P - Interest Rates, Present Value, and Future Value

In this reading, we have explored a foundation topic in investment mathematics, the time value of money. We have developed and reviewed the following concepts for use in financial applications:

- The interest rate, r, is the required rate of return; r is also called the discount rate or opportunity cost.

- An interest rate can be viewed as the sum of the real risk-free interest rate and a set of premiums that compensate lenders for risk: an inflation premium, a default risk premium, a liquidity premium, and a maturity premium.

- The future value, FV, is the present value, PV, times the future value factor,

. - The interest rate, r, makes current and future currency amounts equivalent based on their time value.

- The stated annual interest rate is a quoted interest rate that does not account for compounding within the year.

- The periodic rate is the quoted interest rate per period; it equals the stated annual interest rate divided by the number of compounding periods per year.

- The effective annual rate is the amount by which a unit of currency will grow in a year with interest on interest included.

- An annuity is a finite set of identical sequential cash flows.

- There are two types of annuities, the annuity due and the ordinary annuity. The annuity due has a first cash flow that occurs immediately; the ordinary annuity has a first cash flow that occurs one period from the present (indexed at t = 1).

- On a time line, we can index the present as 0 and then display equally spaced hash marks to represent a number of periods into the future. This representation allows us to index how many periods away each cash flow will be paid.

- Annuities may be handled in a similar approach as single payments if we use annuity factors rather than single-payment factors.

- The present value, PV, is the future value, FV, times the present value factor,

. - The present value of a perpetuity is

, where A is the periodic payment to be received forever. - It is possible to calculate an unknown variable, given the other relevant vari ables in time value of money problems.

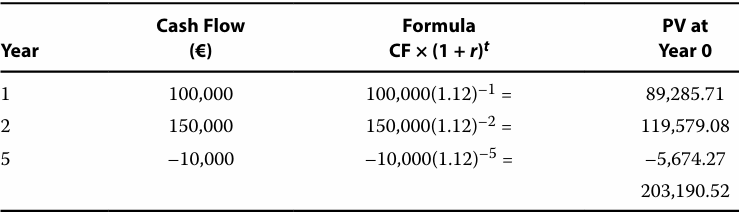

- The cash flow additivity principle can be used to solve problems with uneven cash flows by combining single payments and annuities.

Questions

1]

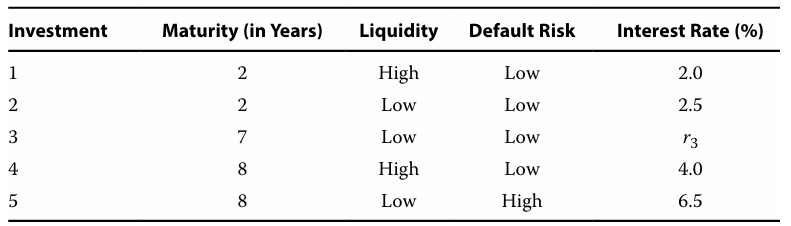

A] Explain the difference between the interest rates on Investment 1 and Investment 2.

B] Estimate the default risk premium.

C] Calculate upper and lower limits for the interest rate on Investment 3,

Liquidity of 1 is higher than 2 → Liquidity premium = 0.5

Compare 4 and 5...

Modify 4 with the liquidity premium → 4.5

Default risk premium = 2

Compare 2 and 3 → Lower bound = 2.5

Compare 3 and modified 4 → Upper bound = 4.5

2]

The nominal risk-free rate is best described as the sum of the real risk-free rate and a premium for expected inflation.

3]

Which of the following risk premiums is most relevant in explaining the difference in yields between 30-year bonds issued by the US Treasury and 30-year bonds issued by a small private issuer?

Liquidity

4]

The value in six years of $75,000 invested today at a stated annual interest rate of 7% compounded quarterly is closest to:

$113,733

5]

A bank quotes a stated annual interest rate of 4.00%. If that rate is equal to an effective annual rate of 4.08%, then the bank is compounding interest:

m = 365

6]

Given a €1,000,000 investment for four years with a stated annual rate of 3% compounded continuously, the difference in its interest earnings compared with the same investment compounded daily is closest to:

Therefore, difference is€6.

7]

A couple plans to set aside $20,000 per year in a conservative portfolio projected to earn 7 percent a year. If they make their first savings contribution one year from now, how much will they have at the end of 20 years?

Future value of an annuity.

=

$819, 909.85

8]

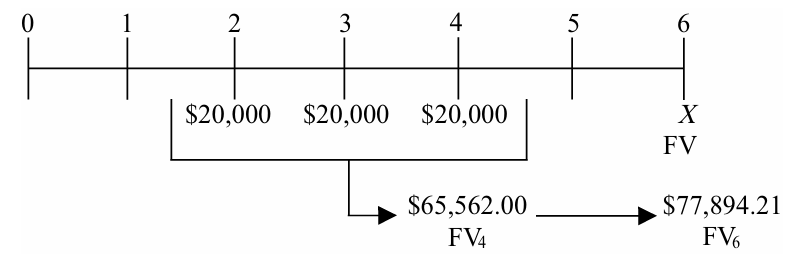

Two years from now, a client will receive the first of three annual payments of $20,000 from a small business project. If she can earn 9 percent annually on her investments and plans to retire in six years, how much will the three business project payments be worth at the time of her retirement?

Future value of a delayed annuity.

=

=$65,562

Delayed by 2 years →

$77,894.21

9]

Stated annual rate of 4%, compounded semiannually:

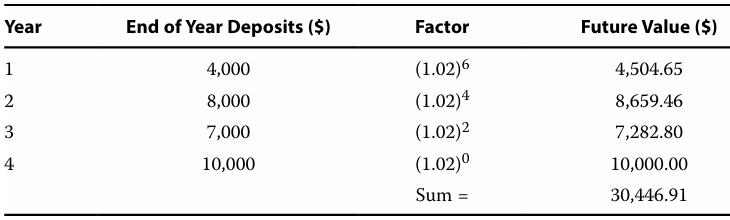

Future Value of Unequal Cash Flows

10]

To cover the first year’s total college tuition payments for his two children, a father will make a $75,000 payment five years from now. How much will he need to invest today to meet his first tuition goal if the investment earns 6 percent annually?

$56,044.36

11]

4% a year compounded annually.

$27,763.23

12]

A client requires £100,000 one year from now. If the stated annual rate is 2.50% compounded weekly, the deposit needed today is closest to:

$97,531.6

13]

A client can choose between receiving 10 annual $100,000 retirement payments, starting one year from today, or receiving a lump sum today. Knowing that he can invest at a rate of 5 percent annually, he has decided to take the lump sum. What lump sum today will be equivalent to the future annual payments?

Present value of an annuity.

$772,173.49Your client should accept no less than this amount for his lump sum payment.

14]

You are considering investing in two different instruments. The first instrument will pay nothing for three years, but then it will pay $20,000 per year for four years. The second instrument will pay $20,000 for three years and $30,000 in the fourth year. All payments are made at year-end. If your required rate of return on these investments is 8 percent annually, what should you be willing to pay for:

A] The first instrument?

B] The second instrument (use the formula for a four-year annuity)?

=PV_0=PV_3(1+0.08)^{-3}$

$52,585.46

$73,592.84

15]

Suppose you plan to send your daughter to college in three years. You expect her to earn two-thirds of her tuition payment in scholarship money, so you estimate that your payments will be $10,000 a year for four years. To estimate whether you have set aside enough money, you ignore possible inflation in tuition payments and assume that you can earn 8 percent annually on your investments. How much should you set aside now to cover these payments?

First annuity payment is one period away, giving an ordinary annuity.

=$33,121.27

$28,396.15

16]

An investment pays €300 annually for five years, with the first payment occurring today. The present value (PV) of the investment discounted at a 4% annual rate is closest to:

Annuity due:

$1,388.97

17]

At a 5% interest rate per year compounded annually, the present value (PV) of a 10-year ordinary annuity with annual payments of $2,000 is $15,443.47. The PV of a 10-year annuity due with the same interest rate and payments is closest to:

PV of a 10-year annuity due is simply the PV of the ordinary annuity multiplied by (1+r)

PV = 15433.47 x 1.05 = $16,215.64

18]

Grandparents are funding a newborn’s future university tuition costs, estimated at $50,000/year for four years, with the first payment due as a lump sum in 18 years. Assuming a 6% effective annual rate, the required deposit today is closest to:

Ordinary annuity in Year 17

=$173,255.28

$64,340.85

19]

PV if 12% annual rate of return?

PV if 12% annual rate of return?

20]

A perpetual preferred stock makes its first quarterly dividend payment of $2.00 in five quarters. If the required annual rate of return is 6% compounded quarterly, the stock’s present value is closest to:

== $133.33

$125.62

21]

A sweepstakes winner may select either a perpetuity of £2,000 a month beginning with the first payment in one month or an immediate lump sum payment of £350,000. If the annual discount rate is 6% compounded monthly, the present value of the perpetuity is:

== £400,000

22]

For a lump sum investment of ¥250,000 invested at a stated annual rate of 3% compounded daily, the number of months needed to grow the sum to ¥1,000,000 is closest to:

=0.030453

N46.21 years or 554.5 months

23]

An investment of €500,000 today that grows to €800,000 after six years has a stated annual interest rate closest to:

= 0.07988 → 8% semi annually

24]

A client plans to send a child to college for four years starting 18 years from now. Having set aside money for tuition, she decides to plan for room and board also. She estimates these costs at $20,000 per year, payable at the beginning of each year, by the time her child goes to college. If she starts next year and makes 17 payments into a savings account paying 5 percent annually, what annual payments must she make?

PV of annuity

=$70,919

X = $2,744.5If she starts next year and makes 17 payments into a savings account paying 5 percent annually.

25]

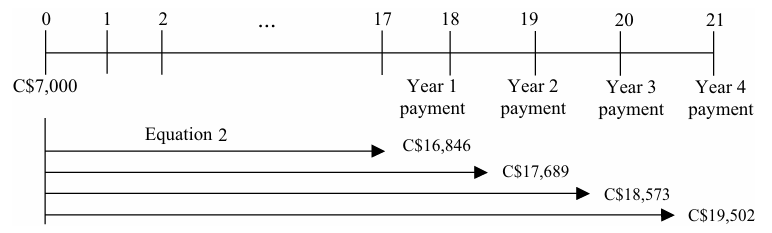

A couple plans to pay their child’s college tuition for 4 years starting 18 years from now. The current annual cost of college is C$7,000, and they expect this cost to rise at an annual rate of 5 percent. In their planning, they assume that they can earn 6 percent annually. How much must they put aside each year, starting next year, if they plan to make 17 equal payments?

We are applying FV on PV = 7,000 with N = 18, 19, 20, 21 and r = 0.05.

Find these values at t = 17 and sum them.

= C$ 62,677

X = C$ 2,221.58

26]

A sports car, purchased for £200,000, is financed for five years at an annual rate of 6% compounded monthly. If the first payment is due in one month, the monthly payment is closest to:

A = PV of Annuity / (

)

Numerator = 200000

, m = 12 and N = 5 £3,866.56

27]

Given a stated annual interest rate of 6% compounded quarterly, the level amount that, deposited quarterly, will grow to £25,000 at the end of 10 years is closest to:

FV = 25000, r = 0.06, m = 4, N = 10£460.68

28]

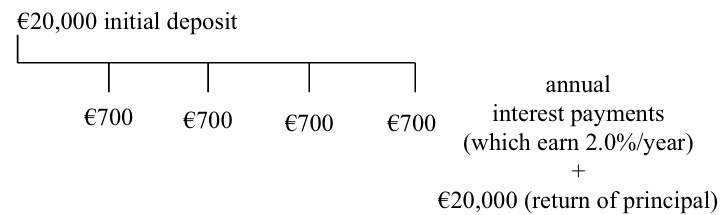

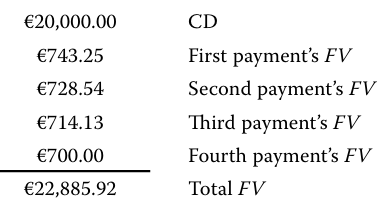

A client invests €20,000 in a four-year certificate of deposit (CD) that annually pays interest of 3.5%. The annual CD interest payments are automatically rein vested in a separate savings account at a stated annual interest rate of 2% com pounded monthly. At maturity, the value of the combined asset is closest to: