Asset-Backed Security (ABS) Instrument and Market Features

Go to Fixed Income

Topics

Table of Contents

Introduction

This learning module covers:

- Covered bonds

- Typical credit enhancement structures used in securitizations

- Non-mortgage asset-backed securities

- Collateralized debt obligations

Covered Bonds

Covered bonds are senior debt obligations issued by a financial institution and backed by a segregated pool of assets that typically consist of commercial or residential mortgages or public sector assets.

Covered bonds are similar to ABS, but they differ because of their:

- Dual recourse nature: Investors have claims against both the issuing financial institution and the underlying asset pool.

- Balance sheet impact: The underlying asset pool remains on the issuing financial institution’s balance sheet. It is not transferred to a separate SPV. The covered pool bondholders retain a top-priority claim against the pool.

- Dynamic cover pool: The underlying asset pool is not static. The issuing financial institution must replace any prepaid or non-performing assets in the cover pool to ensure sufficient cash flows until maturity. In contrast, ABS pass through default and prepayment risk to investors.

- Redemption regimes in the event of sponsor default: In the event of sponsor default, redemption regimes align the covered bond’s cash flows as closely as possible to the original maturity schedule.

- In the case of hard-bullet covered bonds, if payments do not occur according to the original schedule, a bond default is triggered and bond payments are accelerated.

- Soft-bullet covered bonds delay the bond default and payment acceleration of bond cash flows until a new final maturity date, which is usually up to a year after the original maturity date.

- Conditional pass-through covered bonds convert to pass-through securities after the original maturity date if all bond payments have not yet been made.

Because of these additional safety features, covered bonds usually have lower credit risks and therefore lower yields as compared to otherwise similar ABS.

ABS Structures to Address Credit Risk

Credit Enhancement

Three main types of internal credit enhancements widely used in securitization transactions are:

- Overcollateralization: The value of the collateral exceeds the face value of the issued bonds. This provides a safety cushion to investors.

- Excess Spread: This is the difference between the coupon on the underlying collateral (say 8%) and the coupon paid on the securities (say 6%). The excess spread (8% – 6% = 2%) can absorb collateral shortfall or be used to build up reserves.

- Subordination or Credit Tranching: More than one bond class or tranches are created, and they differ in how they share any losses resulting from defaults in the collateral pool.

External credit enhancements like financial guarantees by banks or insurance companies, letters of credit, and cash collateral accounts are also commonly used.

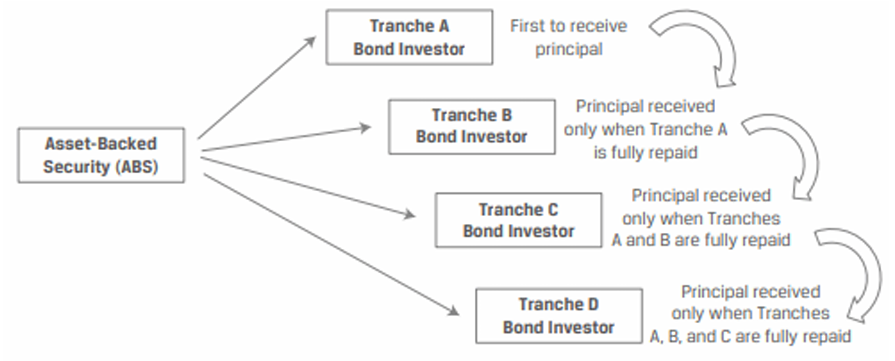

Credit Tranching

The four tranches have differing yields and degrees of risk, and they are affected differently in the event of a default.

Class A, the most senior investor tranche with the highest ranking in the capital structure, receives principal payments first, carries the least risk, and provides the lowest return. Class B mezzanine tranche assumes slightly higher risk but offers higher returns. Class D absorbs losses first and has the highest risk, but also the highest potential yield. Because of the residual nature of its claims to cash flows from the asset pool, the lowest tranche is sometimes referred to as the equity tranche.

Non-Mortgage Asset-Backed Securities

A wide range of assets apart from mortgage loans are used as collateral for asset-backed securities (e.g. auto loans, credit card receivables, personal loans, commercial loans).

Based on the way the collateral pays, ABS can be categorized into two types:

- Amortizing (Mortgage loans and automobile loans)

- Non-Amortizing (Credit card receivables)

This learning module focuses on credit card receivable ABS and a residential solar ABS.

Credit Card Receivable ABS

Credit cards such as Visa and MasterCard are used to finance the purchase of goods and services, as well as for cash advances. When a cardholder makes a purchase using a credit card, he is agreeing to repay the amount borrowed (purchase amount) to the issuer of the card within a certain period, typically a month.

If the outstanding amount is not repaid within this grace period, then a finance charge (interest rate) is applied to the balance not paid in full each month. Credit card receivables are pooled together to act as a collateral for credit card receivable-backed securities.

Cash flow, on a pool of credit card receivables consists of:

- Finance charges: These represent the periodic interest the credit card borrower is charged on the unpaid balance after the grace period.

- Fees and principal repayments. Fees include any late payment fees and any annual membership fees.

Characteristics of Credit Card Receivable-Backed Securities

Payment Structure

- The security holders are paid an interest periodically (e.g., monthly, quarterly, or semiannually). The interest rate may be fixed or floating.

- The principal payments made by borrowers do not flow through to investors during a period known as the lockout period. Instead, the repayments are reinvested to issue new loans. As a result, credit card receivables increase during the lockout period. During this period, the cash flow to security holders comes from finance charges and fees.

Amortization Provision

- Credit card receivable-backed securities are non-amortizing loans. The principal is not amortized during the lockout period.

- Certain provisions in credit card receivable-backed securities require early amortization of the principal if certain events occur. Such provisions are referred to as

early amortizationorrapid amortizationprovisions and are included to safeguard the credit quality of the issue. The only way the principal cash flows can be altered is by triggering the early amortization provision.

If issuers believe there may be a default in credit card repayments, then the principal repayments will be used to pay security holders (investors) instead of reinvesting to issue new loans.

Solar ABS

An increasing number of homeowners are installing solar energy systems, so many specialty finance companies have begun to offer specialized home improvement financing options: solar loans or solar leases. Solar loans involve borrowing money to purchase the system from an installer. Solar leases involve renting equipment directly from a solar company.

A solar ABS is created by securitizing solar loans. They have captured the interest of institutional investors because they provide the opportunity to contribute to sustainability while generating attractive risk-adjusted yields. Institutional investors looking for ESG or climate finance investment alternatives can invest in solar ABS.

ABS are typically collateralized by the underlying debt, such as mortgages, loans, or receivables. The loans can be further secured by pledging a lien on the installed systems, the property itself, or both. This effectively makes them a junior mortgage on the property and increases their safety for investors.

Solar loan borrowers are typically prime borrowers who own their homes and have a track record of timely payments. Solar ABS investors are also typically protected by overcollateralization, subordination, and excess spreads. Collectively, these features reduce the default risk in these securitizations even further.

Many solar ABS contain a pre-funding period, which allows the trust to acquire additional qualifying transactions, during a certain period of time after the close of the initial transaction.

Collateralized Debt Obligations

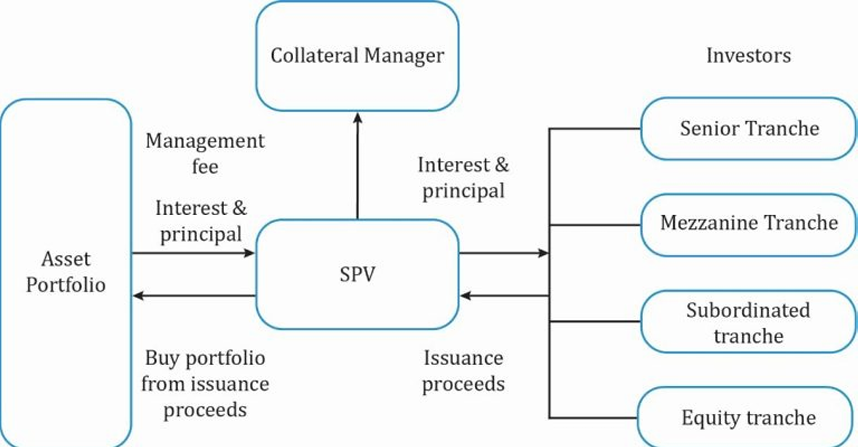

A collateralized debt obligation is a generic term used to describe a security backed by a diversified pool of one or more debt obligations (e.g., corporate and emerging market bonds, leveraged bank loans, ABS, RMBS, CMBS, or CDO).

Like an ABS, a CDO involves the creation of a SPV. But, in contrast to an ABS, where the funds necessary to pay the bond classes come from a pool of loans that must be serviced, a CDO requires a collateral manager to buy and sell debt obligations, for and from the CDO’s portfolio of assets, to generate sufficient cash flows to meet the obligations of the CDO bondholders, and to generate a fair return for the equity holders.

The structure of a CDO includes senior, mezzanine, and subordinated/equity bond classes.

Generic CDO Structure

- The CDO raises funds by issuing debt. The debt obligations are structured as bond classes or tranches, such as senior, mezzanine, or subordinated classes with varying risk and return expectations. Investors invest in a particular bond class based on their risk appetite.

- The funds raised from the issuance of bonds are used by the collateral manager to invest in assets. He seeks to earn a higher return from these assets than what is paid to the bondholders.

- The excess spread is used to pay the equity holders and the CDO manager.

The sources of cash flow to bondholders include interest, principal repayments, and sale of collateral assets.

The most common types of CDOs are:

- Cash flow CDOs, where the cash flows from interest payments and principal repayments are redistributed across the tranches.

- Market value CDOs, where the value accruing to the tranches depends on the market value of the portfolio.

- Synthetic CDOs, where the collateral pool is created synthetically through credit derivatives.

CDOs: Risks and Motivations

In the case of defaults in the collateral, there is a risk that the manager will fail to earn a return sufficient to pay off the investors in the senior and mezzanine tranches. Investors in the subordinated/equity tranche risk the loss of their entire investment.