Working Capital and Liquidity

Go to Corporate Issuers

Topics

Table of Contents

Introduction

- Cash conversion cycle

- Primary and secondary sources of liquidity; evaluating a company’s liquidity position

- Working capital approaches and their impact on the funding needs of a company

Cash Conversion Cycle

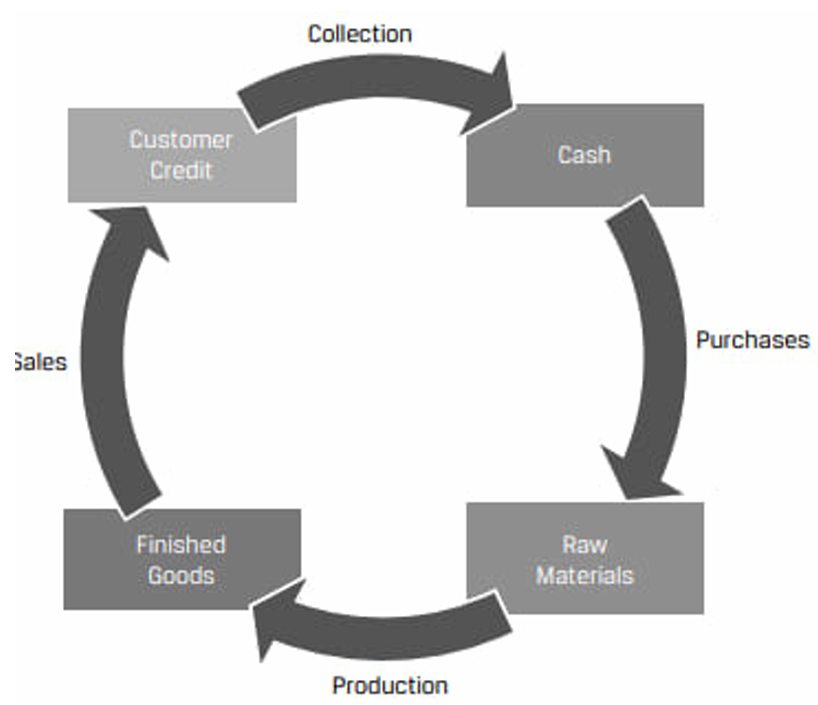

The business operations of a company are typically made up of several sequential steps such as: acquiring raw materials, producing inventory, selling products to customers, and collecting cash. These activities are known as the issuer’s operating cycle, and they can occur once or several times per year.

These activities generate cash outflows and inflows that do not always occur at the same time as the activity. For example, raw materials may be purchased on credit and a payment made to the vendor later. Finished goods can be sold and delivered to customers but payment collected later. Inventory may take time to produce and be ready for sale.

Future cash inflows from operating activities are recorded as short-term assets, while future cash outflows are recorded as short-term liabilities.

| Short Term | Meaning | Recognized when | Derecognized when | |

|---|---|---|---|---|

| Accounts receivable | Asset | Amounts to be collected from customers for products or services sold | Product or service is sold to customer on credit | Cash is received from customer |

| Inventory | Asset | Cost of products produced or purchased for sale | Issuer takes ownership of materials, goods, supplies, etc. | Product is sold to customer |

| Accounts payable | Liability | Amounts owed to suppliers for products or services received | Product or service is received, and issuer defers payment to supplier | Cash is paid to supplier |

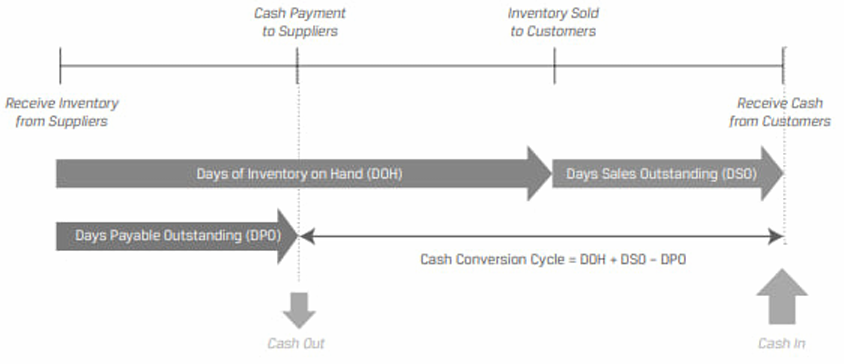

| The amounts of time that accounts payable, inventory, and accounts receivable are outstanding on the balance sheet are known, respectively, as days payable outstanding (DPO), days of inventory on hand (DOH), and days sales outstanding (DSO). |

Cash Conversion Cycle

A company’s cash conversion cycle is the amount of time between an issuer paying its suppliers and receiving cash from customers. (i.e., the time between derecognition of accounts payable and derecognition of accounts receivable)

Cash conversion cycle = Days of inventory on hand + Days sales outstanding – Days payable outstanding.

Generally, the shorter the cycle the better. A short cash conversion cycle means that a company converts its inventory investment into cash quickly, whereas a long cash conversion cycle means that a company converts its inventory investment into cash slowly. The longer the cycle the higher the amount of working capital a company will need.

Some companies can also have a negative cash conversion cycle – they receive cash from customers well before suppliers are paid.

Companies can shorten their cash conversion cycle in several ways:

- Reduce days on inventory on hand by

- discounting products with low demand, using a

just in timeinventory system, using data analytics to improve demand forecasts.

- discounting products with low demand, using a

- Reduce days sales outstanding by

- offering prompt-payment discounts to customers, imposing late fees, working with third-party collection agencies.

- Increase days payable outstanding by

- negotiating longer payment terms with suppliers.

However, the ability to negotiate better terms is highly dependent on the power dynamics between the company and its supplier. A small company purchasing a specialized critical component from a sole supplier, may not have the ability to negotiate better terms.

Suppliers usually offer discounts for prompt payments. For example, the terms may be: 2/10 net 30, which means if the payment is made within 10 days, the company will get a 2 percent discount else the entire payment must be made within 30 days.

In such cases the company should compare the cost of trade credit with its other short-term borrowing costs to make a decision on whether to take the discount.

Cost of trade credit =

where:

- n = 365 / number of days beyond discount period

A company is evaluating two options to fund its working capital needs:

- Option 1: Forgo the 2% discount offered by its supplier. The standard trade terms are 2/10 net 30.

- Option 2: Borrow through its external line of credit. The effective annual rate for the line of credit is 7.7%.

Which option should the company prefer?

The effective annual rate on the forgone trade credit can be calculated as:

This is significantly higher than the 7.7% rate on the external credit line. Therefore, the company should prefer the credit line. It should borrow from the credit line and pay the supplier early to avail the discount.

Apart from the cash conversion cycle, analysts also assess the amount of working capital used by a company.

- Total working capital = Current assets – Current Liabilities

- Net working capital = Current assets, excluding cash and marketable securities – Current liabilities, excluding short-term and current debt.

To compare across firms, total or net working capital is often expressed as a percentage of sales. The lower this ratio, the better.

| Cash | 100 | 1 |

| Marketable Securities | 20 | 2 |

| Acc Receivables | 600 | 3 |

| Inventory | 800 | 4 |

| Prepaid Expenses | 30 | 5 |

| PPE | 10000 | 6 |

| Intangibles | 500 | 7 |

| Total Assets | 12050 | 8 |

| Acc Payable | 980 | 9 |

| Accrued Expenses | 70 | 10 |

| Short Term Debt | 1000 | 11 |

| Long Term Debt | 2000 | 12 |

| Shareholder's Equity | 8000 | 13 |

| Total Liabilities and Equity | 12050 | 14 |

| Current Assets → 3, 4, 5 | ||

| Current Liabilities → 9, 10 | ||

| Net Working Capital = 380 |

Liquidity

‘Liquidity’ is the extent to which a company is able to meet its short-term obligations using cash flows and those assets that can be readily transformed into cash.

The liquidity of an asset can be evaluated along two dimensions:

- The type of the asset

- The speed at which the asset can be converted into cash (by sale or financing)

‘Liquidity management’ refers to the company’s ability to generate cash when needed, at the lowest possible cost.

Two sources of liquidity for a company are:

- primary sources of liquidity, such as cash balances

- secondary sources of liquidity, such as selling assets

The main difference between the two is that using primary sources has no effect on a company’s ongoing operations, whereas using secondary sources may have a negative impact on a company’s ongoing operations.

Primary Liquidity Sources

They represent the most readily accessible resources available to the company.

Primary sources include:

- Free cash flow: The firm’s after-tax operating cash flow less planned short- and long-term investments.

- Cash and marketable securities on hand: Cash available in bank accounts or held as marketable securities that can be sold quickly without loss of value.

- Borrowings from banks, bondholders, or supplier’s trade credit. This option settles the current obligation but creates a new obligation that has to be repaid in future.

Secondary Liquidity Sources

Secondary sources include:

- Suspending or reducing dividend payments

- Delaying or reducing capital expenditures

- Issuing additional equity

- Renegotiating debt contracts

- Selling assets

- Filing for bankruptcy protection and reorganization

Factors Affecting Liquidity: Drags and Pulls

A company’s liquidity position is affected by cash receipts and the amount of cash it has to pay.

- ‘Drags on liquidity’ reduce cash inflows.

- For example, uncollected receivables, obsolete inventory, tight credit etc.

- ‘Pulls on liquidity’ accelerate cash outflows.

- For example, earlier payment of vendor dues, reduced credit limits (by suppliers), limits on short-term lines of credit (by banks) etc.

Measuring and Evaluating Liquidity

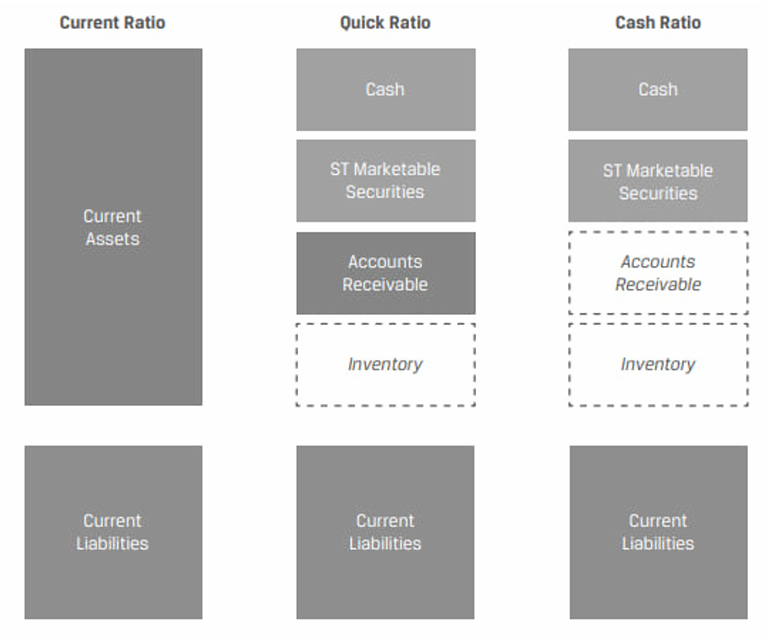

Liquidity ratios are used to measure a company’s ability to meet its short-term obligations.

- A higher number implies greater liquidity.

- Cash ratio is the most conservative liquidity ratio and a good measure of a company’s ability to handle a crisis situation.

- The levels of these ratios, and their trends, or changes over time, in addition to comparisons with competitors or the industry, are used to judge a firm’s liquidity position.

Managing Working Capital and Liquidity

Working Capital Management

To determine their required working capital investment, companies first identify their optimal levels of inventory, receivables and payables as a function of sales. They then project these assumptions forward into the future.

After determining its working capital requirements, a firm then identifies the optimal mix of short-and long-term financing necessary to fund these requirements.

Companies may take different approaches to working capital management:

- Conservative approach: In a conservative approach, the firm holds a larger position in current assets (cash, receivables, and inventories). This provides financial flexibility to respond to unforeseen events, but it results in a lower return on equity. The firm finances a majority of its current assets (both permanent and variable) with long-term debt or equity financing.

- Aggressive approach: In an aggressive approach, the firm holds a substantially smaller position in current assets. This reduces financial flexibility, but it results in a higher return on equity. Also, the firm finances a majority of its current assets (both permanent and variable) with short-term debt or payables.

- Moderate approach: In a moderate approach, the firm holds a position in current assets that is somewhere between the two approaches. Also, the firm attempts to match the duration of the current assets with the liabilities. It would finance its permanent current assets with long-term debt and equity; and finance its variable current assets with short-term debt and payables.

Current assets can be divided into permanent current assets and variable current assets.

- Permanent current assets remain relatively constant throughout the year.

- Variable current assets vary based on the seasonality of the business, increasing during peak production periods.

| Pros | Cons | |

|---|---|---|

| Conservative approach | - Stable financing avoids rollover risk associated with short-term debt - Financing costs are known upfront - Certainty of working capital needed to purchase the necessary inventory - Extended payment term reduces short-term cash needs for debt service - Higher flexibility during market disruptions that can be covered by larger cash or marketable securities positions |

- Long-term debt typically involves a higher interest rate - High cost of equity - Permanent financing eliminates the opportunity to borrow only as needed (increasing ongoing financing costs) - A longer lead time is required to establish the financing position - Long-term debt may require more covenants that restrict business operations |

| Aggressive approach | - Short-term lines of credit provide the flexibility to access financing only when needed—particularly appropriate for seasonality—reducing overall interest expense - Short-term loans involve less rigorous credit analysis, as the lender has greater clarity as to the short-term operations of the firm - Flexibility to refinance if rates decline |

- Interest expense may fluctuate as rates on short-term financing change - May result in higher short-term cash needs to satisfy debt maturities - Rollover risk of short-term debt increases bankruptcy risk, particularly during market disruptions - May have to rely on more costly trade credit, tighten customer credit, or sell receivables if unable to refinance at favorable terms |

| Moderate approach | - Lower financing cost versus conservative approach; lower risk than aggressive approach - Flexibility to increase financing for seasonal spikes while maintaining a base level for ongoing needs - Diversifying sources of funding with a more disciplined approach to balance sheet management |

- Access to short-term capital may be limited for seasonal or growth needs - Uncertain cost of short-term debt for variable needs during market disruptions - May have to rely on more costly trade credit to meet seasonal or growth needs if unable to refinance at favorable terms |

Liquidity and Short-Term Funding

Companies seek to implement a short-term financing strategy that will help achieve the following objectives:

- Ensure sufficient capacity to handle peak cash needs.

- Maintain sufficient and diversified sources of credit.

- Ensure rates are cost-effective.

- Ensure both implicit and explicit funding costs are considered.

Factors that will influence a company’s short-term borrowing strategies are:

- Size: Larger companies have additional and cheaper options as compared to smaller companies.

- Creditworthiness: The borrower’s creditworthiness determines the access to and the cost of borrowing.

- Legal and regulatory considerations: Legal and regulatory constraints on specific industries can restrict how much a company can borrow and under what terms.

- Underlying assets: Depending on their business model, some companies may have assets that are considered attractive as collateral for secured loans.