Intro to FSA

Go to Financial Statement Analysis

Topics

Table of Contents

Introduction

Financial analysis is the process of examining a company’s performance.

For this purpose, financial reports are one of the most important sources of information available to a financial analyst. A financial analyst must have a strong understanding of the information provided in a company’s financial reports, notes, and supplementary information.

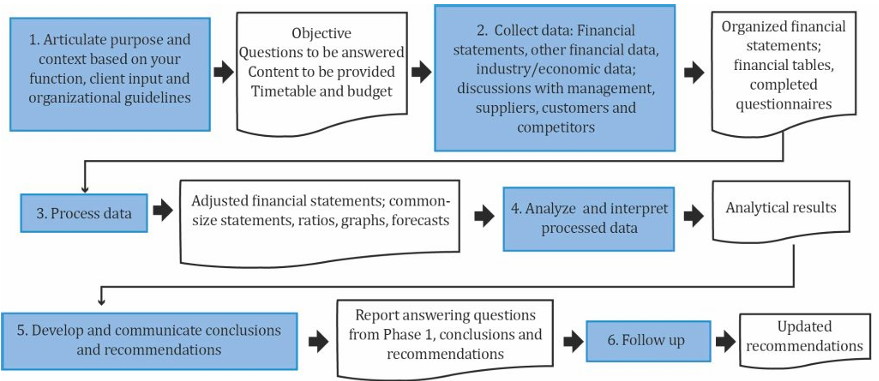

Financial Statement Analysis Framework

A generic financial statement analysis framework is summarized in the figure below. The grey boxes represent phases of financial analysis while the white boxes represent outputs from each phase.

Articulate the Purpose and Context of Analysis

In this step, we understand the purpose of the analysis.

- An equity analyst analyzes the financial reports in order to decide whether to invest in the stocks of the company or not.

- A credit analyst looks at the company in a very different light in order to judge whether it should be given a loan or not.

Next, the analyst defines the context which includes details such as the intended audience, time frame, budget, and so on. Once the purpose and the context are defined, the analyst compiles the specific questions to be answered by the analysis, decides on the content to be prepared, and finalizes the timeline and the budget.

Collect Data

Next, the analyst collects data required to answer the questions compiled in the previous step. The sources of data are financial reports and other information sources.

The output from this step includes organized financial statements, financial tables, and completed questionnaires.

Process Data

After collecting data, the analyst processes the data using appropriate analytical tools.

This involves:

- Making any adjustments to the financial statements to facilitate comparison. For example, adjustments will be required to compare a company using IFRS with a company using US GAAP.

- Creating graphs, ratios, common-size statements, etc.

The output from this step includes adjusted financial statements, common-size statements, ratios, graphs, and forecasts.

Analyze/Interpret the Processed Data

The next step is to interpret the processed data and come up with a decision.

An equity analyst may come up with a buy, sell, or hold decision.

Develop and Communicate Conclusions/Recommendations

Next, the analyst communicates the conclusions or recommendations in the appropriate format.

An equity analyst will prepare a research report and send it to his firm’s clients.

Follow-up

Conduct periodic reviews to check if the previous conclusions are still valid. Change the conclusions/recommendations when necessary.

An equity analyst may send quarterly updates on his initial buy, sell, or hold recommendation.

Scope of Financial Statement Analysis

In order to understand financial analysis, we first need to understand the difference between the roles of financial reporting and financial statement analysis.

Financial Reporting

The role of financial reporting is to provide information about a

- company’s performance (income statement and cash flow statement)

- financial position (balance sheet)

- changes in financial position (statement of changes in equity)

Financial Statement Analysis

The role of financial statement analysis is to use the financial reports prepared by firms and combine them with other sources of information to decide if you can invest in the equity of the firm or lend money to the firm.

Regulated Sources of Information

Standard-Setting Bodies

Standard-setting bodies are private sector organizations that help develop financial reporting standards.

The two important standard-setting bodies are:

- ==Financial Accounting Standards Board (FASB) ==– For the US. The standards developed by FASB are called US GAAP (Generally Accepted Accounting Principles).

- International Accounting Standards Board (IASB) – For the rest of the world. The standards developed by IASB are called IFRS (International Financial Reporting Standards).

Standard-setting bodies simply set the standards but they do not have the authority to enforce the standards.

Regulatory Authorities

Regulatory authorities are government entities that have legal authority to enforce the financial reporting standards. For example: Securities and Exchange Commission (SEC) – for the U.S.

Regulatory authorities are also responsible for the regulation of capital markets under their jurisdiction.

The International Organization of Securities Commissions (IOSCO)

Technically not being a regulatory authority, IOSCO still regulates a significant portion of the world’s financial markets. (Think of it as an umbrella organization of regulatory authorities). This organization has established objectives and principles to guide securities and capital market regulation.

Core Objectives

- Protect investors.

- Ensure fairness, efficiency, and transparency in markets.

- Reduce systemic risk.

Principles

- There should be full, accurate, and timely disclosure of financial results and risks.

- Financial statements should be of a high and internationally acceptable quality.

Primary Financial Statements

The curriculum presents this information in terms of SEC filings – e.g. Forms 10-K, 20-F, DEF-14A, 10-Q etc. You are not expected to memorize these forms. Also, exam questions are unlikely to test country-specific regulations. For these reasons, we have simplified the explanation in this section for better comprehension.

The primary financial statements are the balance sheet, the income statement, the cash flow statement, and the statement of changes in owners’ equity.

Balance Sheet

The balance sheet reports the firm’s financial position at a specific point in time.

It has the following elements:

- Assets – What the company owns.

- Liabilities – What the company owes.

- Owners’ equity – What the shareholders of the company own. Depending on the form of the organization, owners’ equity may be referred to as

- partners’ capital

- shareholders’ equity

- shareholders’ funds

- net assets

The relationship between the elements can be shown as: $$\text{Assets = Liabilities + Owners’ equity}$$The capital structure of a company represents the combination of liabilities and equity used to finance its assets. Both financial position and capital structure are useful in credit analysis.

Income Statement

The income statement reports the financial performance of the firm over a period of time.

It has the following elements:

- Revenues – Income generated by selling goods and services.

- Expenses – Costs incurred for producing goods and services.

- Net income – Resulting profit or loss.

The relationship between the elements can be shown as: $$\text{Net income = Revenues – Expenses}$$

Cash Flow Statement

The cash flow statement reports the sources and uses of cash for the firm over a period of time.

It has the following elements:

- Operating cash flows – Cash flows from day-to-day activities.

- Investing cash flows – Cash flows associated with the acquisition and disposal of long-term assets, such as property and equipment.

- Financing cash flows – Cash flows from activities related to obtaining or repaying capital.

Statement of Changes in Owner’s Equity

It reports the changes in the owners’ investment in the firm over time.

It has the following elements:

- Paid in capital – Amount raised from owners.

- Retained earnings – Firm’s profits that have been retained (i.e., not paid out as dividends).

Along with these required financial statements (mentioned above), a company typically provides additional information in its financial reports.

This includes footnotes, management’s commentary, and auditor’s report.

Footnotes

They provide additional details about the information presented in financial statements.

This includes important information about the accounting methods, estimates, and assumptions. They also contain information regarding acquisitions and disposals, commitments and contingencies, legal proceedings, employee stock options and other benefits, related party transactions and business, and geographic segments.

Management Discussion and Analysis (MD&A)

It provides an assessment of the data reported in the financial statements from the management’s perspective.

Examples of content include trends and significant events affecting the company’s operations, liquidity and capital resources, off-balance sheet obligations, and planned capital expenditures.

Auditor’s Report

An audit is an independent review of a firm’s financial statements. It enables the auditor to express an opinion on the fairness and reliability of the financial reports.

An audit report can contain one of the following opinions:

- Unqualified Opinion – Reasonable assurance that financial statements are fairly presented. This is also referred to as an “unmodified” or a “clean” opinion. (This is the opinion that you would like to see.)

- Qualified Opinion – Some misstatement or exception to accounting standards.

- Adverse Opinion – Financial statements materially depart from accounting standards and are not presented fairly.

If the auditor is not able to issue an opinion for reasons such as a scope limitation, a disclaimer of opinion is issued.

For listed companies, the audit report also includes a discussion of Key Audit Matters (international) and Critical Audit Matters (US). Key Audit Matters and Critical Audit Matters include issues having a higher risk of misstatement, involving significant management judgment and estimates.

Other Sources

- Interim reports – Quarterly or semiannual reports prepared by the firm. These reports are not audited.

- Proxy statements – Statements distributed to shareholders about matters that are to be put to a vote, e.g. management and director compensation.

Comparison of IFRS with Alternative Financial Reporting Systems

A significant percentage of listed companies use either IFRS or US GAAP. An analyst must be cautious when comparing financial measures between companies reporting under IFRS and companies reporting under US GAAP. If needed, specific adjustments need to be made to achieve comparability.

US GAAP uses standards issued by FASB while IFRS uses standards issued by IASB. While the two organizations are working towards convergence, significant differences still remain.

| US GAAP | IFRS | |

|---|---|---|

| Developed by | Financial Accounting Standards Board (FASB) | International Accounting Standards Board (IASB) |

| Based on | Rules | Principles |

| Interest paid | Cash Flows from Operating activities | Cash Flows from Financing or Operating activities |

| Inventory valuation | FIFO; LIFO and Weighted Average Method | FIFO and Weighted Average Method |

| Development cost | Treated as an expense | Capitalized, in specific conditions |

| Reversal of inventory write-down | Prohibited | Permissible, in specific conditions |

Monitoring Developments in Financial Reporting Standards

Analysts must be aware that reporting standards are evolving rapidly. They need to monitor developments in financial reporting and assess their implications for security analysis and valuation.

A financial analyst can remain aware of developments in financial reporting standards by monitoring three sources:

- new products or transactions

- actions of standard setters and groups representing users of financial statements

- company’s disclosures regarding critical accounting policies and estimates.

New Products or Types of Transactions

New products or transactions can emerge as a result of economic events such as new businesses (e.g. fintech) or a newly developed financial instrument (e.g. crypto currencies). Analysts should investigate whether these products or transactions were created for the purpose of ‘window dressing’ financial reports.

If needed, an analyst can obtain additional information from the company’s management, which should be able to describe the economic purpose, financial statement reporting, significant estimates, judgments used in determining the reporting, and future cash flow implications for these items.

Evolving Standards and the Role of CFA Institute

The IASB and FASB both provide extensive information on their websites about new standards and proposed changes to the standards. Furthermore, both bodies seek feedback from the financial analyst community on how the standards can be improved further.

CFA Institute actively works in supporting improvements to financial reporting. CFA Institute volunteers serve on several liaison committees that meet on a regular basis to make recommendations to the IASB and FASB.

Other Sources of Information

In addition to the information required by regulatory authorities, analysts can also obtain information from the following sources.

- Issuer sources (other than regulatory filings such as annual and quarterly reports and proxy statements)

- Earnings call

- Presentations and events, such as investor days

- Press releases

- Discussion with management, investor relations, or other company personnel

- Company website

- Public third-party sources

- Free industry whitepapers or analyst reports from a consultancy

- Economic or industry indicators from governments and other organizations, Eg. retail sales and price indexes

- General news outlets

- Industry-specific news outlets

- Social media

- Proprietary third-party sources

- Analyst reports and communications

- Reports and data from platforms such as Bloomberg

- Reports and data from consultancies such as Rystad for the energy industry

- Proprietary primary research

- Surveys, conversations, product comparisons, and other studies commissioned by the analyst or conducted directly.