Corp Gov- Conflicts, Mechanisms, Risks and Benefits

Go to Corporate Issuers

Topics

Table of Contents

Introduction

- The principal-agent and other relationships between stakeholder groups

- Corporate governance mechanisms to manage stakeholder relationships

- The potential risks of poor corporate governance and the benefits from effective corporate governance

Stakeholder Conflicts and Management

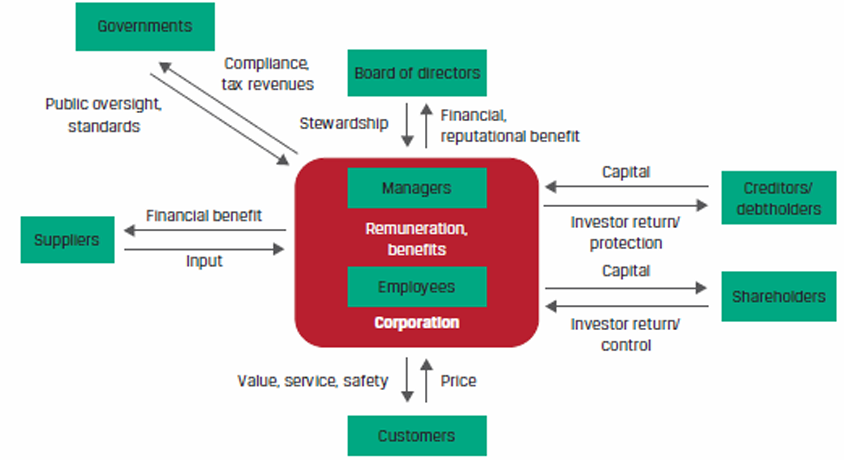

A corporation has a complex ecosystem of stakeholders.

A principal-agent relationship arises when a principal hires an agent to carry out a task or a service (e.g. shareholders and managers/directors). An agent is obliged to act in the best interests of the principal and should not have a conflict of interest in performing a task.

However, in reality, there are several conflicts of interest that arise in a principal agent relationship, for example: information asymmetry.

Information asymmetry: Managers have greater access to information about a company’s performance and prospects as compared to outsiders such as shareholders and creditors. This information asymmetry reduces shareholders’ ability to assess managers’ true performance and vote out poor performers.

Investors demand higher risk premiums and returns from companies that have greater information asymmetry.

Shareholder and Manager/Director Relationships

In this relationship, shareholders are the principals and managers/directors are the agents. Compensation is the main tool used to align the interest of managers/directors with those of the shareholders. In theory, stock grants/options offered as part of management compensation are intended to motivate managers to maximize shareholder value. However, in practice, the alignment of interests is rarely perfect.

Common examples of conflict of interests are:

- Insufficient effort: Managers may devote insufficient time to their duties. They may conduct too little monitoring of employees or assert too little control.

- Entrenchment: If the overall level of manager/director compensation is excessive, they may try to avoid risk so as to not jeopardize the compensation they have been receiving.

- Empire building: If manager/director compensation is tied to the size of the company, it can lead to

growth for growth’s sake; managers may pursue acquisitions and expansions that do not increase shareholder value. - Excessive risk taking: Because option holders only participate in stock up moves, a compensation package that relies too heavily on stock grants/options may encourage excessive risk taking by management. Similarly, a compensation package with too little or no stock grants/options can have the opposite effect.

- Self-dealing: Managers may misuse firm resources to maximize personal benefits (e.g., private planes, club memberships, and personal security), or they may defraud investors by misappropriating assets.

Agency costs: Agency costs arise due to conflicts of interest when an agent makes decisions for a principal. All public companies and large private companies are usually managed by non-owners. Therefore, an agency cost in the context of a corporation is a consequence of a conflict of interest between managers and owners.

Since outside shareholders are aware of this conflict, they will take steps that incur costs such as:

- Costs borne by owners to monitor the management of the company, e.g., expenses of the annual report, board of director expenses, etc.

- Costs borne by management to assure owners that they are maximizing the company value, e.g., the implicit cost of noncompete employment contracts and the explicit cost of insurance to guarantee performance.

The better a company is governed, the lower the agency costs.

Controlling and Minority Shareholder Relationships

Corporate ownership structures can be classified as:

- Dispersed: Many shareholders exist and none of them have the ability to individually exercise control over the company.

- Concentrated: An individual shareholder or a group has the ability to exercise control over the company (known as controlling shareholders)

Conflicts of interest may arise between controlling shareholders and minority shareholders.

- Controlling shareholders may have a large percentage of their wealth tied up in company stock and would want management to diversify the company to achieve stability. Minority shareholders with diverse portfolios, on the other hand, would prefer management to focus on the core business because they can diversify cheaply on their own.

- Controlling shareholders may have a multi-decade perspective, whereas some minority shareholders may seek quick gains from cost cutting, selling assets, or share repurchases.

Share ownership alone may not necessarily reflect whether the control of a company is dispersed or concentrated. Controlling shareholders may be either majority shareholders or minority shareholders.

- Majority shareholders: Own more than 50% of a company’s shares.

- Minority shareholders: Own less than 50% of a company’s shares.

Dual-Share Classes

An equity structure with multiple share classes tends to assign superior voting powers to one class and limited voting rights to other classes.

The multiple-class structure allows controlling shareholders avoid dilution of their voting power when new shares are issued and to retain control of board elections, strategic decisions, and all other significant voting matters for an extended period of time — even if their ownership level falls below 50%.

Shareholder vs. Creditor (Debtholder) Interests

There is a conflict of interest between the two suppliers of capital to a company under the following circumstances:

- Distribution of dividends: Creditors are concerned if a company pays excess dividends to shareholders that may impair its ability to service debt.

- Risk tolerance: Shareholders have a higher risk tolerance and prefer a company takes on more risk to generate higher returns. The better the performance of a company, the higher is the return shareholders can expect. Creditors are conservative and prefer a stable operating cash flow over higher returns as they do not have a claim to residual income.

- Increased borrowing: When a company increases its borrowing and fails to generate returns to service the debt, then the default risk faced by the creditors increases.

Corporate Governance Mechanisms

Corporate governance can be defined as the arrangement of checks, balances, and incentives that exists to manage conflicting interests among a company’s management, board, shareholders, creditors, and other stakeholders.

A sound governance structure ensures that a corporation has mechanisms in place that not only facilitate adherence to rules and regulations imposed by external authorities, but also meet the specific needs of internal stakeholders.

Shareholder Mechanisms

Mechanisms to mitigate shareholder risks include company reporting and transparency, general meetings, investor activism, derivative lawsuits, and corporate takeovers.

Corporate Reporting and Transparency

Shareholders have access to financial and non-financial information about the company from annual reports, proxy statements, disclosures on the company’s website, the investor relations department, and other channels.

Such information helps shareholders to:

- reduce the extent of information asymmetry between shareholders and managers

- assess the performance of the company and that of its directors and managers

- make informed decisions in valuing the company and deciding to purchase, sell, or transfer shares

- vote on key corporate matters or changes.

Shareholder Meetings

General meetings provide an opportunity to shareholders to exercise their vote on major corporate issues.

There are typically two types of general meetings:

- Annual general meetings: These are usually held once a year. During an AGM, a company’s annual performance is presented and discussed, and shareholders’ questions are answered.

- Extraordinary general meetings: These can be called anytime during the year, either by the company or shareholders, whenever a major resolution has to be passed such as an amendment to a company’s bylaws, mergers or acquisitions, or the sale of businesses.

Number of votes required may be one of the following two types based on the type of resolution to be passed:

- For simple decisions, a simple majority of votes is sufficient.

- For material decisions, a supermajority vote is required, i.e., 75% of the votes must be in favor of a resolution to be passed.

Proxy voting allows shareholders to authorize another individual to vote on their behalf at the AGM. In cumulative voting, shareholders may accumulate their votes to vote for one candidate in an election that involves more than one director.

Shareholder Activism

Shareholder activism refers to strategies used by shareholders to attempt to compel a company to act in a desired manner. The primary motivation of activist shareholders is to increase shareholder value. Hedge funds are amongst the most predominant shareholder activists.

Shareholder Derivative Lawsuits

Shareholder derivative lawsuits are legal proceedings initiated by one or more shareholders against board directors, management, and/or controlling shareholders of the company. However, in many countries, the law prohibits shareholders from taking legal action through the court system.

Corporate Takeovers

Shareholders prefer corporate takeover if the management of a company underperforms.

The commonly used methods for corporate takeovers are as follows:

- Proxy contest: A group attempting to take a controlling position on a company’s board influences shareholders to vote for them.

- Tender offer: An offer by a group seeking to gain control to purchase a shareholder’s shares.

- Hostile takeover: One company tries to acquire another company by bypassing the management and directly going to the company’s shareholders.

Creditor Mechanisms

Mechanisms to mitigate creditor risks include bond indenture(s), company reporting and transparency, and committee participation.

Bond Indenture

A bond indenture is a legal contract that describes the structure of a bond, the obligations of the company, and the rights of the bondholders.

- Covenants are terms in a bond indenture that specify what a bond issuer may and may not do. The goal is to reduce bondholders’ exposure to risk.

- Affirmative covenants require the company to take specific actions or meet certain requirements, such as maintaining adequate levels of insurance.

- Restrictive covenants require bond issuers to not perform certain actions, such as allowing the company’s liquidity level to fall below a minimum coverage ratio.

- Collaterals are pledged assets or financial guarantees that may be used to repay bondholders if an issuer defaults on periodic payments.

Corporate Reporting and Transparency

Creditors require the company to provide periodic financial information to monitor the risk exposure and to ensure covenants are not violated.

Creditor Committees

In some countries, official creditor committees are formed once a company files for bankruptcy. Such committees are expected to represent bondholders throughout the bankruptcy proceedings and protect bondholder interests in any restructuring or liquidation.

Board of Director and Management Mechanisms

The board of directors delegates specific functions to individual committees that, in turn, report to the board on a regular basis.

The most commonly established board committees are:

Audit Committee

The key functions of the audit committee include:

- monitoring the financial reporting process

- supervising the internal audit function, annual audit plan, and annual review

- appointing and interacting with an external auditor as well as implementing remediation per that auditor.

Governance Committee

The key functions of the governance committee include:

- developing and monitoring corporate governance policies and practices

- ensuring organizational compliance and remediation with applicable laws and regulations

- aligning organizational structure with governance principles.

Remuneration or Compensation Committee

The key functions of the remuneration committee include:

- developing director and executive remuneration policies

- overseeing performance policy management and evaluation

- setting human resources (HR) policies relating to employee compensation.

Nomination Committee

The key functions of the nomination committee include:

- overseeing the director nomination and board election process

- identifying senior leadership candidates

- maintaining board composition and independence.

Risk Committee

The key functions of the risk committee include:

- determining company risk profile

- ensuring appropriate enterprise risk management

- aligning corporate activities with risk appetite.

Investment Committee

The key functions of the investment committee include:

- assessing of major investment opportunities

- evaluating board investment recommendations.

Employee Mechanisms

Labor Laws

Standard rights of employees in any country such as hours of work, pension and retirement plans, vacation and leave, are defined in labor laws. Employees can form unions in many countries to collectively influence the management on issues they may face.

Employment Contracts

Individual employee contracts define an employee’s rights and responsibilities, remunerations, and other benefits such as ESOPs.

Customer and Supplier Mechanisms

Companies enter into contracts with both customers and suppliers that define the products, services, any guarantee, after-sales support, payment terms, etc. It also defines the course of action in case one party violates the contract.

Government Mechanisms

Regulations

Governments and regulatory agencies pass laws to protect the interests of consumers or specific stakeholders. Sensitive industries such as banks, health care, and food manufacturing companies have to comply with a rigorous regulatory framework.

Corporate Governance Codes

Many regulatory authorities have also adopted corporate governance codes, which are guiding principles for publicly traded companies. These codes require companies to disclose whether they have implemented recommended corporate governance practices or explain why they have not done so.

Corporate Governance Risks and Benefits

Risks of Poor Governance and Stakeholder Management

Weak Control Systems

Weak control systems and poor monitoring can affect a company’s performance and value. One example is that of Enron where auditors failed to uncover fraudulent reporting that ultimately affected many stakeholders.

Ineffective Decision-Making

Poor decisions include managers avoiding good investment opportunities to maintain a low-risk profile or taking on excessive risk without properly evaluating potential investments. Both decisions are not in the interests of shareholders. Such decisions may result from information asymmetry, when managers have access to more information than the board/shareholders.

==Legal, Regulatory, and Reputational Risks ==

Improper implementation and monitoring of corporate governance procedures may result in the following risks:

- Legal: Stakeholders such as shareholders, creditors and employees may file lawsuits against the company if their rights are violated.

- Regulatory: Government/regulator may choose to take action if the applicable laws are violated.

- Reputational: A company may be subjected to negative publicity by investors/analysts if there is an improperly managed conflict of interest.

Default and Bankruptcy Risks

Poor corporate governance may affect the company’s performance, which in turn may affect the company’s ability to service its debt. If creditors’ rights are violated and they choose to take legal action on defaulting debt, the company may be forced to file for bankruptcy.

Benefits of Effective Governance and Stakeholder Management

The benefits of good corporate governance and stakeholder management are as follows:

- Operational efficiency: All employees of a company have a clear understanding of their responsibilities and reporting structures. The operational efficiency of a company is improved when good governance structure is combined with strong internal control mechanisms.

- Improved control: Improved control at all levels to help a company manage its risk efficiently. Control can be improved with a good audit committee, complying with laws and regulations, and introducing procedures to handle related-party transactions.

- Better operating and financial performance: A company’s operating and financial performance can be improved with good governance practices. Proper remuneration for management, mitigation of lawsuits against the company, and improving the decision-making of its managers to make the right investments are ways that will help in improving the performance of a company.

- Lower default risk and cost of debt: A company’s cost of debt and default risk can be reduced by protecting creditors’ rights, ensuring proper audits are conducted, and that there is no information gap between the company and its creditors.