Long Term Labilities and Equity

Go to Financial Statement Analysis

Topics

Table of Contents

Introduction

- Financial reporting of leases from the perspective of lessors and lessees

- Financial reporting of defined contribution, defined benefit, and stock-based compensation plans

- Presentation and disclosures relating to long-term liabilities and share-based compensation

Leases

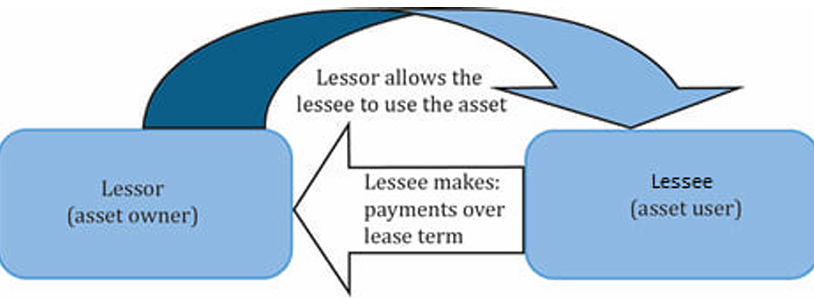

A lease is a contract in which a lessor grants the lessee the exclusive right to use a specific underlying asset for a period of time in exchange for payments.

- An asset’s owner is called a lessor.

- The entity or person wishing to use the asset is called the lessee.

- The lessor allows the lessee to use the asset for a pre-determined period.

- In return, the lessee makes periodic payments to the lessor over the period for the right to use the asset.

Advantages of Leasing

Following are some of the advantages to leasing an asset compared to purchasing it.

- Less cash is needed upfront. Leases typically require little to no down payment.

- Since leases are a form of secured borrowing, they generally have low interest rates.

- Lower risks associated with ownership such as obsolescence.

Lease Classification as Finance or Operating

A finance lease is similar to purchasing an asset while an operating lease is similar to renting an asset.

A lease is classified as a finance lease if any of the following five criteria are met.

- The lease transfers ownership of the underlying asset to the lessee.

- The lessee has an option to purchase the underlying asset and is reasonably certain it will do so.

- The lease term is for a major part of the asset’s useful life.

- The present value of the sum of the lease payments equals or exceeds substantially all of the fair value of the asset.

- The underlying asset has no alternative use to the lessor.

If none of the criteria are met, then the lease is classified as an operating lease.

Financial Reporting of Leases

The financial reporting of leases depends on:

- Whether the party is the lessee or lessor

- Whether the party reports with IFRS or US GAAP

- Whether the lease is a finance or operating

US GAAP and IFRS share the same accounting treatment for lessors but differ for lessees.

IFRS has a single accounting model for both operating leases and finance lease lessees, while US GAAP has different accounting models for each.

Lessee Accounting—IFRS

Under IFRS, there is a single accounting model for both finance and operating leases for lessees.

- At inception, recognize a lease liability and corresponding right-of-use (ROU) asset on the balance sheet, both equal to the present value of lease payments.

- The lease liability is subsequently reduced by each lease payment using the effective interest method. Each lease payment is composed of:

- Interest Expense = Lease Liability x Discount Rate

- Principal Repayment = Lease Payment – Interest Expense

- The right-of-use asset is amortized, often on a straight-line basis, over the lease term.

Although the lease liability and ROU begin with the same carrying value, their balance sheet values tend to diverge over time because of the differences in the calculation of principal repayments that reduces the lease liability and the amortization expense that reduces the ROU asset.

The following list shows how the lease transaction affects the financial statements.

- Balance sheet: The lease liability is reported net of principal repayments and the ROU asset is reported net of accumulated amortization.

- Income statement: Interest expense and amortization expense are shown separately.

- Cash flow statement: The principal repayment component is reported as cash outflow under financing activities. The interest expense can be reported under either operating or financing activities.

A company is offered the following terms to lease a machine: five-year lease with an implied interest rate of 10% and an annual lease payment of EUR 100,000 per year payable at the end of each year. PV = EUR 379,079. The asset will be amortized over the five-year lease term on a straight-line basis. The company reports under IFRS.

What would be the impact of this lease on the company’s:

- Balance sheet at the beginning of the year?

- Income statement during the following year?

- Statement of cash flows during the following year?

Solution

| | Lease Payment | Interest Expense | Principal Repayment | Lease Liability | Amortization Expense | ROU Asset |

| --- | ------------- | ---------------- | ------------------- | --------------- | -------------------- | --------- |

| Y0 | | | | 379,079 | | 379,079 |

| Y1 | 100,000 | 37,908 | 62,092 | 316,987 | 75,816 | 303,263 |

| Y2 | 100,000 | 31,699 | 68,301 | 248,685 | 75,816 | 227,447 |

| Y3 | 100,000 | 24,869 | 75,131 | 173,554 | 75,816 | 151,631 |

| Y4 | 100,000 | 17,355 | 82,645 | 90,909 | 75,816 | 75,816 |

| Y5 | 100,000 | 9,091 | 90,909 | 0 | 75,816 | 0 |

| | 500,000 | 120,921 | 379,079 | | 379,079 | |

- Report a lease liability and a ROU asset of EUR 379,079.

- In Year 2, the company will report an interest expense of EUR 31,699 and an amortization expense of EUR 75,816.

- In Year 2, principal repayment of EUR 68,301 will be reported as a cash outflow under financing activities. The interest expense of EUR 31,699 may be reported under operating or financing activities depending on the company’s reporting policies.

Lessee Accounting—US GAAP

Under US GAAP, there are two accounting models for lessees: one for finance leases and another for operating leases.

The finance lease accounting model is the same as the lease accounting model for IFRS.

The operating lease accounting model is different:

- At inception, recognize a lease liability and corresponding right-of-use asset on the balance sheet, both equal to the present value of lease payments.

- As with the previous method, the lease liability is subsequently reduced by each lease payment using the effective interest method.

- But the amortization of the right-of-use asset is different, it is calculated as the lease payment less the interest expense.

Since the principal repayment and amortization are calculated in the same way, the lease liability and the ROU asset will always equal each other.

The following list shows how the lease transaction affects the financial statements.

- Balance sheet: The lease liability is reported net of principal repayments and the ROU asset is reported net of accumulated amortization

- Income statement: Interest expense and amortization expense are shown together as a single operating expense on the income statement. They are not reported separately.

- Cash flow statement: The entire lease payment is reported as cash outflow under operating activities. The interest and principal components are not reported separately.

For a US GAAP company classifying a lease as an operating lease instead of a finance lease affects the financial ratios as shown below:

| Ratio | Formula | Impact |

|---|---|---|

| EBITDA Margin | Lower: Lease expense is classified as an operating expense rather than interest and amortization. | |

| Asset Turnover | Lower: Total assets are higher under an operating lease because the ROU asset is amortized at a slower pace in initial years. | |

| Cash Flow Per Share | Lower: Cash flow from operations is lower because the entire lease payment is included in operating activities versus solely interest expense for a finance lease. |

Lessor Accounting

The accounting for lessors is identical under IFRS and US GAAP. However, the accounting differs based on whether the lease is a finance lease or an operating lease.

==Finance lease lessors (IFRS and US GAAP) ==

- At inception, recognize a lease receivable asset equal to the present value of future lease payments and de-recognize the leased asset, simultaneously recognizing any difference as a gain or loss.

- The lease receivable is subsequently reduced by each lease payment using the effective interest method.

The following list shows how the lease transaction affects the financial statements.

- Balance sheet: Lease receivable net of principal proceeds is reported on the balance sheet.

- Income statement: Interest income is reported on the income statement, typically as revenue.

- Cash flow statement: The entire cash receipt is reported under operating activities.

Operating lease lessors (IFRS and US GAAP)

The lease contract is treated as a rental agreement.

The following list shows how the lease transaction affects the financial statements.

- Balance sheet: The balance sheet is not affected. The lessor continues to recognize the underlying asset and depreciate it.

- Income statement: Lease revenue is recognized on a straight-line basis on the income statement. The depreciation expense continues to be recognized.

- Cash flow statement: The entire cash receipt is reported under operating activities.

Assume that the carrying value of the asset immediately prior to the lease is EUR 350,000, accumulated depreciation is zero, and the lessor elects to depreciate it on a straight-line basis over five years. How would the lessor’s financial statements be affected by the classification of the lease as a finance or operating lease?

| (B) F Net Lease Receivable |

(B) O Net PPE |

(I) F Interest Revenue |

(I) O Lease Revenue |

(C) F | (C) O | |

|---|---|---|---|---|---|---|

| Year 1 | 316,987 | 280,000 | 37,908 | 100,000 | 100,000 | 100,000 |

| Year 2 | 248,685 | 210,000 | 31,699 | 100,000 | 100,000 | 100,000 |

| Year 3 | 173,554 | 140,000 | 24,869 | 100,000 | 100,000 | 100,000 |

| Year 4 | 90,909 | 70,000 | 17,355 | 100,000 | 100,000 | 100,000 |

| Year 5 | 0 | 0 | 9,091 | 100,000 | 100,000 | 100,000 |

- Balance Sheet: The present value of lease payments is well above the carrying value of the asset. The finance lease classification therefore results in a significant increase in assets.

Financial Reporting for Postemployment and Share-Based Compensation Plans

Employee Compensation

Employee compensation packages are designed to achieve a variety of goals, including meeting employees’ liquidity needs, retaining employees, and motivating employees.

Common components of employee compensation are:

- Salary: Provides for the liquidity needs of an employee.

- Bonuses: Generally provided in the form of cash. They can motivate and reward employees for short-or-long term performance.

- Non-monetary benefits such as health and life insurance premiums: Provided to facilitate employees performing their jobs.

- Defined contribution/benefit pension plan: Provides cash flow to employees in retirement.

- Share-based compensation: Aligns employee’s interest with those of shareholders.

Pension Plans

One common post-employment benefit offered by companies to their employees is pension. Pensions and other post-employment benefits give rise to non-current liabilities reported by many companies. When companies promise its employees certain benefits after a certain period of time, they are obligated to fulfill that promise.

The accounting treatment of pensions depends on the type of pension plan. There are primarily two types of pension plans:

- Defined contribution plan: Under this plan, a company contributes an agreed-upon amount to the plan. This contribution is recognized as a pension expense on the income statement and an operating cash outflow.

- Since there is no future payout or obligation, no liability is reported on the balance sheet.

- A liability is recognized on the balance sheet if some prior agreed-upon amount is not paid by the end of the fiscal year.

- Defined benefit plan: Under this plan, a company promises to pay a certain amount in the future to the employees. The amount of future obligation is based on a lot of assumptions such as retirement age of its employees, last drawn salary before retirement, mortality rate, etc.

- The pension obligation is the present value of future payments the company expects to make.

- A company fulfills this obligation by setting up a pension fund (also known as plan assets) and making payments to this fund.

- The ongoing pension obligations are paid from this fund.

- The amount in the fund remains invested until it has to be paid to the retirees.

Accounting for Defined-Benefit Plans

Since the future obligation of defined benefit pension fund cannot be determined with certainty, accounting is more complicated than the defined contribution plan. Listed below are a few rules for you to remember for a defined benefit plan:

- If the fair value of plan assets > present value of estimated pension obligation, the plan is overfunded (has a surplus). It is called net pension asset.

- If the present value of estimated pension obligation > fair value of plan assets, the plan is underfunded. It is called net pension liability.

Under both IFRS and US GAAP, the net pension asset or liability is reported on the balance sheet.

An underfunded defined benefit pension plan is reported as a non-current liability on the balance sheet.

For each period, the change in net pension asset or liability is recognized either in profit or loss or in other comprehensive income.

IFRS, has three components:

- Employee service costs and past service costs: Recognized as pension expense in the income statement.

- Service cost is the present value of the benefit earned by an employee for one additional year of service. It is the sum of past service costs and present value of the increase in pension benefit earned by working for one more year.

- Income accrued on the beginning of net pension liability represents the change in value of the net defined benefit pension liability.

- Recognized as pension expense in the income statement.

- Used to estimate the present value of the pension obligation.

- Net Interest Expense = Net Pension Liability

Discount Rate

- Re-measurements: Recognized in other comprehensive income on the balance sheet.

- Remeasurements = Actuarial Gains and Losses and the Actual Return on Plan Assets - Net Interest Expense.

The actual return on plan assets includes interest, dividends and other income derived from the plan assets, including realized and unrealized gains or losses.

US GAAP, has five components:

- Employees’ service costs for the period.

- Interest expense accrued on the beginning pension obligation.

- Expected return on plan assets. It is a reduction in the amount of expense recognized.

- Past service costs.

- Actuarial gains or losses.

The first three are recognized in profit and loss during the period incurred. Past service costs and actuarial gains and losses are recognized in other comprehensive income in the period they occur and later amortized into pension expense. Under US GAAP, companies are also allowed to immediately recognize actuarial gains and losses in profit and loss.

Share-Based Compensation

Share-based compensation is intended to align incentives of management and owners. From an accounting perspective, share-based compensation is treated as an expense even though no cash changes hands when stock options/grants are issued. Both IFRS and US GAAP require us to come up with a fair value to measure the share-based compensation. Also, the nature and extent of share-based compensation and its effect on financial statements need to be disclosed.

There are several disadvantages of share-based compensation:

- Employees may have limited influence over the company’s market value. Hence, it does not necessarily provide the desired incentives.

- Increased ownership may lead managers to be more risk averse or less risk averse than they should be, depending on whether the current stock price is above or below the exercise price of the stock options.

- When shares are granted to employees, the existing shareholder’s ownership is diluted.

Stock Grants

- Compensation expense is reported on the basis of fair value of the stock on the grant date.

- Compensation expense is allocated over the service period.

There are three types of stock grants:

Outright Grants

Restricted Grants

- Shares have to be returned if certain conditions not met. Conditions might include staying with the company for a specified period, or meeting certain performance goals.

Performance Shares

- Determined by performance measures other than change in share price. For example, accounting earnings or return on assets.

- It addresses employees’ concern that share price is beyond their control and should not be used for assessment.

Stock Options

Like stock grants, compensation expense related to stock options is reported at fair value. The fair value has to be estimated using an appropriate valuation model. Commonly used models are the Black–Scholes option pricing model and the binomial model. The value of a stock option is sensitive to model inputs and assumptions.

| Assumption | Impact on Option Value if Increase in Assumption |

|---|---|

| Exercise Price | Lower |

| Stock Price Volatility | Higher |

| Estimated Life of Each Award | Higher |

| Estimated Dividend Yield | Lower |

| Risk Free Rate | Higher |

| In accounting for stock options, there are several important dates, including the grant date, the vesting date, the exercise date, and the expiration date. |

- Grant date is the day that options are granted to employees.

- Vesting date is the date that employees can first exercise the stock options.

- Exercise date is the date when employees actually exercise the options and convert them to stock.

If the options go unexercised, they may expire at some pre-determined future date, commonly 5 or 10 years from the grant date. The compensation expense is allocated over the service period.

A company awards 1,000,000 stock options to its executives on 1 July 2015. The estimated cost of each option is $0.50. The options require a service period of 4 years after the grant date before vesting. What is the stock option expense for 2015?

The expense for the year = 1,000,000 x $0.50/4 x ½ = $62,500

We divide by 4 because the options have a service period of 4 years. Since the options are granted in the middle of 2015, we multiply by ½ to allocate the expense to the second half of 2015.

Other Types of Share-Based Compensation

Both stock grants and stock options have the potential to dilute EPS. To avoid this, options such as Stock Appreciation Rights (SARs) are available. They compensate an employee on the basis of changes in the value of shares without requiring the employee to hold the shares. Like other forms of share-based compensation, SARs align employee’s interests with shareholders.

They have the following additional advantages:

- The potential for risk aversion is limited because employees have limited downside risk and unlimited upside potential similar to employee stock options

- Shareholder ownership is not diluted.

A disadvantage is that SARs require a current-period cash outflow. Similar to other share-based compensation, SARs are valued at fair value and compensation expense is allocated over the service period of the employee.

Presentation and Disclosure

Presentation and Disclosure of Leases

The objective of lease disclosure is to provide the user of financial statements with information to assess the amount, timing and uncertainty of cash flows associated with leases.

The non-current portion of the balance sheet will typically contain a “right of use” asset and the non-current liabilities section will typically show the lease liability.

Lessee Disclosure

Lessee disclosures should include the following:

- Carrying amount of right of use assets and the end of the reporting period by class of underlying asset

- Total cash outflow for leases

- Interest expense on lease liabilities

- Depreciation charges for right-of-use assets by class of underlying asset

- Additions to right of use assets

In addition, lessees should disclose a maturity analysis of lease liabilities and additional quantitative and qualitative information about leasing activity.

Lessor Disclosure

At a minimum, lessors should disclose:

- Finance Leases

- Amount of selling profit or loss

- Finance income on the net investment in the lease

- Income relating to variable lease payments not included in the measurement of the lease

- Operating Leases

- Lease income with separate disclosure for income relating to variable lease payments based on an index or rate.

Presentation and Disclosure of Postemployment Plans

Companies are required to make disclosures such as:

- Nature of benefits provided, the regulatory framework in which the plan operates, governance of the plan, and risks to which the plan exposes the entity

- Reconciliation from the opening balance to the closing balance of the net pension asset or liability, with separate reconciliations for plan assets and the present value of the defined benefit obligation, showing service costs, interest income or expense, remeasurements, past service costs, contributions to the plan, and other components of the change

- Sensitivity analysis showing how changes in significant assumptions (such as the discount rate used to measure the defined benefit pension obligation) would affect the amounts reported on the financial statements

- Composition of plan assets by category, such as equity securities, fixed-income securities, and real estate

- Indications of the effect of the defined benefit pension plans on the entity’s future cash flows

Presentation and Disclosure of Share-Based Compensation

Companies are required to make disclosures such as:

- Description of each type of share-based payment arrangement, including its general terms and conditions, such as vesting requirements, the maximum term of options granted and the method of settlement (i.e., cash or equity)

- Details about the number and weighted average exercises price of options, including:

- Number outstanding at the beginning of the period

- Granted during the period

- Forfeited during the period

- Exercised during the period

- Expired during the period

- Outstanding at the end of the period

- Exercisable at the end of the period.

- For other equity instruments granted during the period (i.e., other than share options), the number and weighted average fair value of those equity instruments at the measurement date, and information on how that fair value was measured.