Investors and Other Stakeholders

Go to Corporate Issuers

Topics

Table of Contents

Introduction

- Securities issued by corporations – debt and equity, the differences in their risk-return profiles, and the conflicts of interest between debt and equity.

- The various stakeholders of a company and their interests.

- ESG considerations in investment analysis

Financial Claims of Lenders and Shareholders

Debt Versus Equity

The key differences between debt and equity financing are:

- Debt represents a contractual obligation on the part of the issuing company. The company is obligated to make the promised interest and principal payments to debtholders. Equity does not involve a contractual obligation.

- Debtholders have a prior legal claim on the company’s cash flows and assets. Their claims have to be fully paid before the company can make distributions to equity owners. Equity holders have a residual claim on the company’s net asset after all other stakeholders have been paid.

- Interest payments on debt are typically tax-deductible. Whereas, dividend payments on equity are not tax deductible.

- Equity represents a more permanent source of capital. It has no finite term and includes voting rights. In contrast, debt represents a cheaper source of capital. It has a stated finite term and no voting rights.

Debt Versus Equity: Risk and Return

Investor’s perspective:

From an investor’s perspective, investing in equity is riskier than investing in debt. Debtholders receive predictable coupon payments, whereas payments to shareholders are at the company’s discretion.

However, equity holders do have a residual claim, which means they are entitled to whatever firm value remains after other stakeholders have been paid off, giving them unlimited upside potential. Therefore, equity holders have an interest in the ongoing maximization of company value (net assets less liabilities), which directly corresponds to the value of their shareholder wealth.

On the other hand, no matter how profitable a company becomes, debtholders will never receive more than their interest and principal repayment. Their maximum return is capped. They are therefore interested in assessing the likelihood of timely debt repayment and the risk associated with the company’s ability to meet its debt obligations.

For both equity holders and debtholders, their initial investment represents their maximum possible loss.

| Equity | Debt | |

|---|---|---|

| Tenor | Indefinite | Term (10 yrs) |

| Return potential | Unlimited | Capped |

| Maximum loss | Initial investment | Initial investment |

| Investment risk | Higher | Lower |

| Desired outcome | Maximize firm value | Timely repayment |

| Issuer Perspective: | ||

| From the company’s perspective, issuing debt is riskier than issuing equity. If a company fails to meet its contractual obligations, it may be forced to declare bankruptcy and liquidate. |

Although riskier, the cost of debt is lower than the cost of equity (this is because the returns to debtholders are capped). A company generating stable, predictable cash flows generally prefers to borrow money rather than issuing additional equity to raise capital. Issuing more equity also dilutes the upside return for existing equity owners given that residual value must be shared across more owners. However, early-stage companies or companies with unpredictable cash flows that find it difficult to borrow may prefer to raise capital through equity to avoid the risk of default.

In the event of a default, a company does have some options to try and avoid bankruptcy. It can renegotiate more favorable terms with the debtholders. However, if things don’t improve, eventually the assets may have to be liquidated to raise as much money as possible to return to the bondholders. Alternatively, the company may be reorganized, with existing shareholders getting wiped out and bondholders becoming the new shareholders of the reorganized company.

| Equity | Debt | |

|---|---|---|

| Capital Cost | Higher | Lower |

| Attractiveness | Creates dilution, may be only option when issuer cash flows are absent or unpredictable | Preferred when issuer cash flows are predictable |

| Investment risk | Lower, holders cannot force liquidation | Higher, adds leverage risk |

Conflicts of Interest among Lenders and Shareholders

Potential conflicts of interest can occur between debtholders and equity holders. Debtholders would prefer that the company invests in less risky projects that generate predictable cash flows, even if those cash flows are relatively small. Equity holders, on the other hand, would prefer that the company invests in riskier projects with a much higher return potential.

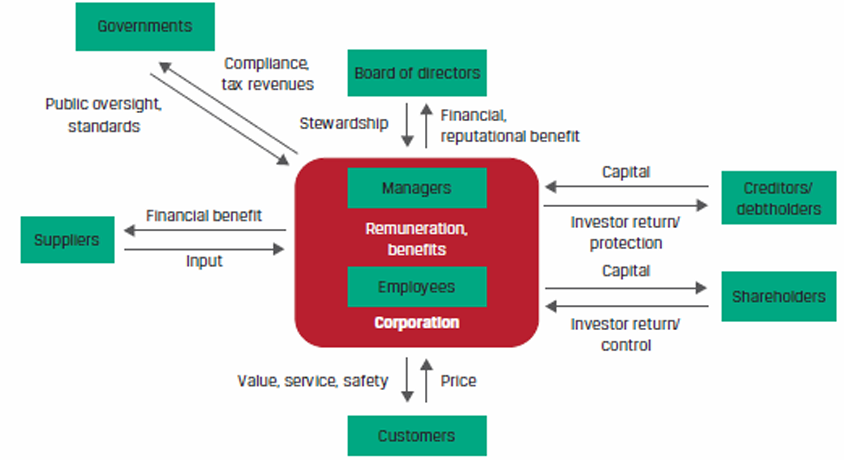

Corporate Stakeholders and Governance

A stakeholder is any individual or group that has a vested interest in a company.

The primary stakeholder groups of a company include:

- Shareholders and creditors provide capital to finance the company’s activities

- Board of directors serves as the steward of the company

- Managers execute the strategy set by the board and run day-to-day operations

- Employees provide human capital for the day-to-day operations of the company

- Customers buy the company’s products and services

- Suppliers provide raw materials as well as goods and services that cannot be produced efficiently internally.

- Government and regulators dictate the rules and regulations governing the company.

Shareholders versus Stakeholders

Traditional corporate governance frameworks were based on the shareholder theory, however, many companies are now moving to corporate governance frameworks based on the stakeholder theory.

- Shareholder theory: The goal of a company is to maximize shareholder returns. The interests of other stakeholders are considered only to the extent that they affect shareholder value.

- Stakeholder theory: The company should consider the interests of all stakeholders, not just shareholders. This theory also gives more importance to ESG considerations by making them an explicit objective for the board of directors and management.

Shareholders

Shareholders own shares in a corporation and are entitled to certain rights, such as the right to receive dividends and to vote on certain corporate issues.

A shareholder’s interests are typically focused on growth in corporate profitability that maximizes the value of the company.

Creditors/Debtholders (Banks and Private Lenders)

- They generally hold a company’s debt till maturity.

- They typically have direct access to company management and insider information which reduces information asymmetries.

- As compared to public debt holders, banks and private lenders can exert a significant degree of influence on a company.

- Most banks and private lenders prefer companies to have less financial leverage as it implies less risk. They may, however, take very different approaches to lending.

- Some focus primarily on the collateral supporting their loan;

- Others hold both debt and equity positions in the same company;

- Some have an equity-like focus on the company;

- Some lend to businesses that they would be interested in owning if the company defaulted.

Public Debtholders (Bondholders)

- They rely on public information and the ratings provided by credit rating agencies to make their investment decisions.

- In return for the capital provided, they expect to receive periodic interest payments and repayment of principal at the end of the term.

- Unlike shareholders, they do not have voting rights.

- They have limited influence over a company’s operations.

- They generally seek to minimize downside risk and prefer stability in company’s operations and performance. This is in contrast to the interests of shareholders, who are willing to take higher risks for higher potential returns.

Board of Directors

A company’s board of directors is elected by shareholders to protect shareholders’ interests, monitor the company’s operations, and provide strategic direction. The board is also responsible for hiring the CEO and overseeing management performance.

A board can be composed on both inside and independent directors.

- Inside directors are major shareholders, founders, and senior managers.

- Independent directors do not have a material relationship with the company in terms of employment, ownership, or remuneration and are chosen for their experience of managing or directing other companies.

There is no standard structure or composition for the board of a company. The number of directors can vary depending on the size, structure, and complexity of operations of the company. However, most corporate governance standards require that board members have a diverse range of expertise, backgrounds, and competencies, with at least one-third of the board being independent.

Staggered board is a commonly followed practice, in which directors are divided into three groups and elected into office in consecutive years, so that all directors are not replaced at the same time. The advantage of a staggered board is that it allows for continuous strategy implementation. The disadvantage is that it limits shareholders’ ability to effect an immediate major change in control of the company.

Managers

Managers, led by the CEO are responsible for executing the strategy set by the board. They are also in charge of the company’s day to day operations.

Senior managers are typically compensated with a base salary, a short-term cash bonus, and a multi-year incentive plan that includes one or more forms of equity (such as options, time-vested shares, and performance-vested shares). As a result, in addition to acting to protect their employment status, managers may be motivated to maximize the value of their total remuneration.

Employees

Lower-level employees seek fair salary, good working conditions, job security, career development opportunities, promotion, etc.

As compared to managers, equity ownership is a minor part of their compensation. Therefore, they are more interested in the company’s long-term stability, survival and growth.

Customers

Customers expect to receive products and services of good quality for the price paid. They also expect after-sales service, support, and guarantee/warranty for the period promised. In return, companies strive to keep their customers happy as this has a direct effect on its revenues. Of all the stakeholders, customers are least concerned about a company’s performance.

Suppliers

The primary interest of a supplier is to be paid on time for the products and services delivered to the company. Some suppliers are keen to maintain a good long-term relationship with companies as it is recurring business. Like customers, suppliers typically have an interest in the company’s long-term stability.

Governments

Government is a stakeholder as it collects taxes from companies and their employees. Governments seek to protect the interests of the general public and ensure the well-being of their nations’ economies.

Corporate ESG Considerations

ESG is an acronym for environmental, social and governance issues. The importance of good corporate governance has long been understood by analysts and shareholders. Therefore, the practice of considering governance factors in investment analysis has evolved considerably. However, the practice of considering environmental and social factors in investment analysis has evolved more slowly.

The three main catalysts for growth in ESG investing are:

- ESG issues are having more financial impacts. Many investors incurred significant losses when the companies they invested in mismanaged ESG issues.

- A greater number of younger investors are increasingly demanding that their inherited wealth or pension contributions be managed responsibly.

- Governments have started prioritizing climate change and social policies. New regulations are forcing companies to adapt their business practices to meet more stringent ESG criteria.

Historically, environmental and social issues, such as climate change, air pollution, and societal impacts of a company’s products and services, have been treated as negative externalities. However, increased stakeholder awareness and strengthening regulations have led to inclusion of environmental and societal costs in the company’s income statement by responsible investors.

| Environmental Issues | Social Issues | Governance Issues |

|---|---|---|

| - Climate change - Air and water pollution - Biodiversity - Deforestation - Energy efficiency - Waste management - Water scarcity |

- Customer satisfaction - Data privacy - Gender and diversity - Employee management - Community relations - Human rights - Labor standards |

- Board composition - Audit committee structure - Bribery and corruption - Executive compensation - Lobbying - Political contributions - Whistleblower schemes |

| Typically, a smaller set of factors are material for each company depending on the business segments and geography it operates in. |

Governance factors

Corporate governance factors to consider include:

- Company ownership and voting structure

- Relevance of board skills and experience

- Alignment of management compensation with company performance

- Strength of company shareholder rights versus peers

- Company effectiveness in managing long-term risks and sustainability

Corporate governance considerations are reasonably consistent across most companies and industries. However, environmental and social considerations differ greatly across industries. For example, environmental and social concerns for the energy sector will be very different from the concerns for the banking sector.

While evaluating ESG factors, analysts first need to evaluate if a factor is material.

An ESG factor is considered to be material when that factor is believed to have an impact on a company’s long-term business model.

Environmental factors

- Natural resource management.

- Pollution prevention.

- Water conservation.

- Energy efficiency and reduced emissions.

- Existence of carbon assets.

- Compliance with environmental and safety standards.

Social factors

- Human rights and welfare concerns in the workplace

- Data privacy and security

- Access to affordable health care products

- Community impact

A specific concern among investors of energy companies is the existence of “stranded assets” — carbon-intensive assets that are at risk of no longer being economically viable because of changes in regulation or investor sentiment.

Evaluating ESG-Related Risks and Opportunities

The process of identifying and evaluating ESG-related factors is similar for both equity and debt analyses.

- Once identified, the material impact of an ESG factor must be quantified, i.e. how will the company’s future cash flows be impacted?

- If a significant long-term adverse ESG related event is discovered, equity is immediately and disproportionately affected. The company may experience a sharp decline in share prices.

- While debt is also impacted, it is usually less affected than equity unless the company’s ability to make interest and principal payments is compromised.

- The effects on debt also vary depending on maturity. For example, some factors may have an impact in the long term but have no impact in the short term. Such factors are not relevant while evaluating short term bonds.