will make the sum of the present values of future cash flows equal to the price of the bond. It is the implied market discount rate.

In simpler terms, it is a bond’s internal rate of return – the rate of return on a bond including interest payments and capital gain if the bond is held until maturity. Yield to maturity is based on three important assumptions:

- The investor holds the bond to maturity.

- The issuer does not default on payments and pays coupon and principal as they come due.

- The investor is able to reinvest all proceeds (coupons) at the YTM.

This is an unrealistic assumption as the interest rates may increase or decrease after the bond is purchased. So, the coupon may be reinvested at a higher or lower rate.

A $100 face value bond with a coupon rate of 10% has a maturity of 4 years. The price of the bond is $80. What is its yield to maturity?

The bond is trading at a discount. So, the coupon rate (10%) must be lower than market rate (17.34%).

| Bond | Coupon Payment per Period | # of Periods to Maturity | Price | YTM |

| ---- | ------------------------- | ------------------------ | ------ | ----- |

| A | 2.5 | 3 | 102.8 | 1.54% |

| B | 2 | 5 | 97.76 | 2.48% |

| C | 0 | 48 | 23.425 | 3.07% |

Flat Price, Accrued Interest, and the Full Price

When a bond is between coupon dates, its price has two parts: flat price and accrued interest. The sum of the two parts is called the full price or dirty price.

Full price or dirty price = Flat price + Accrued interest

where:

- t = # of days since the last coupon payment

- T = # of days between coupon payments

- PV = Present value of the bond (not the flat price)

A 5% French corporate bond is priced for settlement on 14 July 2015. The bond makes semi-annual coupon payments on 1 March and 1 September of each year and matures on 1 September 2020. Assuming a 30/360 day count convention for accrued interest, calculate the full price, the accrued interest, and the flat price per EUR 100 of par value for the following three yields to maturity: (I) 4.75%, (II) 5.00% and (III) 5.10%.

Solution

Given the 30/360 day-count convention, there are 134 days between the last coupon on 1 March 2015 and the settlement date on 14 July 2015 (120 days for full months of March, April, May, and June, plus 14 days in July). Therefore, the fraction of the coupon period that has gone by is assumed to be 134/180. At the beginning of the period, there are 11 periods to maturity.

| Stated YTM | Price at Beginning | Full Price | Accrued Interest | Flat Price |

| ---------- | ------------------ | ---------- | ---------------- | ---------- |

| 4.75 | 101.198 | 102.979 | 1.861 | 101.118 |

| 5 | 100 | 101.855 | 1.861 | 99.9942 |

| 5.1 | 99.5256 | 101.4088 | 1.861 | 99.5478 |

The flat price of the bond is a little below par value, even though the coupon rate and the yield to maturity are equal, because the accrued interest does not take into account the time value of money. The accrued interest is the interest earned by the owner of the bond for the time between the last coupon payment and the settlement date.

However, that interest income is not received until the next coupon date. The calculation of accrued interest in practice neglects the time value of money. Therefore, compared to theory, the reported accrued interest is a little

too highand the flat price is a littletoo low.

Relationships Between Bond Prices and Bond Features

In this section, we will study the relationship between the bond price and market discount rate. The underlying principle is that a bond’s price changes whenever there is a change in market discount rate.

Inverse Effect and Convexity Effect

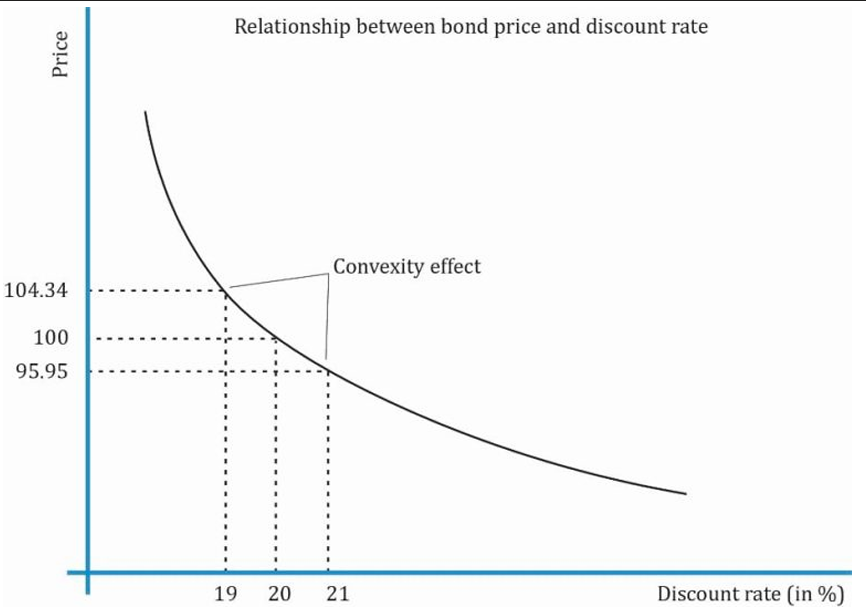

The bond price is inversely related to the market discount rate. This is called the inverse effect.

Remember that the price-yield relationship of a bond is not a straight line. Also note that price changes are not linear for the same amount of change in discount rate. At an interest rate of 20%, the price of the bond is 100. If the interest rate decreases from 20% to 19%, the bond price increases by 4.34%. However, if the interest rate increases from 20% to 21%, the bond price decreases by only 4.05%. This difference in price change is called the convexity effect.

Coupon Effect

The bond with lowest coupon rate has the highest interest rate sensitivity. In other words, a 1% change in interest rates causes a greater % change in the price of bond A (10% coupon) relative to bonds B (20% coupon) and C (30% coupon). This is called the coupon effect.

Maturity Effect

For the same coupon rate, a longer-term bond has a greater percentage price change than a shorter-term bond when their market discount rates change by the same amount. This is called the maturity effect.

Low-coupon and Long-term bonds are more sensitive to changes in discount rates.

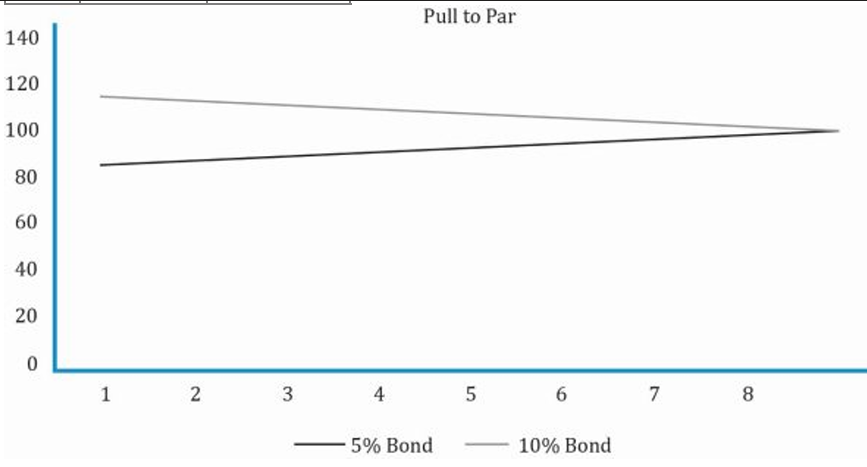

Constant-Yield Price Trajectory

Even if the yield stays constant, bond prices change and come closer to par as time passes and as they near maturity date. The constant-yield price trajectory illustrates the change in a bond’s price over time if yields remain constant. This trajectory shows the pull to par effect.

For a premium bond, the price decreases over time to par and for a discount bond, the price increases over time to par.

Both bonds have a market discount rate of 7.5%. The 5% bond’s initial price is 85.3567 and the 10% bond’s initial price is 114.6433.

| Yr | 5% Bond | 10% Bond | Yr | 5% Bond | 10% Bond |

|---|---|---|---|---|---|

| 1 | 85.3567 | 114.6433 | 5 | 91.6267 | 108.3733 |

| 2 | 86.7585 | 113.2415 | 6 | 93.4987 | 106.5013 |

| 3 | 88.2654 | 111.7346 | 7 | 95.5111 | 104.4889 |

| 4 | 89.8853 | 110.1147 | 8 | 97.6744 | 102.3256 |

|

If the yield stays constant:

- A premium bond’s price decreases to par value as its time to maturity approaches zero.

- A discount bond’s price increases to par value as its time to maturity approaches zero.

- A par bond’s value remains unchanged as it approaches maturity.

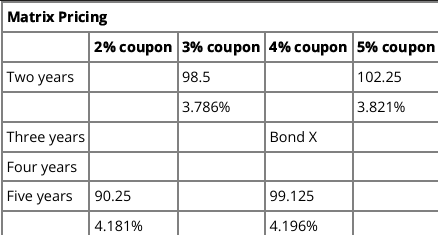

Matrix Pricing

Matrix Pricing Process

One can easily get information at what price a stock is trading. But it is not easy to determine the price of most bonds as they do not trade as often as equity. Matrix pricing is an estimation process to find the market price of a not-so-frequently traded bond based on the prices of comparable bonds with similar times to maturity, type of issuer, coupon rates, and credit quality. This is also applicable for bonds that have not been issued yet.

There are five steps to determine the value of a bond using the matrix pricing method:

- Determine the YTM of comparable bonds, which is given to us already. If it were not given, you can calculate the YTM using the price and coupon.

- Determine the average yield for two-year bonds = 0.038035

- Determine the average yield for five-year bonds = 0.041885

- Calculate the three-market discount rate using linear interpolation. We have the data (yield) for two-year and five-year bonds, but not a three-year bond. From the graph you can see that the YTM of a three-year bond = 0.038 + x.

x can be calculated as

Discount rate for the three-year bond = 3.39%.

5. Using 0.039318 as the discount rate, compute the price for the three-year bond → PV = -100.1906.

A few points to be noted on matrix pricing:

- Matrix pricing is used when underwriting new bonds to estimate the required yield spread over the benchmark rate.

- Benchmark rate is a market reference rate, or a government bond with the same maturity as the bond being priced.

- Assume the YTM for a new bond is calculated using the matrix pricing method as 2.2% and a comparable government bond has a yield of 2.0%. The difference between the yield on a new bond over its benchmark rate is called the required yield spread or spread over the benchmark. In this case, it is 0.2%.

- Yield spreads are always specified in basis points where 1 basis point is one-hundredth of a percentage point. In this case, it is 20 basis points.

An analyst decides to value an illiquid 3-year, 3.75% annual coupon payment corporate bond. Given the following information and using matrix pricing, what is the estimated price of the illiquid bond? (2-year, 4.75% annual coupon payment bond priced at 105.60 and 4-year, 3.5% annual coupon payment bond priced at 103.28.)

Solution: The required yield on the 2-year, 4.75% bond priced at 105.60 is 1.871%. The required yield on the 4-year, 3.50% bond priced at 103.28 is 2.626%. The estimated market discount rate for a 3-year bond having the same credit quality is the average of two required yields: (1.871% + 2.626%)/2 = 2.249%.

The estimated price of the illiquid 3-year, 3.75% annual coupon payment corporate bond is 104.3078 per 100 of par value. $$\sum_{i=1}^{i=3} \frac{3.75}{1.02249^i} + \frac{100}{1.02249^3} = 104.3078$$